|

시장보고서

상품코드

1959302

바이오 폴리아미드 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Bio-Based Polyamide Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

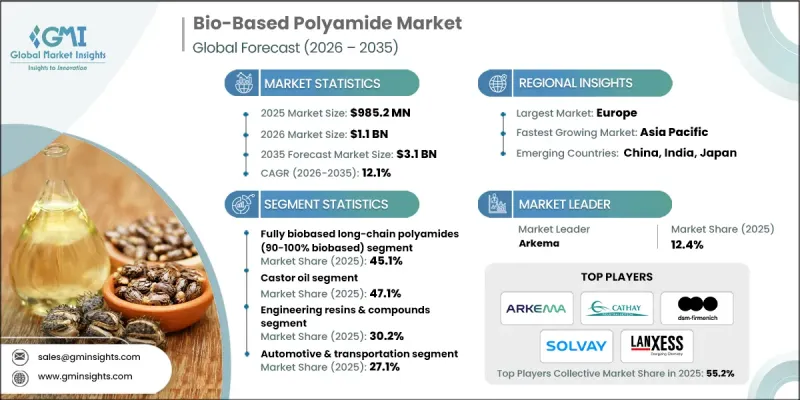

세계의 바이오 폴리아미드 시장은 2025년에 9억 8,520만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 12.1%로 성장하여 31억 달러에 이를 것으로 예측됩니다.

시장 성장은 산업 밸류체인 전반에 걸쳐 지속 가능하고 환경 친화적인 소재에 대한 수요 증가에 의해 주도되고 있습니다. 바이오 폴리아미드는 석유 유래 폴리머를 대체할 수 있는 소재로서 화석연료 의존도를 낮추고 전반적인 탄소배출량 감축을 위한 노력을 뒷받침하고 있습니다. 이 소재들은 까다로운 사용 조건에 적합한 높은 기계적 특성, 내화학성, 열 안정성 등 기존 폴리아미드와 동등하거나 그 이상의 고성능 특성을 갖도록 설계되었습니다. 온실 가스 배출량 감소로 인한 환경 프로파일 개선과 엄격한 규제 프레임워크에 대한 적합성은 제조업체와 환경 친화적인 구매자 모두에게 매력적인 선택이 될 수 있습니다. 또한, 기업의 지속가능성 목표, 탄소 감축 이니셔티브, 에코 라벨 및 환경 인증 요건을 준수하는 것도 채택을 촉진하고 있습니다. 그 결과, 바이오 폴리아미드는 다양한 산업 분야에서 보급이 확대되고 있으며, 장기적인 시장 확대가 강화되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 9억 8,520만 달러 |

| 예측 금액 | 31억 달러 |

| CAGR | 12.1% |

바이오 함량이 90%에서 100%인 완전 바이오 장쇄 폴리아미드는 2025년 45.1%의 점유율을 차지하며 2035년까지 연평균 복합 성장률(CAGR) 12.2%를 나타낼 것으로 예측됩니다. 이 부문은 재생 가능한 원료 조달 기술 및 고분자 가공 기술의 발전과 더불어 우수한 환경성과 신뢰성 높은 기능성을 겸비한 소재에 대한 수요 증가에 따른 수혜를 받고 있습니다. 이러한 폴리아미드는 지속가능성과 내구성이 동시에 요구되는 응용 분야에서 점점 더 선호되는 추세입니다.

피마자유 부문은 2025년 47.1%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 12.2%의 성장률을 보일 것으로 전망됩니다. 원료의 재생 가능성, 안정적인 공급 확보, 우수한 성능 특성으로 인해 피마자유 유래 폴리아미드는 널리 사용되고 있습니다. 가공 효율과 폴리머 설계의 지속적인 개선으로 비용 경쟁력이 향상되어 여러 최종 용도 분야에서 채택이 확대되고 있습니다.

북미 바이오 폴리아미드 시장은 2025년 21.1%의 점유율을 차지하며, 지속적으로 가속화된 성장세를 보이고 있습니다. 이 지역은 환경 정책의 지원, 지속 가능한 소재에 대한 인식 증가, 제조업 전반에 걸친 강력한 채용의 혜택을 누리고 있습니다. 지속적인 연구 활동과 혁신 중심의 제품 개발은 지역 시장에서의 성과를 더욱 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 폴리아미드 유형별, 2022-2035

제6장 시장 추산 및 예측 : 원료원별, 2022-2035

제7장 시장 추산 및 예측 : 용도별, 2022-2035

제8장 시장 추산 및 예측 : 최종 용도별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.03.18The Global Bio-Based Polyamide Market was valued at USD 985.2 million in 2025 and is estimated to grow at a CAGR of 12.1% to reach USD 3.1 billion by 2035.

