|

시장보고서

상품코드

1936657

수소 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Global Hydrogen Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

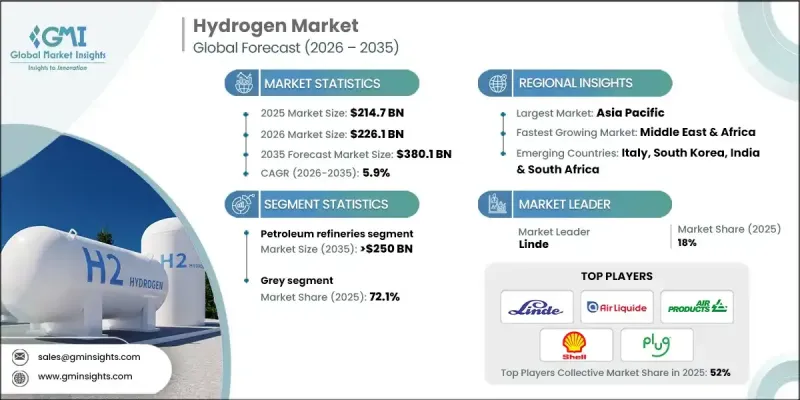

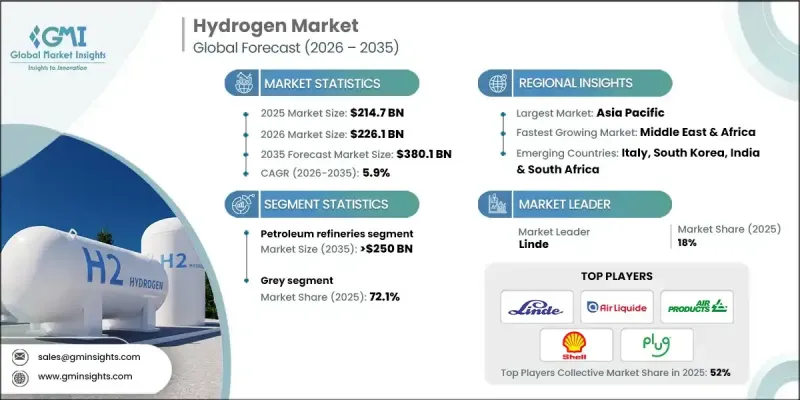

세계의 수소 시장은 2025년에 2,147억 달러로 평가되었으며, 2035년까지 CAGR 5.9%로 성장하여 3,801억 달러에 달할 것으로 예측됩니다.

시장 확대는 기후변화 대응 노력, 기술 발전, 정책 프레임워크의 진화를 배경으로 화석연료 기반 수소 생산에서 저탄소 경로로의 전환이 지속되고 있는 데 기인합니다. 에너지 집약적 산업과 화학 제조(암모니아 및 메탄올 생산 포함)에서 수소의 채택이 확대되면서 강력한 성장 모멘텀을 창출하고 있습니다. 기업들은 배출량을 최소화하기 위해 천연가스와 탄소 포집 및 저장(CCS)을 결합한 블루 수소 솔루션에 집중하고 있습니다. 한편, 탈탄소화 목표에 따라 그린 수소 도입도 가속화되고 있습니다. 저탄소 수소의 생산비용 하락과 더불어 정부의 지원책과 청정에너지 의무화가 시장 역학을 강화하고 있습니다. 중국은 전 세계 생산능력의 약 2/3, 전해장치 설치량의 약 60%, 생산량의 약 60%를 차지하며, 국내 생산량은 연간 20GW를 초과하여 세계 총수요를 초과하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 2,147억 달러 |

| 예측 금액 | 3,801억 달러 |

| CAGR | 5.9% |

2025년에는 재래식 정제 및 원유 소비에 대한 의존도가 지속되면서 회색 수소 부문이 72.1%의 점유율을 차지할 것으로 예상됩니다. 그러나 수증기 메탄 개질법의 높은 탄소강도로 인해 그린 수소로의 전환이 가속화되고 있습니다. 온실가스 배출량 감축과 지속가능성 목표 달성에 대한 압박으로 산업계는 저배출 수소 대안을 모색하고 있으며, 이는 새로운 성장 기회를 창출하고 있습니다.

정유 부문은 탈황 공정에서 수소의 통합 확대에 힘입어 2035년까지 2,500억 달러 규모에 이를 것으로 예상됩니다. 수소는 연료 내 황 함량 감소에 필수적이며, 정유소는 넷제로 목표를 달성하기 위해 단계적으로 그린 수소를 도입하고 있습니다. 이러한 지속적인 변화가 전체 시장의 성장을 뒷받침하고 있습니다.

북미 수소 시장은 2025년 12.1%의 점유율을 차지했으며, 정부 주도의 노력과 청정에너지 정책에 힘입어 성장세를 이어갈 것으로 전망됩니다. 캘리포니아 등 지역에서는 연료전지차 도입과 인프라 확충을 주도하고 있으며, 캐나다는 세계 시장을 향한 주요 청정 수소 수출국으로서 입지를 다지고 있습니다. 탈탄소화, 에너지 전환, 기술 혁신에 대한 지역의 강한 의지가 수소의 보급을 촉진할 것으로 예상됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모 및 예측 : 유형별, 2023-2035

제6장 시장 규모 및 예측 : 용도별, 2023-2035

제7장 시장 규모 및 예측 : 지역별, 2023-2035

제8장 기업 개요

KSM 26.03.05The Global Hydrogen Market was valued at USD 214.7 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 380.1 billion by 2035.

