|

시장보고서

상품코드

1959303

기능성 식품용 포스트바이오틱 원료 시장 성장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Postbiotic Ingredients in Functional Foods Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

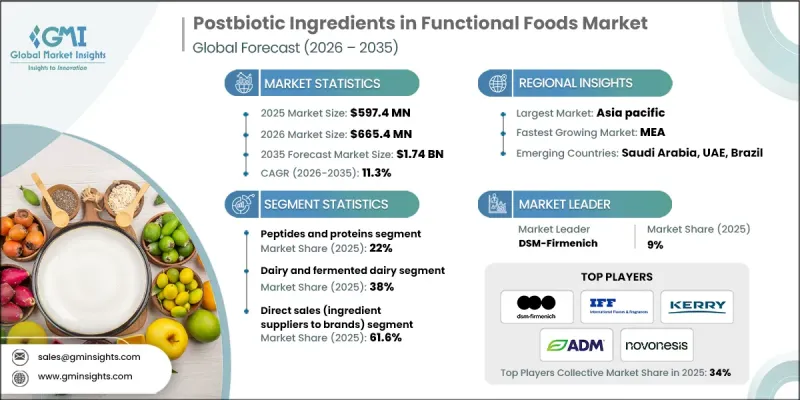

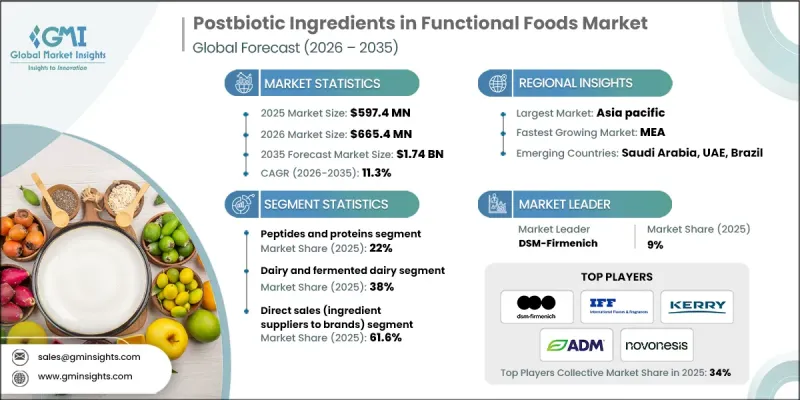

세계의 기능성 식품용 포스트바이오틱 원료 시장은 2025년에 5억 9,740만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 11.3%로 성장하여 17억 4,000만 달러에 이를 것으로 예측되고 있습니다.

이러한 성장은 장 건강 및 마이크로바이옴 과학에 대한 소비자의 인식이 높아지고, 안정성이 높고 배합이 용이한 기능성 원료에 대한 수요가 증가함에 따라 성장세를 보이고 있습니다. 포스트바이오틱 원료는 식품 제조업체가 가공 공정 및 보관 기간 동안 살아있는 배양균을 유지하는 데 따르는 배합상의 어려움 없이 마이크로바이옴 관련 이점을 제공할 수 있는 능력을 부여합니다. 그 결과, 브랜드들은 소화기 건강 및 면역 지원과 관련된 강력한 포지셔닝을 유지하면서 프로바이오틱스를 대체할 수 있는 저위험 대안으로 포스트바이오틱스를 점점 더 많이 채택하고 있습니다. 주요 지역의 규제 명확화와 영양가와 편의성을 추구하는 식품 형태의 융합이 제품 혁신을 가속화하고 있습니다. 발효 식품과 장 건강에 좋은 제품에 대한 관심이 높아지면서 수요가 더욱 강화되고 있으며, 제조업체들은 다양한 카테고리에서 마이크로바이옴을 지원하는 배합을 개발하고 있습니다. 특히 기존 생균이 안정성에 문제가 있는 용도에서 내열성 포스트바이오틱스 원료의 채용이 증가하고 있습니다. 소화기 건강에 대한 소비자의 관심이 수치화될 정도로 높아진 것이 장기적인 시장 확대를 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 5억 9,740만 달러 |

