|

시장보고서

상품코드

1936641

레이저 절단기 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Laser Cutting Machines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

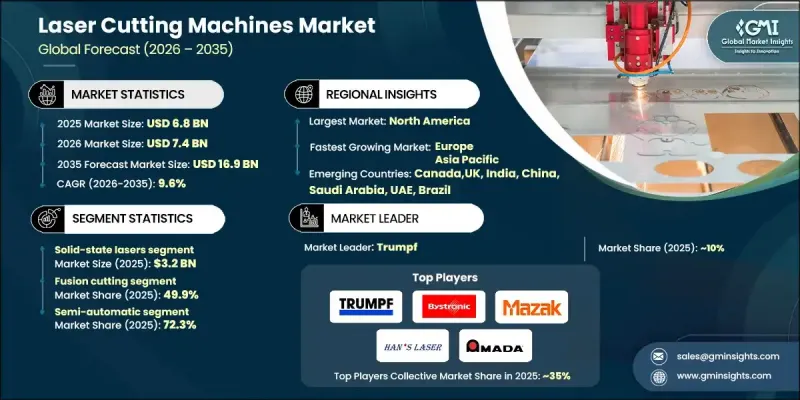

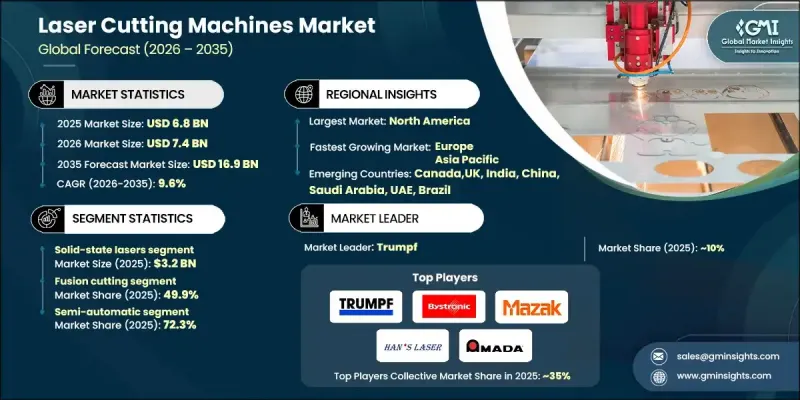

세계의 레이저 절단기 시장은 2025년에 68억 달러로 평가되었으며, 2035년까지 CAGR 9.6%로 성장하여 169억 달러에 달할 것으로 예측됩니다.

각 산업 분야의 제조업체들이 자동화 기술과 인더스트리 4.0을 적극적으로 도입하면서 시장은 빠르게 확대되고 있습니다. 레이저 절단기는 스마트 팩토리 운영의 핵심이 되고 있으며, 연결된 설비, 실시간 모니터링, 고도의 분석을 가능하게함으로써 예지보전을 통한 효율 최적화와 다운타임 감소를 실현합니다. 이 기계는 자동화된 워크플로우에 원활하게 통합할 수 있으며, 마이크론 단위의 정밀도와 최소한의 후처리로 정밀하고 고품질의 절단을 제공합니다. 자동차, 항공우주, 전자기기, 산업기계 분야의 수요 증가가 성장을 견인하고 있습니다. 이러한 산업에서는 기존의 절단 방법으로는 일관되게 달성할 수 없는 가볍고 복잡한 정밀 조립 부품이 필요하기 때문입니다. 레이저 시스템이 구현하는 깨끗한 모서리와 뛰어난 기하학적 정밀도는 생산성을 향상시키고 재료 낭비를 줄여 현대 제조에 필수적인 요소로 자리 잡았습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 68억 달러 |

| 예측 금액 | 169억 달러 |

| CAGR | 9.6% |

고체 레이저 부문은 2025년 32억 달러의 시장 규모를 기록했으며, 2026년부터 2035년까지 CAGR 10%로 성장할 것으로 예상됩니다. 고체 레이저 부문, 특히 파이버 레이저 및 디스크 레이저는 기존의 가스 기반 시스템에 비해 우수한 빔 품질, 빠른 절단 속도, 낮은 운영 비용 및 높은 에너지 효율로 인해 선호되고 있습니다. 이러한 특성으로 인해 고정밀 산업 작업 및 완전 자동화된 생산 라인에 매우 적합합니다. 솔리드 스테이트 레이저는 금속 가공, 자동차, 항공우주, 전자제품 제조 등 다양한 분야에 적용되어 디지털 전환과 산업 효율을 향상시키고 있습니다.

용융 절단 부문은 2025년 49.9%의 점유율을 차지했으며, 2035년까지 연평균 9.9%의 성장률을 기록할 것으로 예상됩니다. 용융 절단은 다용도성, 고속, 고정밀, 다양한 금속 가공 능력과 더불어 후처리를 최소화할 수 있는 매끄러운 절단면을 구현할 수 있다는 점에서 여전히 선호되는 방법입니다. 그 효율성은 자동차, 항공우주, 전자 및 산업 제조 분야에서 재료 폐기물 감소, 더 엄격한 공차, 생산 효율화와 같은 산업계의 요구에 부합합니다.

