|

시장보고서

상품코드

1959575

카프릴로일글라이신 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Capryloyl Glycine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

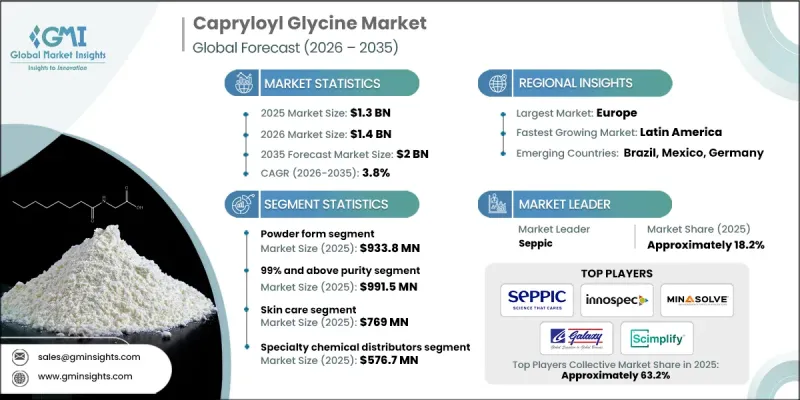

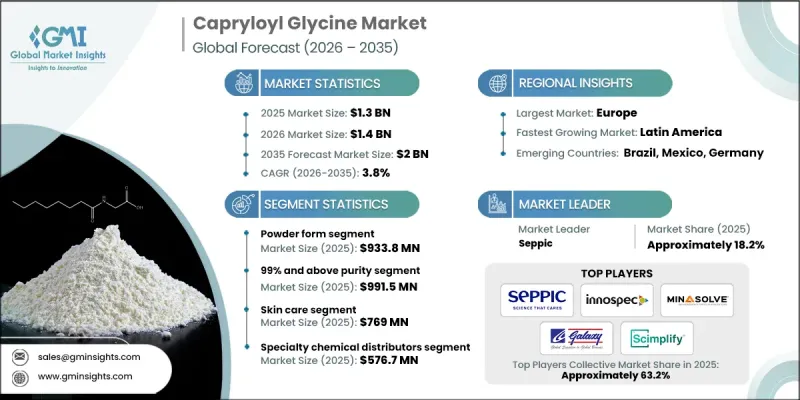

세계의 카프릴로일글라이신 시장은 2025년에 13억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 3.8%로 성장하여 20억 달러에 이를 것으로 예측됩니다.

이 시장은 클린 뷰티 포뮬러의 채택 확대와 퍼스널케어 제품에서 기존 합성 방부제에서 탈피하는 추세에 힘입어 꾸준히 성장하고 있습니다. 소비자들이 보다 순하고 피부 친화적이며 생분해성 성분을 찾는 경향이 강해짐에 따라, 제조업체들은 카프릴로일글라이신과 같은 다기능성 화합물을 사용하여 제품을 재제형화하고 있습니다. 이 아미노산 유도체는 항균성과 피부 컨디셔닝 효과를 제공하기 때문에 스킨케어, 헤어케어, 위생용품 분야에서 매우 수요가 많은 성분입니다. 여드름, 지루성 피부염, 피지 과다 분비 등 피부 및 두피 트러블이 증가함에 따라 마이크로바이옴 건강 유지, 피지 조절, 장벽 기능 보호를 돕는 처방에 대한 장기적인 수요가 증가하고 있습니다. 카프릴로일글라이신은 여드름 치료제, 두피 케어 솔루션, 민감성 피부용 제품에 점점 더 많이 사용되고 있으며, 대중 시장과 프리미엄 부문 모두에서 안정적인 소비를 유지하는 데 도움이 되고 있습니다. 화장품 개발자들은 효과, 안전성, 지속가능성을 추구하는 소비자의 취향에 따라 피부와 두피 마이크로바이옴의 건강을 지원하는 성분을 우선시하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 13억 달러 |

| 예측 금액 | 20억 달러 |

| CAGR | 3.8% |

분말 형태 부문은 2025년 9억 3,380만 달러에 달할 것으로 예측됩니다. 이 형태는 보존 기간이 길고, 보관이 용이하며, 대규모 건식 혼합 제제에서 정확한 투여가 가능하기 때문에 제조업체들이 널리 선호하고 있습니다. 분말 카프릴로일글라이신은 안정성과 정확한 배합이 중요한 맞춤형 퍼스널케어 제품에 특히 적합합니다. 한편, 액체 또는 수용액은 제형에 쉽게 통합할 수 있고, 가공을 빠르게 하고, 생산 효율을 높일 수 있기 때문에 인기가 높아지고 있습니다. 이 두 가지 형태를 사용할 수 있기 때문에 제조업체는 업무의 확장성과 제형 요구에 따라 최적의 형태를 선택할 수 있으며, 다양한 제품 카테고리에서 폭넓게 채택할 수 있습니다.