| 예측 금액 | 17억 4,000만 달러 |

| CAGR | 11.3% |

펩타이드 및 단백질 부문은 2025년 22%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 12.2%의 성장률을 보일 것으로 전망됩니다. 원료 공급업체들은 단일 성분 제공에서 펩타이드, 효소, 세포 분획, 비타민, 기타 생리활성 화합물을 결합한 다기능 블렌드로 전환하고 있습니다. 이 솔루션은 표준화된 표시를 고려한 원료로 일관된 효능, 개선된 향미 프로파일, 향상된 제조 효율성을 제공합니다. 상업적 전략은 유제품, 음료, 스낵의 전체 배합에 사용할 수 있도록 카테고리 간 호환성에 점점 더 중점을 두고 있으며, 안정성 검증 및 문서화를 통해 입증된 차별화된 기능성 표시를 지원하고 있습니다.

유제품 및 발효유 제품 응용 분야는 2025년에 38%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 10.9%의 성장률을 보일 것으로 예측됩니다. 이 부문은 발효를 기반으로 한 건강 효과와 기존 소비 습관과의 자연스러운 친화력으로 인해 여전히 중심적인 위치를 차지하고 있습니다. 제조업체들은 다양한 유제품 베이스 제품에 포스트바이오틱 원료를 배합하여 배합의 안정성을 높이고, 감각적 기대치를 손상시키지 않으면서도 일관된 기능성을 보장하고 있습니다. 전통적인 미각 프로파일을 유지하면서 소화기 건강 메시지를 강화할 수 있다는 점이 이 카테고리 내에서의 채택 확대에 계속 힘을 실어주고 있습니다.

북미 기능성 식품용 포스트바이오틱 원료 시장은 2025년 1억 5,690만 달러 규모이며, 주류 장 건강 기능성 식품의 강력한 혁신에 힘입어 2035년까지 4억 6,040만 달러에 달할 것으로 예측됩니다. 미국은 기능성 식품 브랜드와 원료 공급업체의 성숙한 생태계를 통해 지역 성장을 주도하고 있습니다. 시장 확대는 건강기능식품의 개념이 음료 및 식품 분야에 적용되는 크로스오버 현상, 소화기 건강 제품의 소매 유통망 확대, 그리고 간편한 휴대형 기능성 포맷에 대한 소비자의 높은 수용성에 의해 촉진되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 원료 유형별, 2022-2035

제6장 시장 추산 및 예측 : 식품 유형별, 2022-2035

제7장 시장 추산 및 예측 : 유통 채널별, 2022-2035

제8장 시장 추산 및 예측 : 지역별, 2022-2035

제9장 기업 개요

LSH 26.03.18The Global Postbiotic Ingredients in Functional Foods Market was valued at USD 597.4 million in 2025 and is estimated to grow at a CAGR of 11.3% to reach USD 1.74 billion by 2035.

Growth is driven by rising consumer awareness of gut health and microbiome science, alongside increasing demand for stable and easy-to-formulate functional ingredients. Postbiotic ingredients offer food manufacturers the ability to deliver microbiome-related benefits without the formulation challenges linked to maintaining live cultures during processing and shelf life. As a result, brands are increasingly turning to postbiotics as a lower-risk alternative to probiotics while maintaining strong positioning around digestive health and immune support. Regulatory clarity in key regions, combined with the convergence of nutrition and convenience-driven food formats, is accelerating product innovation. Broader interest in fermented and gut-friendly products has further strengthened demand, with manufacturers developing microbiome-supportive formulations across multiple categories. Heat-stable postbiotic ingredients are gaining traction, particularly in applications where traditional live cultures face stability limitations. Quantifiable consumer interest in digestive wellness continues to support long-term market expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $597.4 Million |

| Forecast Value | $1.74 Billion |

| CAGR | 11.3% |

The peptides and proteins segment accounted for 22% share in 2025 and is expected to grow at a CAGR of 12.2% through 2035. Ingredient suppliers are moving beyond single-component offerings toward multifunctional blends that combine peptides, enzymes, cell fractions, vitamins, and additional bioactive compounds. These solutions are positioned as standardized, label-friendly ingredients that deliver consistent potency, improved flavor profiles, and greater manufacturing efficiency. Commercial strategies increasingly emphasize cross-category compatibility, enabling use across dairy, beverage, and snack formulations while supporting differentiated functional claims backed by stability validation and documentation.

