|

시장보고서

상품코드

1936640

항공우주 반도체 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Aerospace Semiconductor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

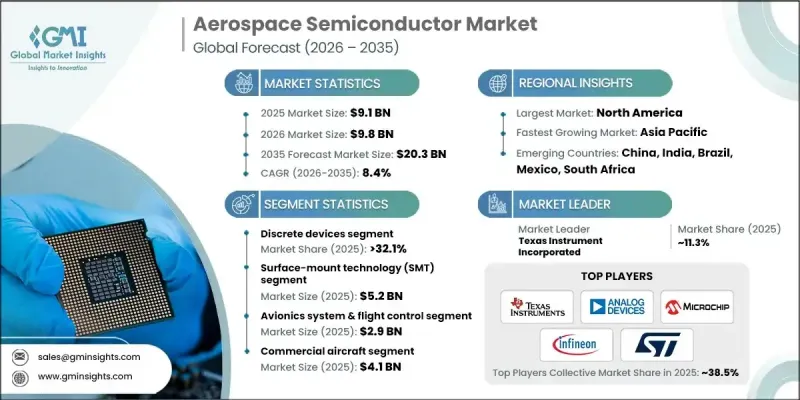

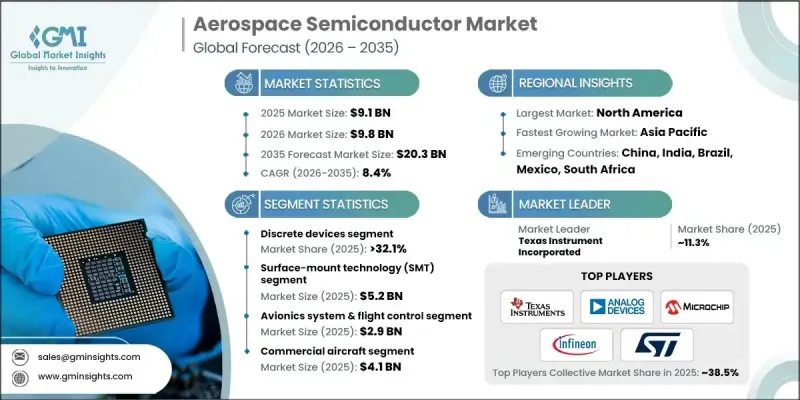

세계의 항공우주 반도체 시장은 2025년에 91억 달러로 평가되었으며, 2035년까지 CAGR 8.4%로 성장하여 203억 달러에 달할 것으로 예측됩니다.

시장 성장은 첨단 항공전자, 비행 제어 시스템, 차세대 항법 및 통신 기술의 채택 확대에 의해 촉진되고 있습니다. 현대 항공기 및 자율비행 시스템용 경량화, 고성능, 고신뢰성 전자부품에 대한 수요 증가가 시장 확대를 견인하고 있습니다. 또한, 위성 기술, 무인 항공 시스템, 우주 탐사용 반도체 솔루션도 수요 급증에 기여하고 있습니다. 통합 비행 관리 시스템, 첨단 조종석 디스플레이와 같은 항공 전자기기 혁신은 반도체 수요를 더욱 가속화하고 있습니다. 국방 현대화와 전 세계 군사비 지출 증가는 민간 및 군용 항공기 애플리케이션 전반에 걸쳐 안전성, 신뢰성, 정확성을 보장하는 항공우주 등급 방사선 내성 반도체 솔루션의 채택을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 91억 달러 |

| 예측 금액 | 203억 달러 |

| CAGR | 8.4% |

2025년 개별 장치 부문은 32.1%의 점유율을 차지했습니다. 이 부품들은 항공전자, 레이더, 비행 제어 시스템에서 전력 관리, 신호 조정, 보호에 필수적인 부품입니다. 높은 신뢰성, 열 안정성, 긴 수명으로 인해 상업, 국방, 우주 프로그램에서 필수적인 존재가 되었습니다.

표면 실장 기술(SMT) 부문은 2025년 52억 달러의 시장 규모를 창출했습니다. SMT의 컴팩트한 크기, 경량 설계, 고밀도 실장은 신뢰성을 향상시키고 조립 시간을 단축하여 보다 진보된 항공전자, 레이더, 통신 솔루션을 실현합니다. 이 기술은 민간, 군사, 우주 분야를 넘나드는 현대 항공우주 응용 분야에서 여전히 필수 불가결한 기술입니다.

북미 항공우주 반도체 시장은 2025년 43%의 점유율을 차지했습니다. 이 지역의 성장은 항공우주 및 방위 기술 발전과 군용 및 민간 항공기 수요 증가에 힘입어 성장하고 있습니다. 각 업체들은 첨단 항법, 통신, 항공전자 시스템을 지원하는 고성능, 고신뢰성 반도체 제품 개발을 우선순위로 삼고 있으며, 정부 시책을 활용해 시장에서의 입지를 강화하기 위해 노력하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 항공우주 반도체 시장 추정 및 예측 : 유형별, 2022-2035

제6장 시장 추정 및 예측 : 기술별, 2022-2035

제7장 항공우주 반도체 시장 추정 및 예측 : 용도별, 2022-2035

제8장 항공우주 반도체 시장 추정 및 예측 : 용도별, 2022-2035

제9장 항공우주 반도체 시장 추정 및 예측 : 지역별, 2022-2035

제10장 기업 개요

KSM 26.03.05The Global Aerospace Semiconductor Market was valued at USD 9.1 billion in 2025 and is estimated to grow at a CAGR of 8.4% to reach USD 20.3 billion by 2035.

