|

시장보고서

상품코드

1959305

코팅 및 세정용 바이오 용제 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Bio-Based Solvents for Coatings and Cleaning Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

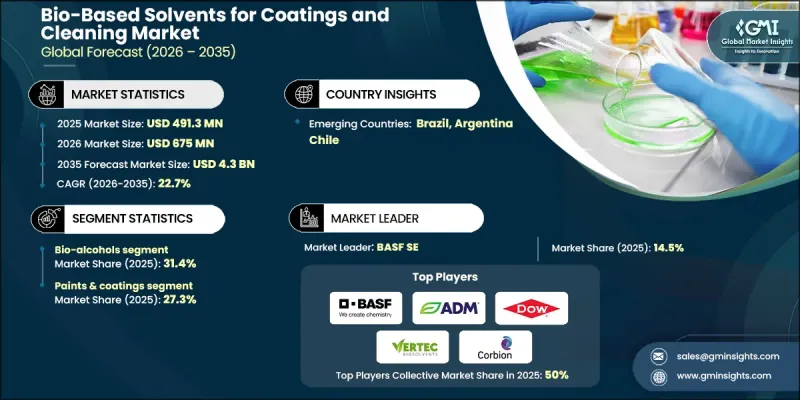

세계의 코팅 및 세정용 바이오 용제 시장은 2025년에 4억 9,130만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 22.7%로 성장하여 43억 달러에 이를 것으로 예측되고 있습니다.

산업이 지속 가능하고 저독성, 저VOC 화학 대체품으로 전환함에 따라 시장은 빠르게 변화하고 있습니다. 환경 영향과 작업장 안전에 대한 소비자의 인식이 높아지면서 기존 석유화학 용제에서 재생 가능한 대체품으로의 전환이 가속화되고 있습니다. 주요 경제권의 규제 당국은 화학물질 안전 프레임워크를 강화하여 제조 및 유지보수 작업에서 고VOC 물질의 사용을 제한하고 있습니다. 확립된 환경 및 화학물질 관리 정책에 따른 컴플라이언스 요구사항으로 인해 제조업체는 보다 안전한 배합을 채택해야 하는 상황에 처해 있습니다. 그 결과, 젖산 에스테르, 재생 가능한 알코올, 테르펜계 용매, 글리세롤 유래 화합물 등 바이오 용매에 대한 수요가 크게 증가하고 있습니다. 이러한 대체품은 환경 부하를 줄이면서 강력한 용해 성능, 제어된 증발 특성, 다양한 기판과의 호환성을 제공합니다. 산업용도료, 표면 처리, 자동차 재도장, 항공우주 유지보수, 고성능 건축용도로의 사용 확대로 시장 성장이 더욱 강화되고 있습니다. 이러한 분야에서는 엄격한 기술 기준을 충족하는 효율적이고 고순도 용매 시스템이 요구되기 때문입니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 금액 | 4억 9,130만 달러 |

| 예측 금액 | 43억 달러 |

| CAGR | 22.7% |

바이오 알코올 부문은 2025년 31.4%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 21.3%의 성장률을 보일 것으로 전망됩니다. 이 제품은 범용성, 광범위한 산업 적용성, 기존 석유계 용매에 비해 비용 경쟁력으로 인해 시장에서의 입지를 확고히 하고 있습니다. 재생 가능한 알코올 기반 용매는 효과적인 용해 특성과 균형 잡힌 증발 속도를 제공하기 때문에 코팅, 표면 처리, 산업용 세정제 배합에 적합합니다. 이 부문은 이미 구축된 대규모 생산 인프라와 신뢰할 수 있는 재생 가능한 원료 공급을 통해 세계 시장에서공급 안정성과 상업적 확장성을 확보하고 있습니다.

페인트 및 코팅 제조 부문은 2025년 27.3%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 21.7%를 나타낼 것으로 예측됩니다. 배합 균일성, 분산 효율, 점도 조절, 경화 성능 등을 위해 용매에 대한 의존도가 높은 이 산업은 바이오 대체품의 주요 소비 분야로 자리매김하고 있습니다. 제조업체들은 엄격한 환경 규제에 대응하고 총 VOC 배출량을 줄이기 위해 재생 가능한 용매를 제품 라인에 통합하는 데 박차를 가하고 있습니다. 친환경 코팅 기술로의 전환으로 기존 용제에서 식물성 알코올, 에스테르계 용액, 글리세롤계 화학물질로 대체되면서 가치사슬 전반의 지속가능성을 위한 노력이 강화되고 있습니다.