미국 레이저 절단기 시장은 2025년에 19억 달러에 달했으며, 2026년부터 2035년까지 연평균 9.8%의 성장률을 기록할 것으로 예상됩니다. 자동차, 항공우주, 전자, 금속 가공 등 정밀한 절단 부품과 복잡한 설계를 필요로 하는 산업에서 강한 수요가 성장을 주도하고 있습니다. 레이저 소스, 소프트웨어 통합 및 자동화 기능의 지속적인 기술 혁신은 광범위한 보급을 지원하고 제조업체가 기존 시스템의 업그레이드 및 확장을 촉진하는 요인으로 작용하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 기술별, 2022-2035

제6장 시장 추정 및 예측 : 제조 공정별, 2022-2035

제7장 시장 추정 및 예측 : 기능 유형별, 2022-2035

제8장 시장 추정 및 예측 : 용도별, 2022-2035

제9장 시장 추정 및 예측 : 유통 채널별, 2022-2035

제10장 시장 추정 및 예측 : 지역별, 2022-2035

제11장 기업 개요

KSM 26.03.05The Global Laser Cutting Machines Market was valued at USD 6.8 billion in 2025 and is estimated to grow at a CAGR of 9.6% to reach USD 16.9 billion by 2035.

The market is experiencing rapid expansion as manufacturers across industries increasingly adopt automation technologies and Industry 4.0 practices. Laser cutting machines are becoming central to smart factory operations, enabling connected equipment, real-time monitoring, and advanced analytics to optimize efficiency and reduce downtime through predictive maintenance. These machines allow seamless integration into automated workflows, delivering precise, high-quality cuts with micron-level accuracy and minimal post-processing. Rising demand from automotive, aerospace, electronics, and industrial machinery sectors is driving growth, as these industries require lightweight, complex, and intricately assembled components that conventional cutting methods cannot achieve consistently. The ability of laser systems to produce clean edges and superior geometric accuracy enhances productivity while reducing material waste, making them indispensable for modern manufacturing.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.8 Billion |

| Forecast Value | $16.9 Billion |

| CAGR | 9.6% |

The solid-state lasers segment generated USD 3.2 billion in 2025 and is expected to grow at a CAGR of 10% from 2026 to 2035. The solid-state segment, particularly fiber and disk lasers, is favored due to superior beam quality, faster cutting speeds, lower operating costs, and enhanced energy efficiency compared with traditional gas-based systems. These characteristics make them highly suitable for high-precision industrial operations and fully automated production lines. Solid-state lasers are increasingly adopted across metal fabrication, automotive, aerospace, and electronics manufacturing, supporting digital transformation and industrial efficiency.

The fusion cutting segment held a 49.9% share in 2025 and is anticipated to grow at a CAGR of 9.9% through 2035. Fusion cutting remains the preferred method due to its versatility, high speed, precision, and ability to handle a wide range of metals while producing smooth edges that require minimal post-processing. Its efficiency aligns with industry needs for reduced material waste, tighter tolerances, and streamlined production in automotive, aerospace, electronics, and industrial manufacturing sectors.

U.S. Laser Cutting Machines Market reached USD 1.9 billion in 2025 and is expected to grow at a CAGR of 9.8% between 2026 and 2035. Strong demand from industries requiring precision-cut components and complex designs, such as automotive, aerospace, electronics, and metal fabrication, is driving growth. Continuous technological advancements in laser sources, software integration, and automation capabilities support widespread adoption and encourage manufacturers to upgrade or expand their existing systems.

Key players in the Global Laser Cutting Machines Market include Bystronic, Coherent, Mitsubishi Electric Corporation, IPG Photonics, Trumpf, Amada, Jenoptik, LVD Company, Tanaka, Mazak Optonics, Trotec Laser, Universal Laser Systems, Prima Power, Han's Laser, and Epilog Laser. Companies in the laser cutting machines market are employing multiple strategies to expand their market presence and maintain a competitive advantage. They are investing heavily in R&D to develop faster, more energy-efficient, and higher-precision laser systems that cater to diverse industrial applications. Strategic collaborations with OEMs and industrial integrators are being used to strengthen distribution networks and ensure seamless integration into smart factories. Manufacturers are expanding production capacity, introducing fiber and hybrid laser technologies, and enhancing software and automation compatibility to attract high-end clients.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Process

- 2.2.4 Function type

- 2.2.5 Application

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of automation & industry 4.0

- 3.2.1.2 Increasing demand for high-precision fabrication

- 3.2.1.3 Shift toward energy-efficient fiber & solid-state lasers

- 3.2.1.4 Demand for reduced material waste & higher productivity

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High operational & maintenance expenses

- 3.2.2.2 Material limitations & processing challenges

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By technology

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Solid-state lasers

- 5.3 Gas lasers

- 5.4 Semiconductor laser

Chapter 6 Market Estimates & Forecast, By Process, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Fusion cutting

- 6.3 Flame cutting

- 6.4 Sublimation cutting

Chapter 7 Market Estimates & Forecast, By Function Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Semi-automatic

- 7.3 Robotic

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Consumer electronics

- 8.4 Defense and aerospace

- 8.5 Industrial

- 8.6 Others (medical, energy & power etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Amada

- 11.2 Bystronic

- 11.3 Coherent

- 11.4 Epilog Laser

- 11.5 Han's Laser

- 11.6 IPG Photonics

- 11.7 Jenoptik

- 11.8 LVD Company

- 11.9 Mazak Optonics

- 11.10 Mitsubishi Electric Corporation

- 11.11 Prima Power

- 11.12 Tanaka

- 11.13 Trotec Laser

- 11.14 Trumpf

- 11.15 Universal Laser Systems