|

시장보고서

상품코드

1959306

퍼스널케어용 바이오 계면활성제 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Bio-based Surfactants for Personal Care Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

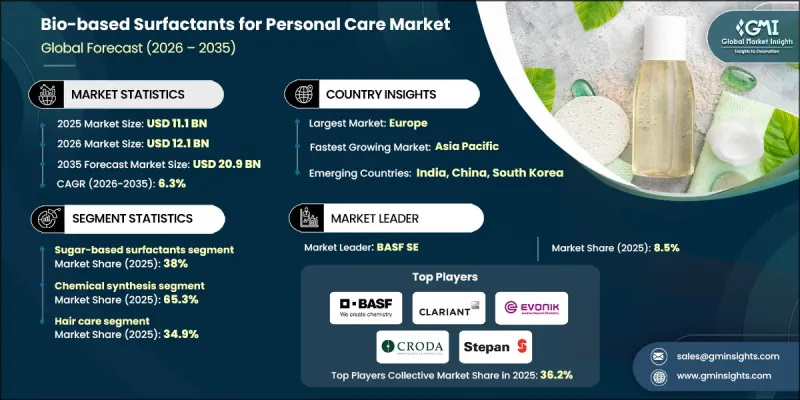

세계의 퍼스널케어용 바이오 계면활성제 시장은 2025년에 111억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 6.3%로 성장하여 209억 달러에 이를 것으로 예측되고 있습니다.

시장 확대는 뷰티 및 퍼스널케어 산업에서 지속 가능한 생분해성 원료로의 전환이 가속화되고 있음을 반영합니다. 퍼스널케어 제품에 사용되는 바이오 계면활성제는 미생물 유래 바이오 계면활성제, 아미노산 계면활성제, 당 유래 계면활성제, 바이오 에톡실레이트, 발효, 효소 처리, 재생 가능한 원료 합성을 통해 개발된 기타 식물 유래 대체품 등 다양한 재생 가능 기술 포트폴리오를 포함하고 있습니다. 포트폴리오를 포함하고 있습니다. 이들 원료는 헤어케어, 스킨케어, 구강위생, 베이비케어, 특수 미용제품에 대한 채용이 확대되고 있습니다. 환경적 지속가능성과 원료 투명성에 대한 소비자의 인식이 높아지면서 구매 결정에 큰 영향을 미치고 있습니다. 세계 각국 정부는 그린 케미스트리 프레임워크 추진, 재생 가능한 처방에 대한 혁신 지원, 친환경적인 퍼스널케어 제조 시스템으로의 전환을 촉진하는 규제 정책을 도입하고 있습니다. 유럽은 현재 주요 경제권의 강력한 규제 지원과 생산 인프라에 대한 막대한 투자에 힘입어 세계를 선도하고 있습니다. 한편, 아시아태평양은 급속한 산업 발전, 자연주의 뷰티 솔루션에 대한 관심 증가, 클린 라벨 및 친환경 퍼스널케어 제품에 대한 소비자 선호도 증가를 배경으로 고성장 지역으로 부상하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 금액 | 111억 달러 |

| 예측 금액 | 209억 달러 |

| CAGR | 6.3% |

당계면활성제 부문은 2025년 38%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 6.7%의 성장률을 보일 것으로 전망됩니다. 그 존재감이 높아진 것은 순한 성능 특성, 높은 생분해성, 민감한 피부용 포뮬러에 대한 적합성 때문입니다. 이러한 계면활성제는 천연 및 유기농 제품과 잘 어울리기 때문에 다양한 퍼스널케어 분야에서 널리 사용되고 있습니다. 제조업체들은 클린 뷰티 기준에 부합하면서도 효과적인 세정력을 발휘하는 설탕 유래 솔루션을 선호하고 있습니다. 순한 식물 유래 성분에 대한 수요가 증가함에 따라 차세대 화장품 제형에 당계면활성제의 통합이 가속화되고 있습니다.