Market expansion is driven by the ongoing transition from fossil-fuel-based hydrogen production to low-carbon pathways, fueled by climate commitments, technological advancements, and evolving policy frameworks. Increased adoption of hydrogen in energy-intensive industries and in chemical manufacturing, including ammonia and methanol production, is creating strong growth momentum. Companies are increasingly focusing on blue hydrogen solutions, combining natural gas with carbon capture and storage (CCS) to minimize emissions, while green hydrogen deployment is accelerating in line with decarbonization goals. Falling production costs for low-carbon hydrogen, combined with supportive government incentives and clean energy mandates, are strengthening market dynamics. China dominates global capacity, accounting for nearly two-thirds of electrolyzer installations and around 60% of production, with domestic manufacturing exceeding 20 GW annually, surpassing total global demand.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $214.7 Billion |

| Forecast Value | $380.1 Billion |

| CAGR | 5.9% |

The grey hydrogen segment accounted for 72.1% share in 2025, due to continued reliance on conventional refining and crude oil consumption. However, the high carbon intensity of steam methane reforming is accelerating the shift toward green hydrogen. Pressure to reduce greenhouse gas emissions and meet sustainability targets is prompting industries to explore low-emission hydrogen alternatives, creating new growth opportunities.

The petroleum refinery sector is expected to reach USD 250 billion by 2035, driven by increasing integration of hydrogen in desulfurization processes. Hydrogen remains essential for reducing sulfur content in fuels, and refineries are progressively adopting green hydrogen to align with net-zero ambitions. This ongoing transformation is supporting broader market growth.

North America Hydrogen Market held 12.1% share in 2025, supported by government-led initiatives and clean energy policies. Regions like California are spearheading fuel cell vehicle deployment and infrastructure expansion, while Canada is positioning itself as a major clean hydrogen exporter to global markets. Strong regional commitments to decarbonization, energy transition, and technological innovation are expected to stimulate hydrogen adoption.

Key players in the Global Hydrogen Market include Air Liquide, Air Products & Chemicals, Ally Hi Tech, Ballard Power Systems, Caloric, Claind, Cummins, ENGIE, HyGear, Infinite Green Energy, Iwatani Corporation, Linde, Mahler AGS, McPhy Energy, Messer, Nel ASA, Nuvera Fuel Cells, Plug Power, Resonac Holdings Corporation, Taiyo Nippon Sanso Corporation, Teledyne Technologies Incorporated, and Xebec Adsorption. Companies are strengthening their market presence by investing in research and development to improve electrolyzer efficiency, scaling low-carbon hydrogen production, and forming strategic partnerships across energy and industrial sectors. Firms are focusing on developing both green and blue hydrogen solutions to meet emerging regulatory requirements and sustainability targets. Additionally, market participants are expanding global manufacturing footprints, building strategic supply chains, and enhancing technology portfolios to support fuel cell applications, industrial usage, and export opportunities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.3.1 Key trends for market estimates

- 1.3.1.1 Quantified market impact analysis

- 1.3.1.2 Mathematical impact of growth parameters on forecast

- 1.3.1 Key trends for market estimates

- 1.4 Primary research & validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2023 - 2035

- 2.2 Business trends

- 2.3 Type trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Price trend analysis

- 3.5.1 By capacity

- 3.5.2 By region

- 3.6 Cost structure analysis

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Legal factors

- 3.9 Emerging opportunities and trends

- 3.9.1 Digitization & IoT integration

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Type, 2023 - 2035 (USD Billion & MT)

- 5.1 Key trends

- 5.2 Grey

- 5.3 Blue

- 5.4 Green

Chapter 6 Market Size and Forecast, By Application, 2023 - 2035 (USD Billion & MT)

- 6.1 Key trends

- 6.2 Petroleum refinery

- 6.3 Chemical

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2023 - 2035 (USD Billion & MT)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Netherlands

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 Iran

- 7.5.3 UAE

- 7.5.4 South Africa

- 7.5.5 Qatar

- 7.5.6 Kuwait

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 Air Liquide

- 8.2 Air Products & Chemicals

- 8.3 Ally Hi Tech

- 8.4 Ballard Power Systems

- 8.5 Caloric

- 8.6 Claind

- 8.7 Cummins

- 8.8 ENGIE

- 8.9 HyGear

- 8.10 Infinite Green Energy

- 8.11 Iwatani Corporation

- 8.12 Linde

- 8.13 Mahler AGS

- 8.14 Mcphy Energy

- 8.15 Messer

- 8.16 Nel ASA

- 8.17 Nuvera Fuel Cells

- 8.18 Plug Power

- 8.19 Resonac Holdings Corporation

- 8.20 Taiyo Nippon Sanso Corporation

- 8.21 Teledyne Technologies Incorporated

- 8.22 Xebec Adsorption