|

시장보고서

상품코드

1959580

유리섬유 강화 플라스틱(GRP) 배관 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Glass Reinforced Plastic (GRP) Piping Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

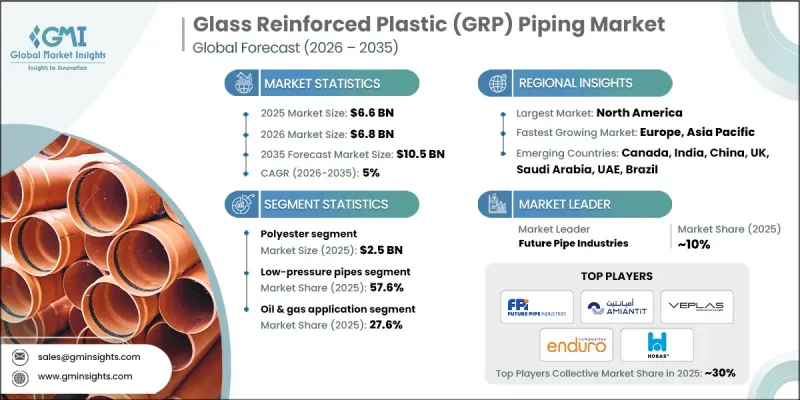

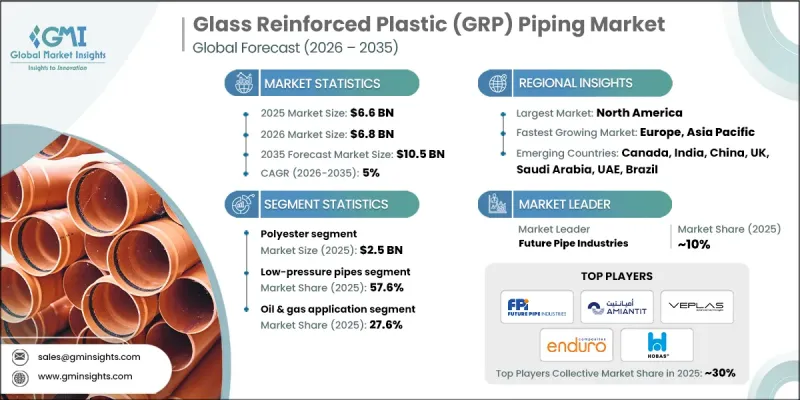

세계의 유리섬유 강화 플라스틱(GRP) 배관 시장은 2025년에 66억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5%로 성장하여 105억 달러에 이를 것으로 예측됩니다.

시장 성장은 높은 내식성, 내구성, 낮은 유지보수성을 요구하는 산업 분야에서 GRP 배관 채택이 확대되면서 시장 성장을 견인하고 있습니다. 석유 및 가스, 화학, 물 관리 등의 분야에서 GRP의 사용은 기존의 철강 및 콘크리트 시스템에 비해 긴 수명, 내화학성, 낮은 운영 비용으로 인해 증가하고 있습니다. GRP 배관은 가혹한 환경 조건에서도 높은 내구성을 발휘하고 수명주기 비용을 최소화하기 때문에 지속 가능하고 내구성이 뛰어난 인프라 솔루션을 원하는 산업계에 매력적인 선택이 되고 있습니다. 특히 개발도상국의 급속한 도시화와 지자체 인프라의 확장은 급수, 하수 관리, 관개 네트워크에서 GRP 배관에 대한 수요를 촉진하고 있습니다. 이 소재의 장기적인 성능 안정성과 지속가능성의 장점은 정부와 민간 기업이 장기적인 신뢰성을 위해 GRP 솔루션을 채택하는 것을 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 금액 | 66억 달러 |

| 예측 금액 | 105억 달러 |

| CAGR | 5% |

폴리에스테르 기반 GRP 배관 부문은 2025년 25억 달러 시장 규모를 차지할 것으로 예상되며, 2035년까지 연평균 5.2%의 성장률을 보일 것으로 예측됩니다. 이 배관은 우수한 내식성으로 높은 평가를 받고 있으며, 상수도, 하수, 관개, 산업용 화학물질 용도에 적합합니다. 폴리에스테르계 배관은 에폭시 수지나 비닐에스테르 수지의 대체품에 비해 비용 효율성이 뛰어나 신뢰성과 효율성을 중시하는 비용 중심 시장에서 대규모 지자체 프로젝트 및 인프라 프로젝트에서 채택을 촉진하고 있습니다.

석유 및 가스 부문은 2025년 27.6%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 4.8%로 성장할 것으로 전망됩니다. GRP 배관은 긴 수명, 내식성, 낮은 유지 보수성을 가지고 있으며, 플로우 라인, 물 주입 시스템, 생산 수처리, 정유소 가동에 적합합니다. 기업의 탐사 확대, 노후화된 인프라 교체, 운영 효율화를 추구함에 따라 다운타임과 라이프사이클 비용을 절감하는 GRP 솔루션에 대한 수요는 지속적으로 증가하고 있습니다.

