|

시장보고서

상품코드

1936645

여드름 케어 화장품 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Anti-acne Cosmetics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

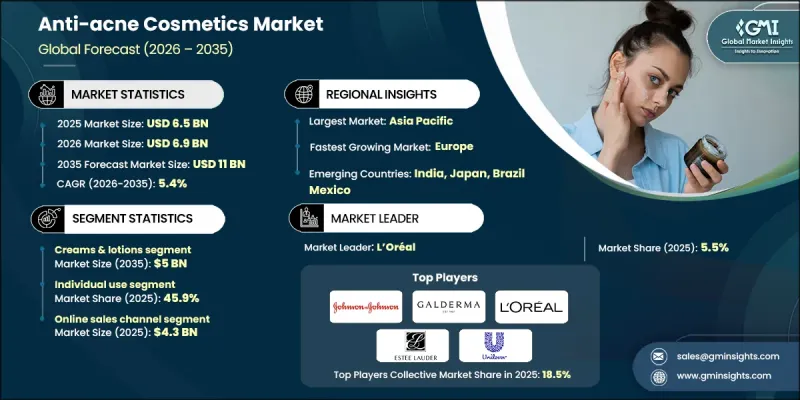

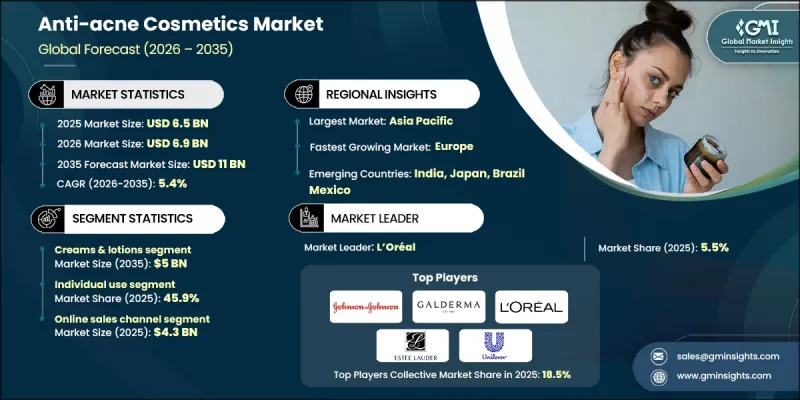

세계의 여드름 케어 화장품 시장은 2025년에 65억 달러로 평가되었으며, 2035년까지 CAGR 5.4%로 성장하여 110억 달러에 달할 것으로 예측됩니다.

시장 성장은 확대되는 클린 뷰티 운동과 천연 및 유기농 성분을 함유한 스킨케어 제품에 대한 선호도 증가에 큰 영향을 받고 있습니다. 합성 화합물의 잠재적 부작용에 대한 우려가 커지면서 소비자들은 보다 순하고 무독성이며 천연 유래 성분으로 만들어진 제품을 선호하는 경향이 강해지고 있습니다. 이러한 소비자 행동의 변화는 업계 전반의 제품 개발 전략을 재구성하고 있으며, 제조업체들은 클린 라벨에 대한 기대에 부합하도록 제품을 재구성하고 있습니다. 피부 건강에 대한 인식이 높아지고 퍼스널케어에 대한 지출이 증가하면서 지속적인 수요를 뒷받침하고 있습니다. 또한, 지속가능한 미용 습관에 대한 관심 증가와 친환경 제품을 장려하는 지원적인 규제 프레임워크는 장기적인 시장 확대를 촉진하고 있습니다. 피부 관리 습관이 성분에 대한 인식과 건강 지향성을 중시하게 되면서, 여드름 방지 화장품은 다양한 연령대와 피부 타입에서 폭넓게 받아들여지고 있으며, 2025년 이후에도 꾸준한 성장세를 이어갈 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035 |

| 개시 금액 | 65억 달러 |

| 예측 금액 | 110억 달러 |

| CAGR | 5.4% |

크림 및 로션 부문은 2025년에 29억 달러의 매출을 창출하고 2035년까지 50억 달러에 달할 것으로 예상됩니다. 이 부문은 다재다능함과 적용의 용이성으로 인해 계속해서 주류의 지위를 유지하고 있습니다. 소비자들은 여드름 관리에 도움이 될 뿐만 아니라 보습, 피부 톤업, 장기적인 피부 관리 등 부가적인 효과를 제공하는 외용제 타입의 제품을 선호합니다. 다기능 스킨케어 솔루션에 대한 소비자의 기대치 변화로 인해 여드름 치료제 카테고리의 크림과 로션에 대한 수요가 지속적으로 증가하고 있습니다.

개인용 부문은 2025년 45.9%의 점유율을 차지했습니다. 이 부문의 성장은 가정에서 사용할 수 있는 저렴하고 편리한 여드름 케어 솔루션에 대한 소비자의 선호도가 높아지면서 성장세를 견인하고 있습니다. 자가 관리 습관으로 전환함으로써 잦은 전문 치료에 대한 의존도를 낮추고, 시간과 비용의 효율성을 실현하고 있습니다. 이러한 추세는 개인화된 스킨케어와 자율적인 제품 선택에 대한 광범위한 움직임을 반영하고 있으며, 전체 시장의 성장을 주도하는 개인 소비자의 중요성을 뒷받침합니다.