순도 99% 이상의 부문은 2025년 9억 9,150만 달러 시장 규모를 형성할 것으로 예측됩니다. 고순도 카프릴로일글라이신은 원료의 추적성과 배합의 정확성이 매우 중요한 고급 화장품, 화장품, 의료용 외용제에서 특히 선호되고 있습니다. 강화된 규제 기준, 국제 규정 준수 요건, 피부과 테스트를 거친 고품질 제품에 대한 소비자 선호도가 높아지면서 이 부문 수요가 가속화되고 있습니다. 각 제조업체들은 자사 제품의 차별화, 제품 성능 향상, 그리고 까다로운 품질 요건을 충족하는 프리미엄 및 용도별 특화 솔루션 공급자로서의 입지를 구축하기 위해 고도의 정제 기술에 대한 투자를 진행하고 있습니다.

북미 카프릴로일글라이신 시장은 2025년 3억 5,290만 달러 규모에 달할 것으로 예측됩니다. 이 지역은 정교한 퍼스널케어 산업, 높은 1인당 스킨케어 지출, 원료의 투명성과 지속가능성을 중시하는 클린 뷰티 운동의 확산에 힘입어 큰 성장 기회를 가지고 있습니다. 미국은 이 지역에서 가장 큰 기여를 하는 국가이며, 소비자의 기대에 부응하기 위해 제형업체들은 천연 유래의 다기능 성분을 점점 더 많이 찾고 있습니다. 제품 안전에 대한 인식 증가, 마이크로바이옴 친화적인 포뮬러, 친환경 성분에 대한 수요는 대중 시장과 프리미엄 퍼스널케어 카테고리 모두에서 카프릴로일글라이신의 채택을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 형태별, 2022-2035

제6장 시장 추산 및 예측 : 순도별, 2022-2035

제7장 시장 추산 및 예측 : 용도별, 2022-2035

제8장 시장 추산 및 예측 : 유통 채널별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.03.18The Global Capryloyl Glycine Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 3.8% to reach USD 2 billion by 2035.

The market has been steadily expanding, fueled by the growing adoption of clean beauty formulations and the shift away from conventional synthetic preservatives in personal care products. Consumers are increasingly demanding mild, skin-friendly, and biodegradable ingredients, prompting manufacturers to reformulate products with multifunctional compounds like capryloyl glycine. This amino acid derivative offers antimicrobial properties and skin-conditioning benefits, making it a highly sought-after ingredient across skincare, haircare, and hygiene products. Rising incidences of skin and scalp concerns such as acne, seborrheic dermatitis, and excess sebum production are driving long-term demand for formulations that support microbiome health, oil control, and barrier protection. Capryloyl glycine is increasingly incorporated into anti-acne treatments, scalp care solutions, and products for sensitive skin, helping maintain consistent consumption across both mass-market and premium segments. Cosmetic formulators are prioritizing ingredients that support skin and scalp microbiome health, aligning with consumer preferences for efficacy, safety, and sustainability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $2 Billion |

| CAGR | 3.8% |

The powder form segment reached USD 933.8 million in 2025. This form is widely favored by manufacturers due to its longer shelf life, ease of storage, and ability to be accurately dosed in large-scale and dry-blend formulations. Powder capryloyl glycine is particularly suitable for tailored personal care products where stability and precise incorporation are crucial. Meanwhile, liquid or aqueous solutions are gaining popularity because they integrate easily into formulations, accelerate processing, and enhance production efficiency. This dual availability allows manufacturers to select the most appropriate format based on operational scalability and formulation needs, supporting broader adoption across diverse product categories.

