|

시장보고서

상품코드

1959601

동기 콘덴서 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Synchronous Condenser Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

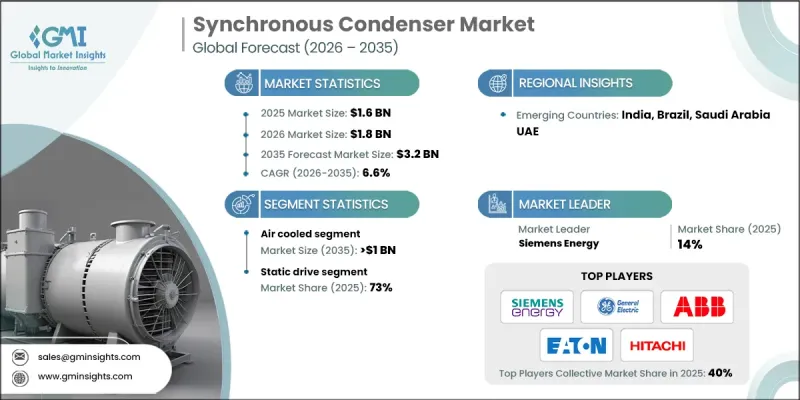

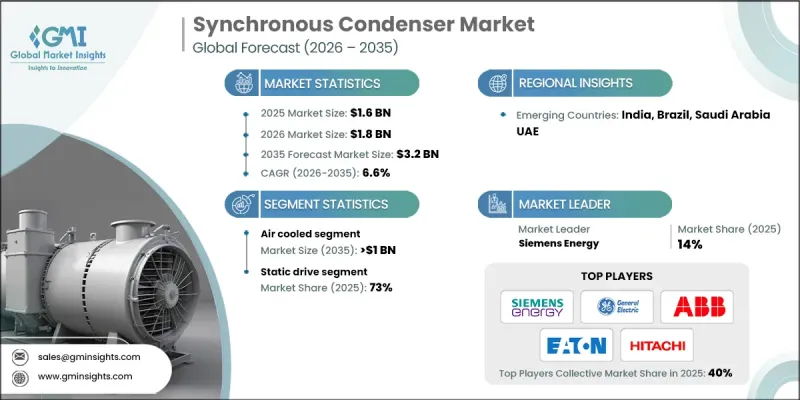

세계의 동기 콘덴서 시장은 2025년에 16억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 6.6%로 성장하여 32억 달러에 이를 것으로 예측됩니다.

이러한 성장은 기존 전력망의 관성 및 무효전력을 공급하던 화석연료 발전소의 폐지로 인해 동기 콘덴서가 효과적으로 대응할 수 있는 중요한 틈새가 생긴 것이 주요 요인으로 작용했습니다. 스마트 그리드 개발 및 고압직류송전(HVDC) 프로젝트를 포함한 그리드 현대화 이니셔티브는 이러한 장비에 대한 수요를 가속화하고 있습니다. 정부와 전력회사는 노후화된 인프라를 갱신하고, 보다 엄격한 신뢰성 기준을 달성하며, 분산형 에너지 자원을 통합하기 위해 많은 투자를 하고 있습니다. 풍력 및 태양광 발전의 급속한 도입은 전압과 주파수를 불안정하게 만드는 변동성 출력을 가져옵니다. 동기 콘덴서는 신속하고 안정적인 무효 전력 지원을 제공하여 전력 시스템을 안정화시키고 전력 품질을 향상시킵니다. 전력 수요 증가와 재생 에너지 프로젝트에 대한 대규모 투자가 결합되어 이러한 시스템의 도입을 더욱 촉진하고 있습니다. 현대의 전력 시스템에서는 간헐적인 에너지원을 효율적으로 관리할 수 있는 고도의 솔루션이 요구되고 있기 때문입니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측연도 | 2026-2035년 |

| 개시 연도 가치 | 16억 달러 |

| 예측 금액 | 32억 달러 |

| CAGR | 6.6% |

공랭식 부문은 2035년까지 10억 달러에 달할 것으로 예측됩니다. 공랭식 동기 콘덴서는 수냉식이나 수소 냉각식 시스템에 비해 비용 효율성이 뛰어나고 설치 과정이 간단하여 선호되고 있습니다. 이러한 설계는 인프라 요구 사항을 줄여 초기 자본 지출과 운영상의 복잡성을 줄여줍니다. 따라서 수자원이 한정된 지역이나 안전 규제가 엄격한 지역에서 특히 적합합니다. 기술 발전으로 효율성과 신뢰성이 더욱 향상되면서 전 세계 산업 및 유틸리티 분야에서 공랭식 냉각 시스템의 채택이 확대되고 있습니다.

2025년 기준 정전기 구동 부문은 73%의 점유율을 차지하며, 2026년부터 2035년까지 연평균 6%의 성장률을 보일 것으로 예측됩니다. 사이리스터, IGBT 등 전력 전자 부품을 활용한 정전식 구동은 기존 시동 방식에 비해 뛰어난 효율을 제공합니다. 시동 전류와 토크를 정밀하게 제어할 수 있어 기계적 스트레스를 최소화하고 장비의 마모를 줄여 대규모 전력망에서 보다 안정적인 작동을 보장합니다.