북미 유리섬유강화플라스틱(GRP) 배관 시장은 2025년 12억 달러로 평가되었습니다. 미국의 광범위한 노후화된 배관 라인은 긴 수명, 내식성, 낮은 유지보수 비용을 제공하는 재료로 교체가 필요하며, GRP 배관이 선호되는 솔루션으로 자리매김하고 있습니다. 석유 및 가스, 화학 처리, 재생 에너지 분야의 투자 증가로 인해 가혹한 조건을 견디고 지속 가능한 운영을 지원하는 배관 기술에 대한 수요가 증가하고 있습니다. 환경 규제에 대한 적합성과 효율성에 대한 규제 당국의 집중적인 노력은 친환경 GRP 재료의 도입을 더욱 가속화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 제품 유형별, 2022-2035년

제6장 시장 추산·예측 : 제조 공정별, 2022-2035년

제7장 시장 추산·예측 : 압력 정격별, 2022-2035년

제8장 시장 추산·예측 : 용도별, 2022-2035년

제9장 시장 추산·예측 : 유통 채널별, 2022-2035년

제10장 시장 추산·예측 : 지역별, 2022-2035년

제11장 기업 개요

LSH 26.03.26The Global Glass Reinforced Plastic Piping Market was valued at USD 6.6 billion in 2025 and is estimated to grow at a CAGR of 5% to reach USD 10.5 billion by 2035.

Market growth is driven by the rising adoption of GRP piping across industries that demand highly corrosion-resistant, durable, and low-maintenance materials. Sectors such as oil and gas, chemicals, and water management are increasingly using GRP due to its longer service life, chemical resistance, and lower operational costs compared to traditional steel or concrete systems. GRP piping also offers resilience under extreme environmental conditions while minimizing lifecycle costs, making it an attractive choice for industries seeking sustainable and durable infrastructure solutions. Rapid urbanization and expanding municipal infrastructure, particularly in developing regions, are fueling demand for GRP pipes in water distribution, sewage management, and irrigation networks. The material's performance stability over time, combined with its sustainability benefits, is encouraging governments and private enterprises to adopt GRP solutions for long-term reliability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.6 Billion |

| Forecast Value | $10.5 Billion |

| CAGR | 5% |

The polyester-based GRP pipes segment accounted for USD 2.5 billion in 2025 and is expected to grow at a CAGR of 5.2% through 2035. These pipes are favored for their excellent corrosion resistance, making them ideal for water, sewage, irrigation, and industrial chemical applications. Polyester variants are cost-effective compared to epoxy and vinyl ester alternatives, driving their adoption in large-scale municipal and infrastructure projects, particularly in cost-sensitive markets seeking both reliability and efficiency.

The oil & gas segment held a 27.6% share in 2025 and is projected to grow at a CAGR of 4.8% during 2026-2035. GRP pipes provide long service life, corrosion resistance, and low maintenance requirements, making them suitable for flowlines, water injection systems, produced water handling, and refinery operations. As companies expand exploration, replace aging infrastructure, and seek operational efficiency, the demand for GRP solutions that reduce downtime and total lifecycle costs continues to rise.

North America Glass Reinforced Plastic (GRP) Piping Market was valued at USD 1.2 billion in 2025. Widespread aging pipelines in the U.S. require replacement with materials that provide longevity, corrosion resistance, and lower maintenance costs, positioning GRP pipes as a preferred solution. Increased investments across oil and gas, chemical processing, and renewable energy sectors are boosting demand for piping technologies that withstand harsh conditions while supporting sustainable operations. Regulatory focus on environmental compliance and efficiency further accelerates the adoption of eco-friendly GRP materials.

Key players in the Global Glass Reinforced Plastic Piping Market include Enduro Composites, Future Pipe Industries, Smithline Reinforced Composites, Veplas d.d., Industrial Plastic Systems, Plasticon Composites, Composite Pipes Industry, Dubai Pipes Factory, Graphite India Limited, Sarplast, HOBAS, Hanwei Energy Services Corp., Saudi Arabian Amiantit Company, and Fibrex. Companies in the Glass Reinforced Plastic Piping Market are pursuing multiple strategies to strengthen their foothold. They are investing in R&D to develop high-performance, corrosion-resistant, and lightweight pipes suitable for extreme conditions and specialized applications. Strategic partnerships with municipal authorities, industrial clients, and engineering firms allow for early adoption and integration of advanced piping systems. Expanding manufacturing capabilities and localizing production help reduce lead times and logistical costs while meeting regional demand. Firms are also emphasizing sustainable and eco-friendly materials to align with regulatory standards and environmental goals.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Manufacturing process

- 2.2.4 Application

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for corrosion-resistant & low-maintenance materials

- 3.2.1.2 Urbanization and growing water & wastewater needs

- 3.2.1.3 Infrastructure development & replacement of aging systems

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Impact of global trade uncertainties & tariff fluctuations

- 3.2.2.2 High initial capital costs & installation expenses

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Epoxy

- 5.3 Polyester

- 5.4 Vinyl ester

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Manufacturing Process, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Filament winding

- 6.3 Resin transfer molding (RTM)

- 6.4 Centrifugal casting

Chapter 7 Market Estimates & Forecast, By Pressure Rating, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low-pressure pipes

- 7.3 High-pressure pipes

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Oil & gas

- 8.3 Chemicals

- 8.4 Wastewater treatment

- 8.5 Irrigation

- 8.6 Water supply

- 8.7 Others (pulp & paper, power generation, mining, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Composite Pipes Industry

- 11.2 Dubai Pipes Factory

- 11.3 Enduro Composites

- 11.4 Fibrex

- 11.5 Future Pipe Industries

- 11.6 Graphite India Limited

- 11.7 Hanwei Energy Services Corp.

- 11.8 Harwal Group

- 11.9 HOBAS

- 11.10 Industrial Plastic Systems

- 11.11 Plasticon Composites

- 11.12 Sarplast

- 11.13 Saudi Arabian Amiantit Company

- 11.14 Smithline Reinforced Composites

- 11.15 Veplas d.d.