|

시장보고서

상품코드

1959612

항염증제 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Anti-inflammatory Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

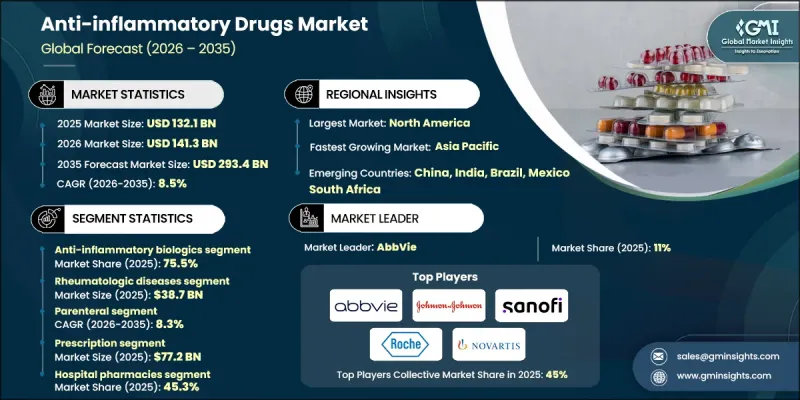

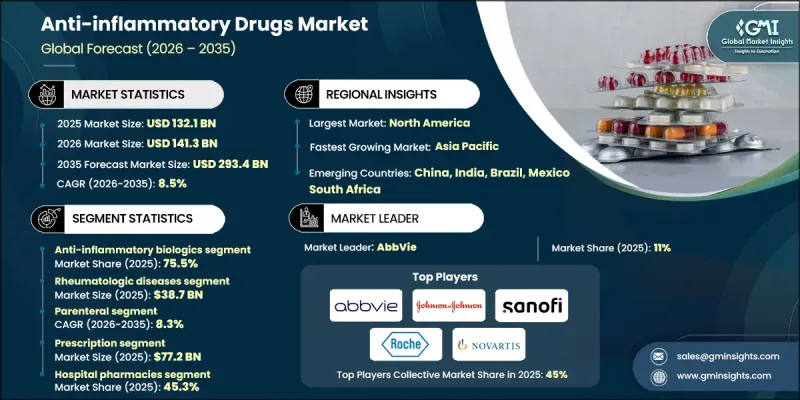

세계의 항염증제 시장은 2025년에 1,321억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 8.5%로 성장하여 2,934억 달러에 이를 것으로 예측되고 있습니다.

시장 성장은 면역학 연구와 분자과학의 지속적인 발전으로 뒷받침되고 있으며, 이를 통해 보다 정밀하고 효과적인 치료법을 개발할 수 있게 되었습니다. 치료 접근법은 기존의 비스테로이드성 항염증제(NSAIDs)와 코르티코스테로이드에서 표적 생물학적 제제, 단일클론항체, 첨단 저분자 억제제로 꾸준히 전환되고 있습니다. 이러한 혁신은 질병 관리 개선, 부작용 감소, 환자들에게 더 나은 장기적 치료 결과를 가져다주고 있습니다. 이 시장은 염증 관리, 증상 완화, 질병 진행 지연을 목표로 하는 다양한 치료 클래스를 통해 광범위한 급성 및 만성 염증성 질환에 대응하고 있습니다. 강력한 상환 제도와 면역에 초점을 맞춘 신약개발에 대한 지속적인 투자가 치료법의 보급을 촉진하고 있습니다. 경구제, 지속형 주사제, 저용량 생물학적 제제 등 첨단 전달 플랫폼의 등장으로 환자의 편의성과 복약 순응도가 향상되고 있습니다. 전반적으로 시장은 혁신적인 규제 환경과 확대되는 임상 파이프라인에 힘입어 정밀의료에 기반한 환자 중심 치료로 진화하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 1,321억 달러 |

| 예측 금액 | 2,934억 달러 |

| CAGR | 8.5% |

항염증 생물학적 제제 부문은 2025년 75.5%의 점유율을 차지하며 2026년부터 2035년까지 8.6%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 이러한 선도적 지위는 높은 임상적 효과, 염증 경로에 대한 선택적 표적화, 중등도에서 중증의 질병 상태를 관리할 수 있는 능력에 의해 뒷받침됩니다. 이러한 치료법은 증상 완화와 장기적인 질환 개선 효과를 모두 제공하기 때문에 고급 치료 환경에서 선호되는 선택이 되고 있습니다.