재생 가능한 원료로부터의 화학 합성 부문은 2025년에 65.3%의 점유율을 차지하고 2035년까지 연평균 복합 성장률(CAGR) 6.2%를 나타낼 것으로 예측됩니다. 이 제조 공정은 아미노산 유래 변이체, 당계 계면활성제, 바이오 에톡실레이트 등 다양한 바이오 계면활성제 생산에 중요한 역할을 하고 있습니다. 이 방식은 확장성, 운영 효율성, 안정적인 생산 품질로 잘 알려진 확립된 화학 기술을 통해 가공된 재생 가능한 원료를 활용합니다. 신흥 생명공학 플랫폼과 비교하여, 이 방법은 높은 상업적 타당성과 비용 우위를 제공하며, 대규모 생산에 있어 매력적입니다. 재생 가능한 원료 공급망에 대한 투자 증가와 신뢰할 수 있는 바이오 계면활성제 생산에 대한 수요 증가는 이 기술 플랫폼의 우위를 더욱 강화하고 있습니다.

북미 퍼스널케어용 바이오 계면활성제 시장은 2026년부터 2035년까지 연평균 6.7%의 성장률을 보일 것으로 예측됩니다. 이 지역의 성장은 지속 가능한 원료 개발의 혁신과 그린 케미컬 원칙에 따른 발효 기반 기술의 채택 확대에 의해 촉진되고 있습니다. 기존 계면활성제의 환경오염에 대한 소비자들의 우려가 커지면서 각 브랜드들은 생분해성 및 식물성 대체품을 활용한 제품 재설계를 진행하고 있습니다. 클린 뷰티 운동의 확산과 환경 친화적 제조를 장려하는 규제가 결합되어 헤어케어, 스킨케어, 특수 퍼스널케어 부문 수요를 더욱 자극하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 제품 유형별, 2022-2035년

제6장 시장 추산·예측 : 기술 유형별, 2022-2035년

제7장 시장 추산·예측 : 용도별, 2022-2035년

제8장 시장 추산·예측 : 지역별, 2022-2035년

제9장 기업 개요

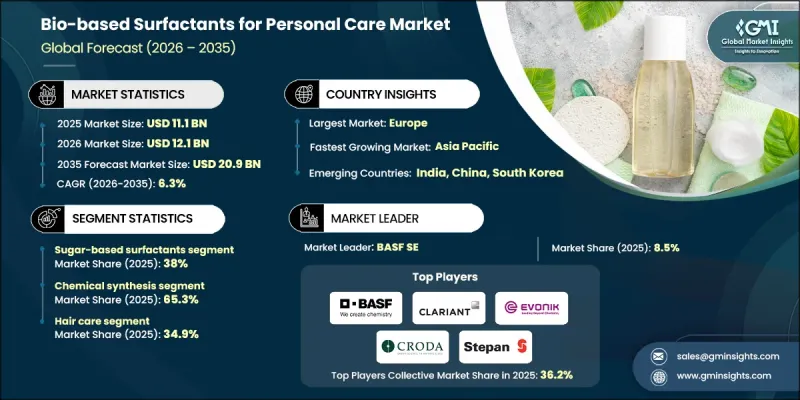

LSH 26.03.26The Global Bio-based Surfactants for Personal Care Market was valued at USD 11.1 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 20.9 billion by 2035.

Market expansion reflects the accelerating shift toward sustainable and biodegradable ingredients within the beauty and personal care industry. Bio-based surfactants used in personal care formulations include a broad portfolio of renewable technologies such as microbial-derived biosurfactants, amino acid-based surfactants, sugar-derived surfactants, bio-based ethoxylates, and other plant-origin alternatives developed through fermentation, enzymatic processing, and renewable feedstock synthesis. These ingredients are increasingly incorporated into hair care, skin care, oral hygiene, baby care, and specialty beauty products. Rising consumer awareness of environmental sustainability and ingredient transparency is significantly influencing purchasing decisions. Governments worldwide are promoting green chemistry frameworks, funding innovation in renewable formulations, and introducing regulatory policies that encourage the transition toward eco-conscious personal care manufacturing systems. Europe currently leads the global landscape, supported by strong regulatory backing and substantial investment in production infrastructure across major economies. Meanwhile, Asia Pacific is emerging as a high-growth region, driven by rapid industrial advancement, increased focus on natural beauty solutions, and expanding consumer preference for clean-label and environmentally responsible personal care products.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.1 Billion |

| Forecast Value | $20.9 Billion |

| CAGR | 6.3% |

The sugar-based surfactants segment accounted for 38% share in 2025 and is forecast to grow at a CAGR of 6.7% through 2035. Their growing prominence is attributed to their mild performance profile, high biodegradability, and suitability for sensitive skin formulations. These surfactants are widely adopted across diverse personal care categories due to their compatibility with natural and organic product positioning. Manufacturers favor sugar-derived solutions for their ability to deliver effective cleansing while aligning with clean beauty standards. The increasing demand for gentle, plant-based ingredients is accelerating the integration of sugar-based surfactants into next-generation cosmetic formulations.