북미 코팅 및 세정용 바이오 용제 시장은 2025년 31.2%의 점유율을 차지할 것으로 예상되며, 이는 이 지역의 강력한 성장세를 반영합니다. 이 시장은 성숙한 산업 생태계, 적극적인 환경 정책, 엄격한 대기질 기준의 시행으로 뒷받침되고 있습니다. 생산 및 유지보수 활동에서 고VOC 용제 사용을 제한하는 규제 조치로 인해 재생 가능한 대체품의 채택이 촉진되고 있습니다. 또한, 확립된 바이오리파이닝 기술을 통해 알코올계 및 글리세롤 유래 용매의 지역 밀착형 공급망을 구축하고 있는 점도 강점입니다. 지속적인 청정 기술 프로그램과 그린 케미스트리 이니셔티브는 페인트, 특수 화학 및 산업 공정 분야에서 시장 침투를 더욱 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 유형별, 2022-2035년

제6장 시장 추산·예측 : 최종 이용 산업별, 2022-2035년

제7장 시장 추산·예측 : 지역별, 2022-2035년

제8장 기업 개요

LSH 26.03.26The Global Bio-Based Solvents for Coatings and Cleaning Market was valued at USD 491.3 million in 2025 and is estimated to grow at a CAGR of 22.7% to reach USD 4.3 billion by 2035.

The market is undergoing rapid transformation as industries shift toward sustainable, low-toxicity, and low-VOC chemical alternatives. Growing consumer awareness regarding environmental impact and workplace safety is accelerating the replacement of conventional petrochemical solvents with renewable substitutes. Regulatory authorities across major economies are tightening chemical safety frameworks and limiting the use of high-VOC substances in manufacturing and maintenance operations. Compliance requirements under established environmental and chemical control policies are pushing manufacturers to adopt safer formulations. As a result, demand for bio-based solvents, including lactate esters, renewable alcohols, terpene-based solvents, and glycerol-derived compounds, is rising significantly. These alternatives deliver strong solvency performance, controlled evaporation profiles, and compatibility with diverse substrates while reducing environmental footprint. Expanding use in industrial coatings, surface treatment, automotive refinishing, aerospace maintenance, and high-performance architectural applications is further strengthening market growth, as these sectors require efficient, high-purity solvent systems capable of meeting strict technical standards.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $491.3 Million |

| Forecast Value | $4.3 Billion |

| CAGR | 22.7% |

The bio-alcohols segment accounted for 31.4% share in 2025 and is expected to grow at a CAGR of 21.3% through 2035. Their strong market position is supported by versatility, wide industrial applicability, and cost competitiveness compared to traditional petroleum-based solvents. Renewable alcohol-based solvents provide effective dissolution properties and balanced evaporation rates, making them suitable for coatings, surface preparation, and industrial cleaning formulations. The segment benefits from established large-scale production infrastructure and reliable renewable feedstock availability, ensuring supply stability and commercial scalability across global markets.

The paints and coatings manufacturing segment held 27.3% share in 2025 and is projected to grow at a CAGR of 21.7% between 2026 and 2035. The industry's heavy reliance on solvents for formulation consistency, dispersion efficiency, viscosity adjustment, and curing performance positions it as a key consumer of bio-based alternatives. Manufacturers are increasingly integrating renewable solvents into product lines to meet stringent environmental regulations and reduce total VOC emissions. The transition toward eco-conscious coating technologies has accelerated the substitution of conventional solvents with plant-derived alcohols, ester-based solutions, and glycerol-based chemistries, strengthening sustainability initiatives across the value chain.

North America Bio-Based Solvents for Coatings and Cleaning Market held a 31.2% share in 2025, reflecting strong regional momentum. The market is supported by a mature industrial ecosystem, proactive environmental policies, and rigorous enforcement of air quality standards. Regulatory measures restricting high-VOC solvent usage in production and maintenance activities are encouraging the adoption of renewable alternatives. The region also benefits from established bio-refining capabilities, supporting localized supply chains for alcohol-based and glycerol-derived solvents. Ongoing clean technology programs and green chemistry initiatives are further driving market penetration across coatings, specialty chemicals, and industrial processing sectors.