처방약 부문은 2025년 772억 달러의 매출을 기록할 것으로 예상되며, 여전히 지배적인 위치를 차지하고 있습니다. 의사의 감독과 전문적인 치료 프로토콜이 필요한 염증성 질환 및 자가면역질환의 장기적인 관리를 위해서는 여전히 처방약 기반 치료법이 필수적입니다. 생물학적 제제 및 표적 지향적 경구용 의약품의 광범위한 보급과 더불어 강력한 상환 제도와 병원 중심의 유통망은 이 부문을 지속적으로 지원하고 있습니다.

북미 항염증제 시장은 2025년 39.1%의 점유율을 차지하며 세계 수요를 견인했습니다. 높은 질병 유병률, 잘 정비된 의료 인프라, 혁신적인 치료법에 대한 조기 접근성, 유리한 상환 정책이 시장의 강점을 뒷받침하고 있습니다. 지속적인 임상 연구 활동과 강력한 제약 기업의 존재는 이 지역의 선도적 위치를 더욱 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 약제 클래스별, 2022-2035

제6장 시장 추산 및 예측 : 적응증별, 2022-2035

제7장 시장 추산 및 예측 : 투여 경로별, 2022-2035

제8장 시장 추산 및 예측 : 유형별, 2022-2035

제9장 시장 추산 및 예측 : 유통 채널별, 2022-2035

제10장 시장 추산 및 예측 : 지역별, 2022-2035

제11장 기업 개요

LSH 26.03.16The Global Anti-Inflammatory Drugs Market was valued at USD 132.1 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 293.4 billion by 2035.

Market growth is supported by continued progress in immunology research and molecular science, which is enabling the development of more precise and effective therapies. Treatment approaches are steadily shifting away from traditional nonsteroidal anti-inflammatory drugs and corticosteroids toward targeted biologics, monoclonal antibodies, and advanced small-molecule inhibitors. These innovations are improving disease control, reducing side effects, and delivering better long-term outcomes for patients. The market addresses a wide spectrum of acute and chronic inflammatory conditions through multiple therapeutic classes designed to manage inflammation, ease symptoms, and slow disease progression. Strong reimbursement structures and sustained investment in immune-focused drug discovery are reinforcing adoption. Emerging oral therapies and advanced delivery platforms, including extended-duration injectables and less frequent dosing biologics, are enhancing patient convenience and adherence. Overall, the market is evolving toward precision-based, patient-focused treatments supported by innovation-friendly regulatory environments and expanding clinical pipelines.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $132.1 Billion |

| Forecast Value | $293.4 Billion |

| CAGR | 8.5% |

The anti-inflammatory biologics segment accounted for 75.5% share in 2025 and is expected to grow at a CAGR of 8.6% during 2026-2035. Their leadership position is driven by high clinical effectiveness, selective targeting of inflammatory pathways, and their ability to manage moderate to severe disease states. These therapies deliver both symptom relief and long-term disease modification, making them a preferred option in advanced treatment settings.

The prescription segment generated USD 77.2 billion in 2025, maintaining its dominant position. Prescription-based therapies remain essential for long-term management of inflammatory and autoimmune conditions that require physician supervision and specialized treatment protocols. Broad uptake of biologics and targeted oral drugs, combined with strong reimbursement and hospital-centered distribution, continues to support this segment.

