|

시장보고서

상품코드

1959275

파바빈 원료 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Faba Bean Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

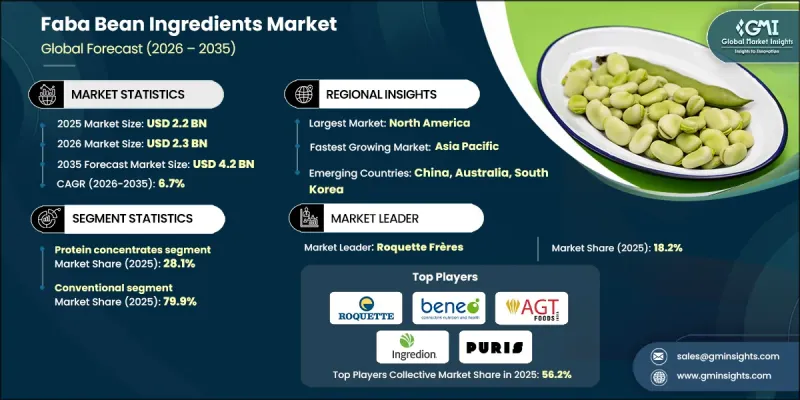

세계의 파바빈 원료 시장은 2025년에 22억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 6.7%로 성장하여 42억 달러에 이를 것으로 예측됩니다.

파바빈 원료는 고단백질 함량, 풍부한 식이섬유, 우수한 영양 프로파일로 평가받는 콩과 식물 'Vicia faba'를 원료로 사용했습니다. 이러한 특성으로 인해 식품 제조, 동물 영양, 양식용 배합사료 등 다양한 분야에서 사용하기에 적합합니다. 세계 콩 원료 시장의 성장은 지속 가능한 단백질 공급원으로의 전환, 영양에 대한 인식 증가, 동물성 대체품에 대한 의존도 감소에 힘입어 지속적으로 성장하고 있습니다. 질소 고정 작용을 통해 토양 건강을 자연스럽게 지원하고, 비료 사용량 억제에 기여함으로써 지속가능성의 매력을 높이고 있습니다. 또한, 대두나 유단백질에 비해 알레르겐을 포함하지 않는 특성도 채용 확대를 촉진하고 있습니다. 북미는 강력한 가공 능력, 성숙한 공급망, 혁신을 지원하는 유리한 규제 환경으로 인해 계속해서 큰 점유율을 차지하고 있습니다. 한편, 아시아태평양은 식물 유래 가공에 대한 투자가 가속화되고, 건강 및 친환경 제품에 대한 소비자의 관심이 높아지면서 가장 빠른 성장세를 보이고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 금액 | 22억 달러 |

| 예측 금액 | 42억 달러 |

| CAGR | 6.7% |

단백질 농축물 부문은 2025년 28.1%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 6.7%의 성장률을 보일 것으로 전망됩니다. 이 원료들은 영양 균형, 비용 효율성, 식품 배합의 다양성으로 인해 카테고리를 선도하고 있습니다. 단백질 농축물은 높은 수준의 천연 단백질을 유지하면서 식감, 결합력, 안정성을 향상시키는 기능적 이점을 제공합니다. 식물성 식품의 배합과 영양을 중시하는 제품에 대한 적합성이 강한 수요를 뒷받침하고 있습니다. 분리물에 비해 농축물은 더 복잡한 가공이 필요하지 않기 때문에 제조업체는 비용을 보다 효과적으로 관리하고 확장성을 유지할 수 있습니다.

재래식 부문은 확립된 재배 방식과 광범위한 가용성에 힘입어 2025년 79.9%의 점유율을 차지할 것으로 예측됩니다. 전통적인 농법과 대규모 가공 인프라의 조합은 안정적인 공급과 저비용 생산을 실현하여 제조업체와 최종 사용자 모두에게 이익을 가져다줍니다. 이러한 요소들이 세계 시장에서 기존 제품의 우위를 지속적으로 강화하고 있습니다. 한편, 유기농 콩 원료는 규모는 작지만 빠르게 성장하고 있는 분야로, 투명성, 지속 가능한 농업, 클린 라벨 조달에 대한 소비자의 관심이 높아지는 추세에 따라 주목받고 있습니다.

북미의 대두 원료 시장은 2026년부터 2035년까지 연평균 6.6%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 이 지역의 성장은 식품, 화장품, 의약품 분야에서 식물 유래 원료의 사용 확대를 반영하고 있습니다. 합성 원료의 환경적 영향에 대한 우려 증가와 지속 가능한 원료에 대한 인식의 확대는 업계 전반의 조달 및 배합 결정에 지속적으로 영향을 미치고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 원료 유형별, 2022-2035년

제6장 시장 추산·예측 : 성질별, 2022-2035년

제7장 시장 추산·예측 : 용도별, 2022-2035년

제8장 시장 추산·예측 : 유통 채널별, 2022-2035년

제9장 시장 추산·예측 : 지역별, 2022-2035년

제10장 기업 개요

LSH 26.03.26The Global Faba Bean Ingredients Market was valued at USD 2.2 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 4.2 billion by 2035.