The market's growth is fueled by the increasing adoption of advanced avionics, flight control systems, and next-generation navigation and communication technologies. Rising demand for lightweight, high-performance, and reliable electronic components for modern aircraft, as well as autonomous flight systems, is driving market expansion. Additionally, semiconductor solutions for satellite technologies, unmanned aerial systems, and space exploration are contributing to the surge in demand. Innovations in avionics, such as integrated flight management systems and sophisticated cockpit displays, are further accelerating the need for semiconductors. Defense modernization and increasing global military expenditure are also supporting the adoption of aerospace-grade, radiation-hardened semiconductor solutions that ensure safety, reliability, and precision across commercial and military aircraft applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.1 Billion |

| Forecast Value | $20.3 Billion |

| CAGR | 8.4% |

In 2025, discrete devices segment accounted for 32.1% share. These components are crucial for power management, signal regulation, and protection in avionics, radar, and flight control systems. Their high reliability, thermal stability, and extended lifecycle make them indispensable for commercial, defense, and space programs.

The surface-mount technology (SMT) segment generated USD 5.2 billion in 2025. SMT's compact size, lightweight design, and high-density packaging improve reliability and reduce assembly times, enabling more sophisticated avionics, radar, and communication solutions. This technology remains essential for modern aerospace applications across commercial, military, and space sectors.

North America Aerospace Semiconductor Market held 43% share in 2025. The region's growth is driven by advancements in aerospace and defense technologies and rising demand for both military and commercial aircraft. Companies are prioritizing the development of high-performance, reliable semiconductor products to support advanced navigation, communication, and avionics systems while leveraging government initiatives to strengthen their market position.

Prominent players in the Global Aerospace Semiconductor Market include Analog Devices, Inc., BAE Systems plc, Broadcom Inc., Cobham Advanced Electronic Solutions, Infineon Technologies AG, Intel Corporation, Maxim Integrated Products, Inc., Microchip Technology, Inc., Northrop Grumman Microelectronics, NXP Semiconductors N.V., ON Semiconductor Corporation, Orbit Semiconductor, Inc., Qorvo, Inc., Skyworks Solutions, Inc., STMicroelectronics N.V., Teledyne e2v, Teledyne Technologies Incorporated, Texas Instruments Incorporated, and VPT, Inc. Key strategies adopted by companies to strengthen their position in the aerospace semiconductor market include investing heavily in research and development to deliver cutting-edge and radiation-hardened components, forming strategic partnerships with aerospace and defense manufacturers, and expanding production capabilities to meet increasing demand. Firms are also focusing on mergers and acquisitions to broaden their technology portfolio and geographic reach, while implementing robust quality assurance processes to comply with strict aerospace standards.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 End Use trends

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in commercial and military aircraft production

- 3.2.1.2 Rise in avionics and flight control system complexity

- 3.2.1.3 Increasing adoption of advanced radar and communication systems

- 3.2.1.4 Demand for high-reliability and radiation-hardened components

- 3.2.1.5 Integration of AI and edge computing in aerospace platforms

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and qualification costs

- 3.2.2.2 Long product certification and approval cycles

- 3.2.3 Market opportunities

- 3.2.4 Expansion of unmanned aerial vehicles and drones

- 3.2.5 Growth in space exploration and satellite constellations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2022-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2026-2035)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By Region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Aerospace Semiconductor Market Estimates & Forecast, By Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends,

- 5.2 Discrete Devices

- 5.2.1 Diodes

- 5.2.2 Transistors

- 5.2.3 Thyristors

- 5.2.4 Modules

- 5.3 Optical Devices

- 5.3.1 LEDs

- 5.3.2 Photodetectors

- 5.3.3 Laser

- 5.3.4 Microwave Devices

- 5.3.5 Sensors

- 5.4 ICs

- 5.4.1 Memories

- 5.4.2 MPUs

- 5.4.3 Logic ICs

- 5.4.4 Analog ICs

- 5.4.5 Hybrid ICs

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Surface-Mount Technology (SMT)

- 6.3 Through-Hole Technology (THT)

Chapter 7 Aerospace Semiconductor Market Estimates & Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Avionics systems & flight control

- 7.3 Communication & connectivity solutions

- 7.4 Power distribution & management

- 7.5 Navigation & sensing technologies

- 7.6 Safety & emergency systems

- 7.7 Aircraft entertainment systems

Chapter 8 Aerospace Semiconductor Market Estimates & Forecast, By End-Use, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Commercial aircraft

- 8.3 Military aircraft

- 8.4 Satellite launch vehicle

- 8.5 Others

Chapter 9 Aerospace Semiconductor Market Estimates & Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends, by region

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia-Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia-Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Analog Devices, Inc.

- 10.2 BAE Systems plc

- 10.3 Broadcom Inc.

- 10.4 Cobham Advanced Electronic Solutions

- 10.5 Infineon Technologies AG

- 10.6 Intel Corporation

- 10.7 Maxim Integrated Products, Inc.

- 10.8 Microchip Technology, Inc.

- 10.9 Northrop Grumman Microelectronics

- 10.10 NXP Semiconductors N.V.

- 10.11 ON Semiconductor Corporation

- 10.12 Orbit Semiconductor, Inc.

- 10.13 Qorvo, Inc.

- 10.14 Skyworks Solutions, Inc.

- 10.15 STMicroelectronics N.V.

- 10.16. Teledyne e2 v

- 10.17 Teledyne Technologies Incorporated

- 10.18 Texas Instruments Incorporated

- 10.19 VPT, Inc.