North America Anti-inflammatory Drugs Market held a share of 39.1% in 2025, leading global demand. Market strength is supported by high disease prevalence, well-developed healthcare infrastructure, early access to innovative therapies, and favorable reimbursement policies. Ongoing clinical research activity and a strong pharmaceutical presence further reinforce the region's leadership.

Key companies operating in the Global Anti-inflammatory Drugs Market include Pfizer, AbbVie, Johnson & Johnson, Novartis, Sanofi, AstraZeneca, Eli Lilly and Company, Bristol-Myers Squibb, Amgen, Hoffmann-La Roche, Merck & Co., GlaxoSmithKline, UCB, Abbott Laboratories, Teva Pharmaceutical, and Sun Pharmaceutical. Companies in the anti-inflammatory drugs market are strengthening their competitive position through sustained investment in research and development, particularly in targeted therapies and next-generation biologics. Many players are expanding their pipelines through strategic collaborations, licensing agreements, and acquisitions to access novel mechanisms of action. The focus on oral formulations and long-acting delivery systems is improving patient adherence and market reach. Firms are also prioritizing geographic expansion in high-growth regions while securing strong reimbursement positioning in mature markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug class trends

- 2.2.3 Treatment trends

- 2.2.4 Route of administration trends

- 2.2.5 Type trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic inflammatory and autoimmune diseases

- 3.2.1.2 Advancements in targeted immunology and biologic drug development

- 3.2.1.3 Supportive regulatory pathways and accelerated approvals

- 3.2.1.4 Rising awareness, diagnosis rates, and access to specialty care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs and long-term affordability concerns

- 3.2.2.2 Safety concerns and long-term tolerability risks

- 3.2.3 Market opportunities

- 3.2.3.1 Next-generation oral therapies and improved patient convenience

- 3.2.3.2 Lifecycle management through biosimilars and combination therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Future market trends

- 3.6 Pricing analysis

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Anti-inflammatory biologics

- 5.3 Nonsteroidal anti inflammatory drugs (NSAIDS)

- 5.4 Corticosteroids

- 5.5 Other drug classes

Chapter 6 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Rheumatologic diseases

- 6.2.1 Rheumatoid arthritis

- 6.2.2 Osteoarthritis

- 6.2.3 Psoriatic arthritis

- 6.2.4 Ankylosing spondylitis

- 6.2.5 Other inflammatory arthritis

- 6.3 Dermatological diseases

- 6.3.1 Psoriasis

- 6.3.2 Atopic dermatitis

- 6.3.3 Hidradenitis suppurativa

- 6.3.4 Other inflammatory skin diseases

- 6.4 Gastrointestinal diseases

- 6.4.1 Inflammatory bowel disease (IBD)

- 6.4.2 Eosinophilic esophagitis

- 6.4.3 Other inflammatory GI disorders

- 6.5 Respiratory diseases

- 6.5.1 Asthma

- 6.5.2 Chronic obstructive pulmonary disease (COPD)

- 6.5.3 Allergic rhinitis

- 6.5.4 Other inflammatory respiratory diseases

- 6.6 Neurological disorders

- 6.7 Other indications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Topical

- 7.4 Injectable

- 7.5 Other routes of administration

Chapter 8 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Prescription

- 8.3 Over the counter (OTC)

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacies

- 9.3 Retail pharmacies

- 9.4 Online pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AbbVie

- 11.2 Abbott Laboratories

- 11.3 AbbVie

- 11.4 Amgen

- 11.5 AstraZeneca

- 11.6 Bristol-Myers Squibb

- 11.7 Eli Lilly and Company

- 11.8 GlaxoSmithKline

- 11.9 Hoffmann-La Roche

- 11.10 Johnson & Johnson

- 11.11 Merck & Co.

- 11.12 Novartis

- 11.13 Pfizer

- 11.14 Sanofi

- 11.15 Sun Pharmaceutical Industries

- 11.16 Teva Pharmaceutical

- 11.17 UCB