Key companies operating in the Global Bio-Based Solvents for Coatings and Cleaning Market include BASF SE, Dow Inc., Archer Daniels Midland Company (ADM), Eastman Chemical Company, DuPont de Nemours, Inc., Evonik Industries AG, Clariant AG, Solvay S.A., LyondellBasell Industries N.V., Corbion N.V., Ashland Global Holdings Inc., Vertec BioSolvents, Inc., Circa Group, Florachem Corporation, and Bio Brands LLC. These industry leaders are actively competing through product innovation, sustainable sourcing strategies, and global expansion initiatives. Companies in the Bio-Based Solvents for Coatings and Cleaning Market are strengthening their competitive position by investing heavily in research and development to enhance solvent performance, purity levels, and application versatility. Strategic collaborations with coatings manufacturers and industrial formulators enable tailored product development and long-term supply agreements. Many firms are expanding bio-refining capacity to secure renewable feedstock supply and improve cost efficiency. Portfolio diversification into specialty and high-performance solvent grades supports differentiation in a competitive environment.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 End use industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Bio-Alcohols

- 5.3 Lactate Esters

- 5.4 Glycerol Derivatives

- 5.5 D-Limonene

- 5.6 2-Methyltetrahydrofuran (2-MeTHF)

- 5.7 Fatty Acid Derivatives

- 5.8 Other Bio-Based Solvents

Chapter 6 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Paints & Coatings Manufacturing

- 6.2.1 Architectural Coatings Manufacturers

- 6.2.2 Industrial Coatings Manufacturers

- 6.2.3 Specialty & Functional Coatings Manufacturers

- 6.3 Automotive & Transportation

- 6.3.1 Original Equipment Manufacturers (OEMs)

- 6.3.2 Tier-1 & Tier-2 Suppliers

- 6.3.3 Aftermarket & Refinishing Services

- 6.4 Industrial Manufacturing

- 6.4.1 Metal Fabrication & Metalworking

- 6.4.2 Machinery & Equipment Manufacturing

- 6.4.3 General Manufacturing & Assembly Operations

- 6.5 Building & Construction

- 6.5.1 Residential Construction

- 6.5.2 Commercial & Institutional Construction

- 6.5.3 Infrastructure & Civil Engineering

- 6.6 Aerospace & Defense

- 6.6.1 Commercial Aircraft Manufacturing

- 6.6.2 Military & Defense Systems

- 6.6.3 Maintenance, Repair & Overhaul (MRO)

- 6.7 Electronics & Electrical Equipment

- 6.7.1 Consumer Electronics Manufacturing

- 6.7.2 Industrial Electronics & Controls

- 6.7.3 Semiconductor & PCB Manufacturing

- 6.8 Pharmaceuticals

- 6.8.1 Active Pharmaceutical Ingredient (API) Manufacturing

- 6.8.2 Medical Devices & Diagnostics

- 6.8.3 Contract Manufacturing Organizations (CMOs)

- 6.9 Printing & Packaging

- 6.9.1 Commercial Printing

- 6.9.2 Flexible Packaging

- 6.9.3 Rigid Packaging & Labels

- 6.10 Cosmetics & Personal Care

- 6.10.1 Skincare & Haircare Products

- 6.10.2 Color Cosmetics & Fragrances

- 6.10.3 Natural & Organic Beauty Products

- 6.11 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 BASF SE

- 8.2 Archer Daniels Midland Company (ADM)

- 8.3 Ashland Global Holdings Inc.

- 8.4 Bio Brands LLC

- 8.5 Circa Group

- 8.6 Clariant AG

- 8.7 Corbion N.V.

- 8.8 Dow Inc.

- 8.9 DuPont de Nemours, Inc.

- 8.10 Eastman Chemical Company

- 8.11 Evonik Industries AG

- 8.12 Florachem Corporation

- 8.13 LyondellBasell Industries N.V.

- 8.14 Solvay S.A.

- 8.15 Vertec BioSolvents, Inc.

- 8.16 Others