Market growth is influenced by rising demand for sustainable, low-impact materials across industrial value chains. Bio-based polyamides are increasingly being adopted as alternatives to petroleum-derived polymers, supporting efforts to reduce fossil fuel dependence and lower overall carbon emissions. These materials are designed to deliver high-performance characteristics that meet or exceed those of conventional polyamides, including strong mechanical properties, chemical resistance, and thermal stability suitable for demanding operating conditions. Their reduced greenhouse gas emissions improved environmental profile, and alignment with strict regulatory frameworks makes them attractive to manufacturers and environmentally conscious buyers alike. Adoption is also being supported by corporate sustainability targets, carbon reduction initiatives, and compliance with eco-labeling and environmental certification requirements. As a result, bio-based polyamides are gaining traction across a wide range of industrial applications, reinforcing long-term market expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $985.2 Million |

| Forecast Value | $3.1 Billion |

| CAGR | 12.1% |

The fully bio-based long-chain polyamides with a bio-based content of 90% to 100% accounted for 45.1% share in 2025 and are expected to grow at a CAGR of 12.2% through 2035. This segment is benefiting from advances in renewable feedstock sourcing and polymer processing technologies, combined with increasing preference for materials that offer both strong environmental credentials and reliable functional performance. These polyamides are increasingly favored in applications requiring durability alongside sustainability.

The castor oil segment held a 47.1% share in 2025 and is projected to grow at a CAGR of 12.2% from 2026 to 2035. Castor oil-based polyamides are gaining widespread acceptance due to the renewable nature of the feedstock, consistent supply availability, and favorable performance characteristics. Continuous improvements in processing efficiency and polymer design are enhancing cost competitiveness and expanding adoption across multiple end-use sectors.

North America Bio-Based Polyamide Market accounted for a 21.1% share in 2025 and continues to demonstrate accelerated growth. The region benefits from supportive environmental policies, rising awareness around sustainable materials, and strong adoption across manufacturing industries. Ongoing research activity and innovation-driven product development are further strengthening regional market performance.

Key companies operating in the Global Bio-Based Polyamide Market include Arkema, DSM, Firmenich, Evonik Industries, LANXESS, Solvay, Avient Corporation, Domo Chemicals, Cathay Biotech, AKRO PLASTIC GmbH, NUREL, and Tekmar Group (TEKMA). Companies in the bio-based polyamide market are reinforcing their market position through strategic investments in research and development to enhance material performance and expand application scope. Many players are prioritizing partnerships with downstream manufacturers to accelerate commercialization and adoption. Capacity expansions, supply chain optimization, and improved access to renewable feedstocks are helping firms meet rising demand. Sustainability certifications and compliance with environmental regulations are being leveraged to strengthen brand credibility. Geographic expansion into high-growth regions and diversification of product portfolios are also key strategies supporting long-term competitiveness and market foothold.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Polyamide type

- 2.2.3 Feedstock sources

- 2.2.4 Application

- 2.2.5 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Polyamide Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Fully biobased long-chain polyamides (90-100% biobased)

- 5.3 High biobased content long-chain polyamides (60-89% biobased)

- 5.4 Moderate biobased content specialty polyamides (25-59% biobased)

Chapter 6 Market Estimates and Forecast, By Feedstock Source, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Castor oil-derived bio-based polyamides

- 6.3 Corn-derived bio-based polyamides

- 6.4 Sugarcane & inedible biomass-derived bio-based polyamides

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Engineering resins & compounds

- 7.3 Textile fibers & filaments

- 7.4 Films & flexible packaging

- 7.5 Extruded profiles & tubes

- 7.6 Additive manufacturing powders & filaments

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Automotive & transportation

- 8.3 Textiles & apparel

- 8.4 Electronics & electrical

- 8.5 Packaging & consumer goods

- 8.6 Construction & building materials

- 8.7 Industrial machinery & water management

- 8.8 Medical & pharmaceutical

- 8.9 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 AKRO-PLASTIC GmbH

- 10.2 Arkema

- 10.3 Avient Corporation

- 10.4 Cathay Biotech

- 10.5 Domo Chemicals

- 10.6 DSM-Firmenich

- 10.7 Evonik Industries

- 10.8 LANXESS

- 10.9 NUREL

- 10.10 Solvay

- 10.11 Tekmar Group (TEKMA)