|

시장보고서

상품코드

1936635

쉘 및 튜브형 열교환기 시장 기회, 성장 촉진요인, 업계 동향 분석, 예측(2026-2035년)Shell and Tube Heat Exchanger Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

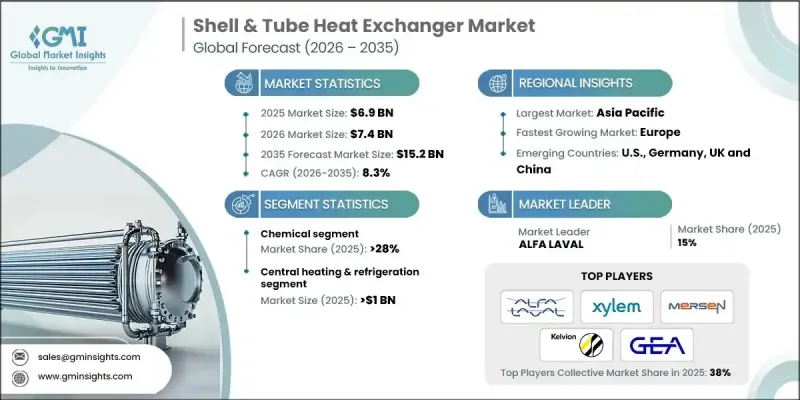

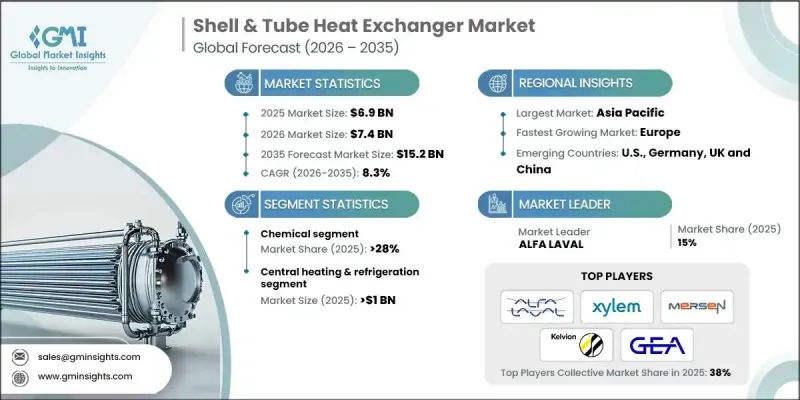

세계의 쉘 및 튜브형 열교환기 시장은 2025년에 69억 달러로 평가되었으며, 2035년까지 CAGR 8.3%로 성장하여 152억 달러에 달할 것으로 예측됩니다.

이러한 성장은 중공업 공정에 대한 투자 확대와 여러 분야에서 효율적인 가열 및 냉각 솔루션에 대한 수요 증가에 의해 주도되고 있습니다. 엄격한 에너지 효율 기준의 채택과 더불어 현대 산업 및 HVAC 인프라에서 첨단 열 관리 시스템에 대한 수요 증가가 시장 상황을 형성하고 있습니다. 산업 탈탄소화 정책과 에너지 소비 감소에 대한 강한 초점이 열회수 솔루션에 대한 수요를 가속화하고 있습니다. 또한, 저탄소 시스템의 보급, 폐열 이용의 통합, 재생에너지 발전의 확대는 시장 역학을 더욱 강화시키고 있습니다. 기업들은 에너지 효율적 운영, 열 시스템의 디지털 모니터링, 지속가능한 산업 인프라에 점점 더 많은 관심을 기울이고 있으며, 이는 업계의 장기적인 성장에 대한 긍정적인 전망을 낳고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 금액 | 69억 달러 |

| 예측 금액 | 152억 달러 |

| CAGR | 8.3% |

화학 분야는 2025년 28%의 점유율을 차지했으며, 2035년까지 CAGR 9%로 성장할 것으로 전망됩니다. 화학제품에 대한 수요 증가와 에너지 절약형 열 솔루션의 도입 확대로 업계는 강한 성장세를 보이고 있습니다. 화학 처리 시설의 엄격한 안전 규제와 실시간 운영 관리를 위한 디지털 모니터링 기술의 도입은 시장 확대를 촉진하고 있습니다. 특히 수요가 많은 화학제품 제조 환경에서 공정 효율성 향상, 다운타임 감소, 안전한 운영을 가능하게 하는 첨단 열교환기 시스템의 도입이 가속화되고 있습니다.

유럽의 쉘 및 튜브형 열교환기 시장은 2035년까지 45억 달러 규모에 달할 것으로 예상됩니다. 이러한 성장은 엄격한 환경 규제, EU 역내 배출량 감축 목표, 에너지 효율과 산업 탈탄소화를 촉진하는 강력한 정책 프레임워크에 의해 뒷받침되고 있습니다. 중공업 공정의 현대화, 폐열 회수 최적화, 디지털 열 관리 솔루션 도입에 대한 투자가 지역 시장을 더욱 강화시키고 있습니다. 유럽 산업계에서는 성능, 에너지 효율, 환경 기준을 충족하는 솔루션에 대한 수요가 증가하고 있으며, 이는 첨단 열교환기의 장기적인 도입을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 용도별, 2022-2035년

제6장 시장 규모 및 예측 : 지역별, 2022-2035년

제7장 기업 개요

KSM 26.03.13The Global Shell & Tube Heat Exchanger Market was valued at USD 6.9 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 15.2 billion by 2035.