미국 여드름 방지 화장품 시장은 2025년 74.5%의 점유율을 차지했습니다. 이러한 시장에서의 선도적 지위는 높은 소비자 인지도, 일반의약품 스킨케어 제품의 높은 보급률, 첨단 피부과 솔루션의 폭넓은 가용성에 의해 뒷받침되고 있습니다. 기존 프리미엄 브랜드의 존재, 디지털 마케팅의 영향력, 임상적으로 검증된 화장품 제품에 대한 수요 확대가 결합되어 시장 침투를 가속화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품 유형별, 2022-2035

제6장 시장 추정 및 예측 : 가격별, 2022-2035

제7장 시장 추정 및 예측 : 최종 용도별, 2022-2035

제8장 시장 추정 및 예측 : 유통 채널별, 2022-2035

제9장 시장 추정 및 예측 : 지역별, 2022-2035

제10장 기업 개요

KSM 26.03.05The Global Anti-acne Cosmetics Market was valued at USD 6.5 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 11 billion by 2035.

Market growth is strongly influenced by the expanding clean beauty movement and the rising preference for natural and organic skincare formulations. Consumers are increasingly prioritizing products made with gentle, non-toxic, and naturally derived ingredients, driven by growing concerns about the potential side effects of synthetic compounds. This shift in consumer behavior is reshaping product development strategies across the industry, with manufacturers responding by reformulating offerings to align with clean-label expectations. Rising awareness of skin health, combined with increased spending on personal care, continues to support sustained demand. Additionally, growing interest in sustainable beauty practices and supportive regulatory frameworks promoting environmentally responsible products are reinforcing long-term market expansion. As skincare routines become more ingredient-conscious and wellness-oriented, anti-acne cosmetics are gaining wider acceptance across diverse age groups and skin types, supporting consistent growth beyond 2025.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.5 Billion |

| Forecast Value | $11 Billion |

| CAGR | 5.4% |

The creams and lotions segment generated USD 2.9 billion in 2025 and is expected to reach USD 5 billion by 2035. This segment remains dominant due to its versatility and ease of application. Consumers favor topical formats that not only help manage acne but also deliver complementary benefits such as moisturization, skin tone enhancement, and long-term skin maintenance. Changing consumer expectations toward multifunctional skincare solutions continue to strengthen demand for creams and lotions within the anti-acne category.

The individual-use segment accounted for 45.9% share in 2025. Growth in this segment is driven by increasing consumer preference for accessible, affordable, and convenient acne care solutions used at home. The shift toward self-care routines has reduced reliance on frequent professional treatments, offering time and cost efficiency. This trend reflects a broader movement toward personalized skincare and independent product selection, reinforcing the importance of individual consumers in driving overall market growth.

United States Anti-acne Cosmetics Market held 74.5% share in 2025. Market leadership is supported by strong consumer awareness, high adoption of over-the-counter skincare products, and widespread availability of advanced dermatological solutions. The presence of established premium brands, combined with digital marketing influence and growing demand for clinically validated cosmetic products, continues to accelerate market penetration.

Key companies operating in the Global Anti-acne Cosmetics Market include L'Oreal, Johnson & Johnson, Unilever, Estee Lauder, Beiersdorf, Galderma, Shiseido, Bayer, AbbVie, Natura & Co, Pierre Fabre, Sunday Riley, Mario Badescu, Honasa Consumer, and Teva. Companies in the Anti-acne Cosmetics Market are strengthening their market position through product innovation, clean-label reformulations, and sustainability-focused strategies. Leading players are investing in research to develop gentle yet effective formulations that align with natural and dermatologically tested standards. Expansion across digital and direct-to-consumer channels is improving brand reach and customer engagement. Firms are also leveraging influencer marketing, personalization tools, and targeted product portfolios to capture specific consumer segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Price

- 2.2.4 End Use

- 2.2.5 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of acne among adolescents and adults.

- 3.2.1.2 Growing awareness and dermatological consultations.

- 3.2.1.3 Innovation in formulations and delivery systems.

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Changing consumer preferences and trends

- 3.2.2.2 Counterfeit and imitation products

- 3.2.3 Opportunities

- 3.2.3.1 Integration of smart skincare and personalization.

- 3.2.3.2 Sustainability and clean beauty trends.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By product type

- 3.6.2 By region

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Gap analysis

- 3.10 Risk assessment and mitigation

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Consumer behaviour analysis

- 3.13.1 Purchasing patterns

- 3.13.2 Preference analysis

- 3.13.3 Regional variations in consumer behaviour

- 3.13.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022-2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Masks

- 5.3 Creams & lotions

- 5.4 Cleansers & toners

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Price, 2022-2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Low

- 6.3 Medium

- 6.4 High

Chapter 7 Market Estimates & Forecast, By End Use, 2022-2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Individual use

- 7.3 Spas and parlors

- 7.4 Dermatological clinics

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-Commerce

- 8.2.2 Company website

- 8.3 Offline

- 8.3.1 Supermarkets/Hypermarkets

- 8.3.2 Specialty Stores

- 8.3.3 Others (Individual stores, Departmental stores, etc.)

Chapter 9 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Bayer

- 10.3 Beiersdorf

- 10.4 Estee Lauder

- 10.5 Galderma

- 10.6 Honasa Consumer

- 10.7 Johnson & Johnson

- 10.8 L'Oreal

- 10.9 Mario Badescu

- 10.10 Natura & Co

- 10.11 Pierre Fabre

- 10.12 Shiseido

- 10.13 Sunday Riley

- 10.14 Teva

- 10.15 Unilever