Faba bean ingredients originate from the Vicia faba crop, a legume valued for its high protein concentration, rich fiber content, and strong nutritional profile. These characteristics make the ingredient suitable across food manufacturing, animal nutrition, and aquaculture formulations. Growth across the global faba bean ingredients market remains driven by a shift toward sustainable protein sources, heightened awareness of nutrition, and declining reliance on animal-derived alternatives. Faba beans naturally support soil health by fixing nitrogen, which helps limit fertilizer usage and strengthens their sustainability appeal. Their allergen-free profile further improves adoption when compared with soy or dairy proteins. North America continues to account for a significant share due to strong processing capabilities, mature supply networks, and favorable regulatory conditions that support innovation. Meanwhile, Asia-Pacific records the fastest expansion as investments in plant-based processing accelerate and consumer interest in health-conscious and eco-friendly products rises.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.2 Billion |

| Forecast Value | $4.2 Billion |

| CAGR | 6.7% |

The protein concentrates segment accounted for 28.1% share in 2025 and is forecast to grow at a CAGR of 6.7% through 2035. These ingredients lead the category due to their balanced nutrition, cost efficiency, and versatility across food formulations. Protein concentrates retain a high level of native protein while offering functional advantages that improve texture, binding, and stability. Their suitability for plant-based food formulations and nutrition-focused products supports strong demand. Compared with isolates, concentrates require less complex processing, allowing manufacturers to manage costs more effectively and maintain scalability.

The conventional faba bean ingredients segment held 79.9% share in 2025, supported by established cultivation practices and widespread availability. Traditional farming methods, combined with large-scale processing infrastructure, enable consistent supply and lower production costs, which benefits both manufacturers and end users. These factors continue to reinforce the dominance of conventional products across global markets. At the same time, organic faba bean ingredients are gaining traction within a smaller but rapidly expanding segment, as consumers increasingly prioritize transparency, sustainable agriculture, and clean-label sourcing.

North American Faba Bean Ingredients Market is expected to register a CAGR of 6.6% between 2026 and 2035. Growth across the region reflects expanding usage of plant-derived ingredients in food, cosmetic, and pharmaceutical applications. Rising concern over the environmental footprint of synthetic inputs, along with growing acceptance of sustainable raw materials, continues to influence purchasing and formulation decisions across industries.

Key companies active across the Global Faba Bean Ingredients Market include Roquette Freres, Ingredion Incorporated, AGT Food & Ingredients, Bunge, BENEO GmbH, Puris Foods, Vestkorn Milling AS, Scoular Company, Royal Ingredients Group, and Seedea. These players compete through capacity expansion, product innovation, and partnerships across food and nutrition supply chains. Companies operating in the faba bean ingredients market focus on several strategic initiatives to strengthen their market position. Many invest in advanced processing technologies to improve protein functionality, texture, and flavor while maintaining nutritional integrity. Strategic collaborations with food manufacturers and ingredient distributors help expand market reach and secure long-term supply agreements. Firms also prioritize sustainability by improving sourcing practices, reducing processing emissions, and supporting regenerative agriculture.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Ingredient type

- 2.2.3 Nature

- 2.2.4 Application

- 2.2.5 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for plant-based proteins

- 3.2.1.2 Sustainability & environmental benefits (nitrogen fixation, lower carbon footprint)

- 3.2.1.3 Allergen-free alternative to soy & dairy proteins

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Antinutritional factors (vicine, convicine) limiting consumption

- 3.2.2.2 Off-flavors & beany taste challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Organic faba bean ingredient premium segment

- 3.2.3.2 Animal feed & aquaculture protein demand

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By ingredient type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Ingredient Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Protein concentrates

- 5.3 Protein isolates

- 5.4 Faba bean flour

- 5.5 Faba bean starch

- 5.6 Faba bean fiber

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Nature, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Organic

- 6.3 Conventional

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bakery & cereals

- 7.2.1 Bread & baked goods

- 7.2.2 Pasta & noodles

- 7.2.3 Breakfast cereals

- 7.2.4 Others

- 7.3 Meat alternatives & plant-based proteins

- 7.3.1 Burgers & patties

- 7.3.2 Sausages & hot dogs

- 7.3.3 Nuggets & strips

- 7.3.4 Others

- 7.4 Dairy alternatives

- 7.4.1 Plant-based milk

- 7.4.2 Plant-based yogurt

- 7.4.3 Plant-based cheese

- 7.4.4 Plant-based ice cream

- 7.4.5 Others

- 7.5 Beverages

- 7.5.1 Protein shakes & RTD beverages

- 7.5.2 Smoothies

- 7.5.3 Nutritional drinks

- 7.5.4 Others

- 7.6 Snacks & confectionery

- 7.6.1 Protein bars & energy bars

- 7.6.2 Extruded snacks & chips

- 7.6.3 Confectionery products

- 7.6.4 Others

- 7.7 Animal feed & pet food

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Supermarkets & hypermarkets

- 8.3 Convenience stores

- 8.4 Specialty stores

- 8.5 Online retailers

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 AGT Food & Ingredients

- 10.2 BENEO GmbH

- 10.3 Bunge

- 10.4 Ingredion Incorporated

- 10.5 Puris Foods

- 10.6 Roquette Freres

- 10.7 Royal Ingredients Group

- 10.8 Scoular Company

- 10.9 Seedea

- 10.10 Vestkorn Milling AS