Growth is fueled by expanding investments in heavy-duty industrial processes and a rising need for efficient heating and cooling solutions across multiple sectors. The adoption of stringent energy efficiency standards, combined with increasing demand for advanced thermal management systems in modern industrial and HVAC infrastructure, is shaping the market landscape. Industrial decarbonization policies and a strong focus on reducing energy consumption are accelerating demand for heat recovery solutions. Moreover, the increasing use of low-carbon systems, integration of waste heat utilization, and expansion of renewable energy generation are further enhancing market dynamics. Companies are increasingly emphasizing energy-efficient operations, digital monitoring of thermal systems, and sustainable industrial infrastructure, creating a positive outlook for the industry's long-term growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.9 Billion |

| Forecast Value | $15.2 Billion |

| CAGR | 8.3% |

The chemical sector accounted for 28% share in 2025 and is projected to grow at a CAGR of 9% through 2035. The industry is experiencing strong momentum due to rising demand for chemical products and increasing adoption of energy-efficient thermal solutions. Stringent safety regulations in chemical processing facilities and the integration of digital monitoring technologies for real-time operational control are further encouraging market expansion. Advanced heat exchanger systems that improve process efficiency, reduce downtime, and enable safer operations are driving adoption, particularly in high-demand chemical production environments.

Europe Shell & Tube Heat Exchanger Market reached USD 4.5 billion by 2035. The growth is supported by strict environmental regulations, EU-wide emissions reduction targets, and strong policy frameworks promoting energy efficiency and industrial decarbonization. Investments in modernizing heavy-duty industrial processes, optimizing waste heat recovery, and adopting digital thermal management solutions are further strengthening the regional market. European industries are increasingly seeking solutions that combine performance, energy efficiency, and compliance with environmental standards, driving long-term adoption of advanced heat exchangers.

Leading players operating in the Global Shell & Tube Heat Exchanger Market include Enerquip Thermal Solutions, ALFA LAVAL, API Heat Transfer, Xylem, Mason Manufacturing LLC, Bronswerk, COMP AIR TREATMENT SYSTEM Pvt. Ltd., Mersen Group, GEA Group Aktiengesellschaft, HRS Process Systems Ltd., FUNKE Warmeaustauscher Apparatebau GmbH, Thermaline, Inc., Wessels Company, Sterling Thermal Technology, Thermofin, Thrush Co, Kelvion Holding GmbH, Kinam Engineering Industries Pvt. Ltd., A.A. Anderson & Co., Inc., and Exergy LLC. Companies in the shell & tube heat exchanger market are strengthening their position by investing in research and development for more energy-efficient and compact designs. They are focusing on digital integration, enabling real-time monitoring, predictive maintenance, and performance optimization for industrial clients. Strategic partnerships with engineering and industrial solution providers allow expansion into new regional markets and high-demand sectors. Firms are also pursuing product customization, targeting heavy industries and chemical facilities with specialized materials and advanced thermal management capabilities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid Sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Application trends

- 2.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of shell & tube heat exchanger

- 3.8 Emerging opportunities & trends

- 3.8.1 Digital transformation with IoT technologies

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Oil & gas

- 5.3 Chemical

- 5.4 Power generation & metallurgy

- 5.5 Marine

- 5.6 Mechanical industry

- 5.7 Central heating & refrigeration

- 5.8 Food processing

- 5.9 Others

Chapter 6 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 UK

- 6.3.3 France

- 6.3.4 Russia

- 6.3.5 Italy

- 6.3.6 Spain

- 6.3.7 Poland

- 6.3.8 Turkey

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 Japan

- 6.4.3 South Korea

- 6.4.4 India

- 6.4.5 Indonesia

- 6.4.6 Malaysia

- 6.4.7 Thailand

- 6.4.8 Vietnam

- 6.4.9 Philippines

- 6.4.10 Australia

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 UAE

- 6.5.3 Egypt

- 6.5.4 South Africa

- 6.5.5 Nigeria

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Argentina

- 6.6.3 Colombia

- 6.6.4 Chile

Chapter 7 Company Profiles

- 7.1 A.A. Anderson & Co., Inc.

- 7.2 ALFA LAVAL

- 7.3 API Heat Transfer

- 7.4 Bronswerk

- 7.5 COMP AIR TREATMENT SYSTEM Pvt. Ltd.

- 7.6 Enerquip Thermal Solutions

- 7.7 Exergy LLC

- 7.8 FUNKE Warmeaustauscher Apparatebau GmbH

- 7.9 GEA Group Aktiengesellschaft

- 7.10 HRS Process Systems Ltd.

- 7.11 Kelvion Holding GmbH

- 7.12 Kinam Engineering Industries Pvt. Ltd.

- 7.13 Mason Manufacturing LLC

- 7.14 Mersen Group

- 7.15 Sterling Thermal Technology

- 7.16 Thermaline, Inc

- 7.17 Thermofin

- 7.18 Thrush Co

- 7.19 Wessels Company

- 7.20 Xylem