The dairy and fermented dairy applications segment held 38% share in 2025 and is forecast to grow at a CAGR of 10.9% by 2035. This segment remains central due to its natural alignment with fermentation-based health narratives and established consumption habits. Manufacturers are incorporating postbiotic ingredients into a wide range of dairy-based products to enhance formulation stability and ensure consistent functional positioning without compromising sensory expectations. The ability to reinforce digestive health messaging while maintaining traditional taste profiles continues to strengthen adoption within this category.

North America Postbiotic Ingredients in Functional Foods Market accounted for USD 156.9 million in 2025 and is projected to reach USD 460.4 million by 2035, supported by strong innovation in mainstream gut-health functional foods. The United States leads regional growth through a well-developed ecosystem of functional food brands and ingredient suppliers. Market expansion benefits from the crossover of dietary supplement concepts into food and beverage applications, widespread retail availability of digestive wellness products, and high consumer acceptance of convenient, on-the-go functional formats.

Key companies operating in the Global Postbiotic Ingredients in Functional Foods Market include DSM-Firmenich, IFF (International Flavors & Fragrances), ADM, Kerry Group, BASF, Novonesis, Cargill, Givaudan, Evonik, and DuPont (IFF legacy Danisco). Companies in the Postbiotic Ingredients in Functional Foods Market are strengthening their competitive position through targeted research and development, strategic partnerships with food manufacturers, and portfolio diversification. Many players are investing in clinically supported formulations to substantiate claims related to digestive and immune health. Expanding multifunctional ingredient blends enhances cross-category application flexibility and improves formulation efficiency for brand owners. Firms are also prioritizing regulatory alignment and clean-label positioning to meet evolving consumer expectations. Strategic acquisitions and collaborations are enabling companies to broaden their geographic reach and accelerate innovation pipelines.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 ingredient type

- 2.2.3 Food type

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By ingredient type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Short-chain fatty acids

- 5.3 Cell wall components

- 5.4 Exopolysaccharides

- 5.5 Enzymes

- 5.6 Peptides and proteins

- 5.7 Vitamins and bioactives

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Food type, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dairy and fermented dairy

- 6.2.1 Yogurt

- 6.2.2 Kefir

- 6.2.3 Cultured milk drinks

- 6.2.4 Cheese and fermented dairy desserts

- 6.3 Non-dairy beverages

- 6.3.1 Functional water

- 6.3.2 Juices and juice drinks

- 6.3.3 Ready-to-drink tea/coffee

- 6.3.4 Plant-based fermented drinks

- 6.4 Bakery and cereals

- 6.4.1 Bread and buns

- 6.4.2 Breakfast cereals and granola

- 6.4.3 Nutrition bars

- 6.5 Confectionery

- 6.5.1 Gummies and jellies

- 6.5.2 Chocolate

- 6.5.3 Candies and lozenges

- 6.6 Infant and child nutrition

- 6.6.1 Infant formula

- 6.6.2 Follow-on formula

- 6.6.3 Toddler foods

- 6.7 Medical and clinical nutrition

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Distribution channel, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Direct sales (ingredient suppliers to brands)

- 7.3 Distributors/agents

- 7.4 Online B2B platforms

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 IFF (International Flavors & Fragrances)

- 9.2 DSM-Firmenich

- 9.3 ADM

- 9.4 Kerry Group

- 9.5 BASF

- 9.6 Evonik

- 9.7 Novonesis

- 9.8 DuPont (IFF legacy Danisco)

- 9.9 Cargill

- 9.10 Givaudan