미국 동기 콘덴서 시장은 2035년까지 1억 8,800만 달러 규모에 달할 것으로 예측됩니다. 전력계통의 신뢰성 확보와 재생에너지 통합을 위한 엄격한 규제로 인해 동기 콘덴서와 같은 고도의 무효전력 보상장치의 필요성이 증가하고 있습니다. 석유 및 가스 산업 등 수요를 포함한 산업 성장도 도입을 더욱 촉진하고 있습니다. 미국은 세계 무역에서도 중요한 역할을 담당하고 있으며, 전력 인프라 투자는 국내외 에너지 시장 모두에 영향을 미칩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모와 예측 : 냉각 방식별, 2022-2035

제6장 시장 규모와 예측 : 시동방법별, 2022-2035

제7장 시장 규모와 예측 : 최종사용자별, 2022-2035

제8장 시장 규모와 예측 : 무효 정격전력별, 2022-2035

제9장 시장 규모와 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.03.16The Global Synchronous Condenser Market was valued at USD 1.6 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 3.2 billion by 2035.

The growth is driven by the retirement of fossil-fuel-based power plants, which traditionally supplied grid inertia and reactive power, leaving a critical gap that synchronous condensers effectively address. Grid modernization initiatives, including smart grid development and high-voltage direct current (HVDC) transmission projects, are accelerating the demand for these devices. Governments and utilities are investing heavily to upgrade aging infrastructure, meet stricter reliability standards, and integrate distributed energy resources. The rapid deployment of wind and solar power introduces variable outputs that can destabilize voltage and frequency. Synchronous condensers provide fast and reliable reactive power support, stabilizing the grid and enhancing power quality. Rising electricity demand, coupled with large-scale investments in renewable energy projects, is further driving the adoption of these systems, as modern grids require advanced solutions to manage intermittent energy sources efficiently.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 6.6% |

The air-cooled segment is expected to reach USD 1 billion by 2035. Air-cooled synchronous condensers are favored for their cost-effectiveness and simpler installation process compared to water- or hydrogen-cooled systems. Their design reduces infrastructure requirements, lowering upfront capital expenditure and operational complexity. This makes them particularly suitable for regions with limited water resources or strict safety regulations. Technological advancements have further improved efficiency and reliability, increasing the adoption of air-cooled systems across industrial and utility applications worldwide.

The static drive segment accounted for 73% share in 2025 and is projected to grow at a CAGR of 6% from 2026 to 2035. Static drives, which leverage power electronic components like thyristors and IGBTs, provide superior efficiency over traditional starting methods. They allow precise control of starting current and torque, minimizing mechanical stress, reducing equipment wear, and ensuring more reliable operation in large-scale electrical networks.

U.S. Synchronous Condenser Market is expected to reach USD 188 million by 2035. Stringent regulations focused on grid reliability and the integration of renewable energy necessitate advanced reactive power compensation devices like synchronous condensers. Industrial growth, including demand from sectors such as oil and gas, further drives adoption. The U.S. also plays a significant role in global trade, where electricity infrastructure investments impact both domestic and international energy markets.

Leading players in the Global Synchronous Condenser Market include ABB, Hitachi Energy Ltd., Toshiba Energy Systems & Solutions Corporation, Mitsubishi Electric Power Products, Inc., Alstom SA, Eaton, Siemens Energy, Doosan, NIDEC Corporation, Bharat Heavy Electricals Limited, Ansaldo Energia, Power Systems & Controls, Inc., BRUSH, Voith GmbH & Co., ANDRITZ, Shanghai Electric, Baker Hughes, and Ingeteam. Companies in the synchronous condenser market are adopting multiple strategies to strengthen their market position. Investment in research and development focuses on enhancing efficiency, reliability, and integration with renewable energy grids. Strategic partnerships with utilities and independent power producers help expand deployment and service networks globally. Firms are developing modular, scalable solutions tailored to industrial, renewable, and grid stabilization applications. Focusing on digital monitoring, predictive maintenance, and remote control capabilities improves operational performance and customer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability landscape

- 3.1.2 Factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Emerging opportunities & trends

- 3.8 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking depictions

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Cooling, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hydrogen Cooled

- 5.3 Air Cooled

- 5.4 Water Cooled

Chapter 6 Market Size and Forecast, By Starting Method, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Static Drive

- 6.3 Pony motors

- 6.4 Others

Chapter 7 Market Size and Forecast, By End User, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Utility

- 7.3 Industrial

Chapter 8 Market Size and Forecast, By Reactive Power Rating, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 ≤ 100 MVAr

- 8.3 > 100 MVAr to ≤ 200 MVAr

- 8.4 > 200 MVAr

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 Italy

- 9.3.3 France

- 9.3.4 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Alstom SA

- 10.3 ANDRITZ

- 10.4 Ansaldo Energia

- 10.5 Baker Hughes

- 10.6 Bharat Heavy Electricals Limited

- 10.7 BRUSH

- 10.8 Doosan

- 10.9 Eaton

- 10.10 General Electric

- 10.11 Hitachi Energy Ltd.

- 10.12 Ingeteam

- 10.13 Mitsubishi Electric Power Products, Inc.

- 10.14 NIDEC Corporation

- 10.15 Power Systems & Controls, Inc.

- 10.16 Shanghai Electric

- 10.17 Siemens Energy

- 10.18 Toshiba Energy Systems & Solutions Corporation

- 10.19 Voith GmbH & Co.

- 10.20 WEG