|

시장보고서

상품코드

1959327

경장 영양제 원료 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Enteral Nutrition Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

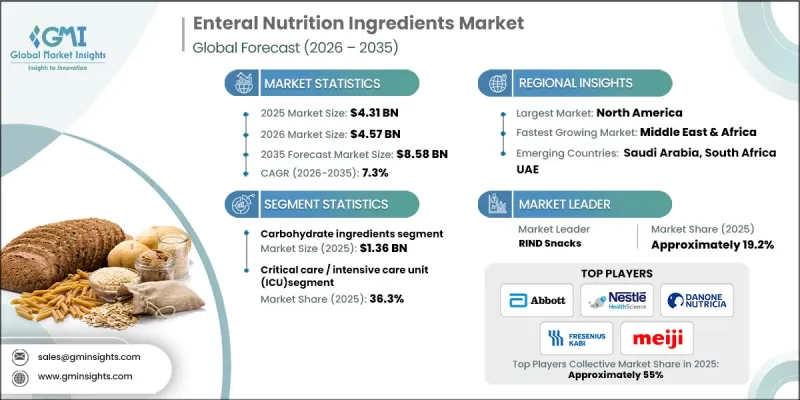

세계의 경장 영양제 원료 시장은 2025년에 43억 1,000만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 7.3%로 성장하여 85억 8,000만 달러에 이를 것으로 예측됩니다.

시장 확대는 만성질환 증가에 따른 장기 영양지원에 대한 수요 증가와 임상 영양 솔루션에 대한 수요 증가로 뒷받침되고 있습니다. 의료 서비스 제공업체는 비용 효율적이고 합병증 위험이 낮으며 환자의 회복 결과를 개선하기 위해 대체 영양법보다 장내 영양을 점점 더 많이 선택하고 있습니다. 이러한 지속적인 전환은 단백질, 탄수화물, 지질, 비타민, 미네랄 등 주요 영양 성분에 대한 수요를 직접적으로 견인하고 있습니다. 인구 통계학적 변화도 중요한 역할을 하고 있으며, 전 세계 노인 인구 증가에 따라 전문적인 영양관리가 요구되고 있습니다. 의료기관과 요양시설의 노인 케어 서비스 확대는 제조업체들이 소화하기 쉽고 영양학적으로 최적화된 원료를 개발하도록 유도하고 있습니다. 동시에 원료 가공 기술 및 제제 기술의 지속적인 혁신으로 제품의 효능, 내약성, 임상 적용성이 향상되어 시장 성장을 더욱 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 금액 | 43억 1,000만 달러 |

| 예측 금액 | 85억 8,000만 달러 |

| CAGR | 7.3% |

탄수화물 원료 부문은 2025년 13억 6,000만 달러를 차지할 것으로 예상되며, 2026-2035년 연평균 6.7% 성장할 것으로 전망됩니다. 전체 원료 유형의 성장은 더 높은 수준의 배합 요건과 진화하는 임상 영양 표준에 의해 형성되고 있습니다. 단백질은 근육의 유지와 회복을 돕기 위해 점점 더 많이 함유되고 있으며, 탄수화물 원료는 지속적인 에너지 공급과 대사 반응을 개선하기 위해 개선되고 있습니다. 지질이나 지방은 흡수성과 소화 내성을 향상시키기 위해 특수한 구조로 배합되는 경우가 증가하고 있습니다. 이처럼 원료의 기능성이 확대됨에 따라 표준 영양제부터 특정 병태에 초점을 맞춘 영양제까지 그 적용 범위가 넓어지고 있습니다.

중환자실/중환자실(ICU) 부문은 2025년 15억 6,000만 달러 시장 규모를 기록하며 36.3%의 점유율을 차지할 것으로 예측됩니다. 2035년까지 연평균 성장률(CAGR)은 6.6%로 예측됩니다. 임상 영양 관리의 변화로 급성기 의료 환경에서 경장영양이 조기에 도입되면서 대사 안정성과 장기 기능을 지원하는 원료에 대한 수요가 증가하고 있습니다. 또한, 영양 지원은 질병 관리 프로세스에 통합되고 있으며, 배합의 복잡성 및 원료 사용 증가로 이어지고 있습니다.

북미 경장 영양제 원료 시장은 2025년 17억 9,000만 달러 규모에 달할 것으로 예상되며, 예측 기간 동안 견조한 성장세를 유지할 것으로 예측됩니다. 이 지역은 선진적인 의료 인프라, 일관성 있는 상환 시스템, 병원 및 재택치료 현장에서 임상 영양을 광범위하게 도입하는 등의 이점을 가지고 있습니다. 미국은 고령화와 장기적인 건강 상태의 높은 발생률로 인해 임상 가이드라인에서 특수 단백질, 지질, 섬유질, 미량 영양소를 이용한 표적형 영양 중재의 중요성이 점점 더 강조되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 원료 유형별, 2022-2035년

제6장 시장 추산·예측 : 용도별, 2022-2035년

제7장 시장 추산·예측 : 지역별, 2022-2035년

제8장 기업 개요

LSH 26.03.26The Global Enteral Nutrition Ingredients Market was valued at USD 4.31 billion in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 8.58 billion by 2035.