The segment with 99% and above purity generated USD 991.5 million in 2025. High-purity capryloyl glycine is particularly favored in premium cosmetics, cosmeceuticals, and medical topical applications, where ingredient traceability and formulation precision are critical. Rising regulatory standards, international compliance requirements, and consumer preference for dermatologically tested and high-quality products are accelerating demand in this segment. Manufacturers are investing in advanced purification technologies to differentiate their offerings, enhance product performance, and position themselves as suppliers of premium, application-specific solutions that meet stringent quality expectations.

North America Capryloyl Glycine Market accounted for USD 352.9 million in 2025. North America represents a major opportunity, driven by the region's sophisticated personal care industry, high per-capita skincare expenditure, and the growing clean-beauty movement emphasizing ingredient transparency and sustainability. The United States is the largest contributor in the region, with formulators increasingly seeking naturally derived, multifunctional ingredients to meet consumer expectations. Rising awareness of product safety, microbiome-friendly formulations, and the demand for environmentally responsible ingredients are fueling the adoption of capryloyl glycine in both mass-market and premium personal care categories.

Key companies operating in the Global Capryloyl Glycine Market include Sinerga S.p.A., Seppic, Euro-Kemical SRL, Innospec Inc., Zley Group, DropBio, AE Chemie, DRAVYOM Chemical Company, Pinpools GMBH, Special Chem, Minasolve, ATAMAN KIMYA, Galaxy Surfactants, and Uniproma. Companies in the Capryloyl Glycine Market are strengthening their position through multiple strategic initiatives. They are investing in R&D to develop high-purity and multifunctional derivatives to meet the demand for premium skincare and sensitive-skin applications. Manufacturers are optimizing production efficiency by offering both powder and liquid formats to suit different formulation requirements and large-scale industrial processing. Strategic partnerships with cosmetic and personal care brands are helping secure long-term supply agreements and enhance market penetration. Firms are also emphasizing sustainability, clean-label positioning, and compliance with global regulatory standards to attract environmentally conscious consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Form

- 2.2.3 Purity

- 2.2.4 Application

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for clean beauty & natural preservative alternatives

- 3.2.1.2 Growing prevalence of acne, seborrheic dermatitis & scalp disorders

- 3.2.1.3 Regulatory push against synthetic preservatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Potential skin irritation & allergic reactions in sensitive populations

- 3.2.2.2 Higher cost compared to conventional synthetic preservatives

- 3.2.3 Market opportunities

- 3.2.3.1 Untapped potential in oral care & dental hygiene products

- 3.2.3.2 Expansion into pharmaceutical-grade wound care & medical topicals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Form, 2022 - 2035 (USD million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Powder Form (>90% Concentration)

- 5.3 Liquid/Aqueous Solution

Chapter 6 Market Estimates and Forecast, By Purity, 2022 - 2035 (USD million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Between 95%-98% Purity

- 6.3 Between 98%-99% Purity

- 6.4 99% and Above Purity

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Skin care

- 7.2.1 Anti-acne products

- 7.2.2 Anti-wrinkle & anti-aging products

- 7.2.3 Sebum control & oily skin treatment

- 7.2.4 Ph balancing & skin barrier restoration

- 7.2.5 Dermo-protective products

- 7.3 Hair care & scalp treatment

- 7.3.1 Anti-dandruff products

- 7.3.2 Anti-seborrheic products

- 7.3.3 Scalp soothing & irritation relief

- 7.3.4 Hair conditioning products

- 7.4 Antiperspirant & deodorant

- 7.4.1 Deodorant formulations

- 7.4.2 Antiperspirant products

- 7.5 Wound care & medical topicals

- 7.5.1 Wound dressings & healing products

- 7.5.2 Dermatological treatments

- 7.6 Oral care

- 7.6.1 Toothpaste formulations

- 7.6.2 Mouthwash & oral rinse products

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Specialty chemical distributors

- 8.4 Online b2b platforms

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Seppic

- 10.2 Scimplify

- 10.3 ATAMAn KIMYA

- 10.4 Pinpools GMBH

- 10.5 Euro-Kemical SRL

- 10.6 Sinerga S.p.A.

- 10.7 AE Chemie

- 10.8 DRAVYOM Chemical Company

- 10.9 DropBio

- 10.10 Uniproma

- 10.11 pecial Chem

- 10.12 Zley Group

- 10.13 Innospec Inc.

- 10.14 Minasolve

- 10.15 Euro-Kemical

- 10.16 Galaxy Surfactants