The chemical synthesis from renewable feedstocks segment held 65.3% share in 2025 and is anticipated to grow at a CAGR of 6.2% by 2035. This production pathway plays a critical role in manufacturing a wide array of bio-based surfactants, including amino acid-derived variants, sugar-based surfactants, and bio-based ethoxylates. The approach leverages renewable raw materials processed through established chemical technologies known for scalability, operational efficiency, and consistent output quality. Compared to emerging biotechnology platforms, this method offers strong commercial viability and cost advantages, making it attractive for large-scale production. Rising investments in renewable feedstock supply chains and growing demand for dependable bio-based surfactant manufacturing are reinforcing the dominance of this technology platform.

North America Bio-based Surfactants for Personal Care Market is expected to register a CAGR of 6.7% between 2026 and 2035. Growth in the region is fueled by innovation in sustainable ingredient development and increased adoption of fermentation-based technologies aligned with green chemistry principles. Consumer concern regarding the ecological footprint of conventional surfactants is prompting brands to reformulate products with biodegradable and plant-derived alternatives. Expanding clean beauty movements, combined with regulatory encouragement for environmentally responsible manufacturing, are further stimulating demand across hair care, skin care, and specialty personal care segments.

Key companies operating in the Global Bio-based Surfactants for Personal Care Market include BASF SE, Croda International Plc, Clariant AG, Evonik Industries AG, Solvay / Syensqo, Galaxy Surfactants Ltd, Kao Corporation, Ajinomoto Co., Inc., Stepan Company, Innospec, Seppic, Lonza, Sino Lion, Miwon Commercial, and Holiferm Ltd. These companies are actively shaping competitive dynamics through innovation, sustainability commitments, and strategic expansion initiatives. Companies in the bio-based surfactants for personal care market are strengthening their market position by investing in advanced research and development focused on high-performance, biodegradable formulations. Strategic collaborations with beauty brands enable the co-creation of customized ingredients tailored to clean-label demands. Many firms are expanding manufacturing capacity for renewable feedstocks while improving supply chain transparency to meet sustainability benchmarks. Portfolio diversification into specialty and premium-grade surfactants supports differentiation in a competitive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Technology type

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Microbial biosurfactants

- 5.2.1 Glycolipids

- 5.2.1.1 Sophorolipids

- 5.2.1.2 Rhamnolipids

- 5.2.1.3 Mannosylerythritol lipids (MELs)

- 5.2.1.4 Trehalolipids

- 5.2.2 Lipopeptides

- 5.2.2.1 Surfactin

- 5.2.2.2 Iturin

- 5.2.2.3 Lichenysin

- 5.2.1 Glycolipids

- 5.3 Sugar-based surfactants

- 5.3.1 Alkyl polyglucosides (APGs)

- 5.3.2 Glucamides

- 5.3.3 Sucrose esters

- 5.3.4 Sorbitan esters

- 5.4 Amino acid-derived surfactants

- 5.4.1 Glutamates

- 5.4.2 Glycinates

- 5.4.3 Isethionates

- 5.4.4 Sarcosinates

- 5.4.5 Taurates

- 5.5 Bio-based ethoxylates

- 5.5.1 Bio-based alcohol ethoxylates

- 5.5.2 Bio-based polysorbates

- 5.5.3 Bio-based PEG derivatives

- 5.5.4 Bio-based castor oil ethoxylates

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Technology Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Microbial fermentation technology

- 6.3 Chemical synthesis from renewable feedstocks

- 6.4 Enzymatic synthesis

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Hair care

- 7.3 Skin care

- 7.4 Oral care

- 7.5 Baby care

- 7.6 Specialty personal care

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Clariant AG

- 9.3 Evonik Industries AG

- 9.4 Croda International Plc

- 9.5 Kao Corporation

- 9.6 Stepan Company

- 9.7 Sino Lion

- 9.8 Galaxy Surfactants Ltd

- 9.9 Ajinomoto Co., Inc.

- 9.10 Seppic

- 9.11 Lonza

- 9.12 Innospec

- 9.13 Holiferm Ltd

- 9.14 Solvay / Syensqo

- 9.15 Miwon Commercial