Market expansion is supported by the rising demand for long-term nutritional support driven by the growing burden of chronic health conditions and the expanding need for clinical nutrition solutions. Healthcare providers are increasingly favoring enteral nutrition over alternative feeding approaches due to its cost efficiency, lower complication risks, and improved patient recovery outcomes. This sustained shift is directly driving demand for core nutritional ingredients, including proteins, carbohydrates, lipids, vitamins, and minerals. Demographic changes also play a critical role, as the global elderly population continues to grow and requires specialized nutritional management. Expanding geriatric care services across medical and assisted-care facilities is encouraging manufacturers to develop ingredients that are easier to digest and nutritionally optimized. In parallel, continuous innovation in ingredient processing and formulation technologies is enhancing product effectiveness, tolerance, and clinical applicability, further supporting market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.31 Billion |

| Forecast Value | $8.58 Billion |

| CAGR | 7.3% |

The carbohydrate ingredient segment accounted for USD 1.36 billion in 2025 and is projected to register a CAGR of 6.7% from 2026 to 2035. Growth across ingredient types is being shaped by more advanced formulation requirements and evolving clinical nutrition standards. Proteins are increasingly incorporated to support muscle preservation and recovery, while carbohydrate ingredients are being refined to deliver sustained energy and improved metabolic response. Lipids and fats are increasingly formulated into specialized structures to improve absorption and digestive tolerance. This broadening of ingredient functionality is expanding their application across both standard and condition-focused nutritional formulations.

The critical care and intensive care unit application segment generated USD 1.56 billion in 2025 and held a 36.3% share, with a CAGR of 6.6% through 2035. Shifts in clinical nutrition practices are driving earlier initiation of enteral feeding in acute care environments, increasing demand for ingredients that support metabolic stability and organ function. Nutritional support is also becoming increasingly integrated into disease management pathways, raising formulation complexity and ingredient utilization.

North America Enteral Nutrition Ingredients Market accounted for USD 1.79 billion in 2025 and is expected to maintain strong growth throughout the forecast period. The region benefits from advanced healthcare infrastructure, consistent reimbursement frameworks, and widespread adoption of clinical nutrition in hospital and home-care settings. The United States plays a central role due to its aging population and high incidence of long-term health conditions, with clinical guidelines increasingly emphasizing targeted nutrition interventions using specialized proteins, lipids, fibers, and micronutrients.

Key participants in the Global Enteral Nutrition Ingredients Market include Fresenius Kabi, Abbott, Meiji, Nutricia (Danone), Nestle Health Science, and other established suppliers. Companies operating in the enteral nutrition ingredients market are strengthening their competitive position through continuous product innovation and targeted ingredient development. Many players are investing in research to enhance the bioavailability, digestibility, and clinical efficacy of core ingredients. Strategic collaborations with healthcare providers and expansion of production capabilities are helping companies meet rising demand across hospital and home-care settings. Firms are also focusing on disease-specific formulations to align with evolving clinical protocols.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Ingredient Type

- 2.2.3 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Ingredient Type, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Protein Ingredients

- 5.2.1 Whole Proteins

- 5.2.2 Hydrolyzed Proteins/Peptides

- 5.2.3 Free Amino Acids

- 5.2.4 Functional Amino Acids

- 5.3 Carbohydrate Ingredients

- 5.3.1 Maltodextrins

- 5.3.2 Corn Syrup Solids / Glucose

- 5.3.3 Complex Carbohydrates

- 5.3.4 Simple Sugars

- 5.4 Fat / Lipid Ingredients

- 5.4.1 Long-Chain Triglycerides (LCTs)

- 5.4.2 Medium-Chain Triglycerides (MCTs)

- 5.4.3 Omega-3 Fatty Acids

- 5.4.4 Monounsaturated Fatty Acids (MUFA)

- 5.4.5 Structured Lipids & Blended Emulsions

- 5.5 Fiber Ingredients

- 5.5.1 Soluble Fibers

- 5.5.2 Insoluble Fibers

- 5.5.3 Resistant Starch

- 5.5.4 Prebiotic Fibers

- 5.6 Micronutrient Ingredients

- 5.6.1 Vitamins

- 5.6.2 Minerals

- 5.6.3 Electrolytes

- 5.6.4 Trace Elements

- 5.7 Functional & Immunonutrition Ingredients

- 5.7.1 Nucleotides

- 5.7.2 Probiotics

- 5.7.3 Antioxidants

- 5.7.4 Bioactive Peptides

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Critical care / intensive care unit (ICU)

- 6.3 Oncology / cancer

- 6.4 Gastrointestinal diseases

- 6.5 Neurological disorders

- 6.6 Metabolic disorders

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East & Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East & Africa

Chapter 8 Company Profiles

- 8.1 Abbott

- 8.2 Nutricia (Danone)

- 8.3 Nestle Health Science

- 8.4 Fresenius Kabi

- 8.5 Otsuka Pharmaceutical

- 8.6 RAUMEDIC AG

- 8.7 EA Pharma

- 8.8 Meiji

- 8.9 Arla Foods Ingredients