|

시장보고서

상품코드

1959631

비닐 시클로헥산 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Vinyl Cyclohexane Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

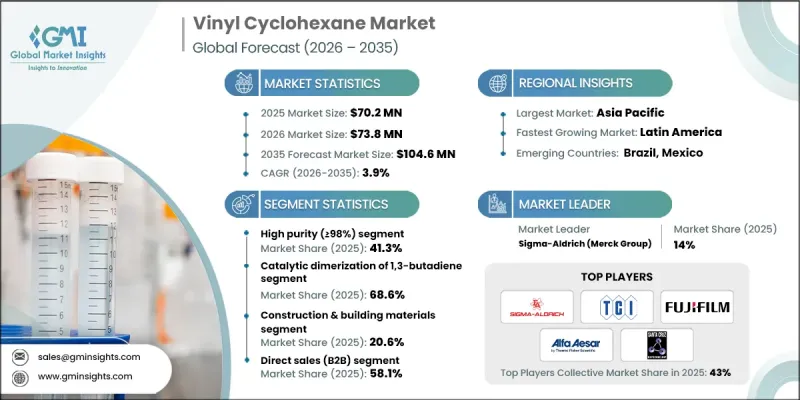

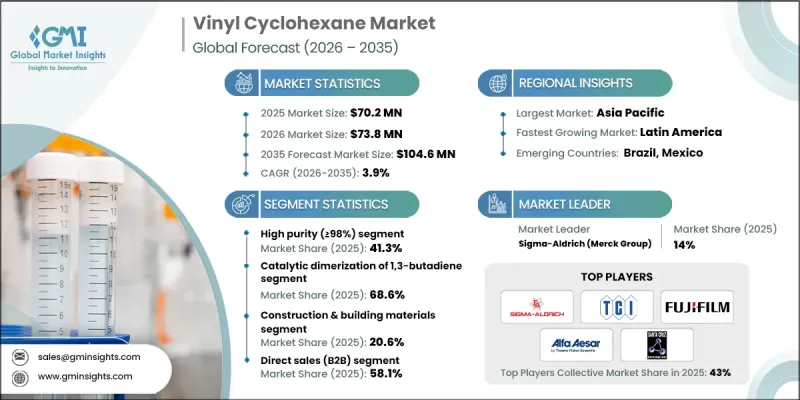

세계의 비닐 시클로헥산 시장은 2025년에 7,020만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 3.9%로 성장하여 1억 460만 달러에 이를 것으로 예측됩니다.

비닐시클로헥산에 대한 수요는 제조업체들이 첨단 소재 응용 분야에 대한 적용을 확대함에 따라 꾸준히 증가하고 있습니다. 이 화합물은 고성능 폴리머, 특수 코팅제, 접착제 및 기타 부가가치 화학 제제 생산에 중요한 중간체 역할을 합니다. 화학적 안정성과 다양한 제형과의 호환성으로 내구성, 구조적 무결성, 장기적인 성능이 요구되는 용도에 매우 적합합니다. 내열성, 내식성, 기계적 강도의 향상이 요구되는 산업 분야에서는 제품 개발 프로세스에 비닐사이클로헥산을 도입하는 것이 가속화되고 있습니다. 주요 최종 사용 분야는 자동차, 전자, 의료, 산업 제조 등 성능 중심의 소재가 우선시되는 분야입니다. 배합 효율 향상과 기능성 확대를 위한 지속적인 연구개발을 통해 더 많은 성장 기회가 열릴 것으로 예측됩니다. 지역별로 보면, 아시아태평양은 폴리머 제조거점이 잘 구축되어 있어 강력한 입지를 유지하고 있습니다. 한편, 북미와 유럽에서는 진화하는 규제 기준에 따라 혁신성, 지속가능성, 친환경 화학을 강조하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 7,020만 달러 |

| 예측 금액 | 1억 460만 달러 |

| CAGR | 3.9% |

고순도 비닐 시클로헥산 등급(순도 98% 이상)은 2025년 41.3%의 점유율을 차지하며 2035년까지 연평균 복합 성장률(CAGR) 5%를 나타낼 것으로 예측됩니다. 이 프리미엄 등급은 광학 투명성, 열 안정성, 내화학성이 필수적인 고급 용도에 널리 채택되고 있습니다. 고순도 배합 제품은 일관된 품질과 신뢰성이 매우 중요한 특수 폴리머, 정밀 코팅, 고성능 수지 분야에서 특히 높은 평가를 받고 있습니다.

직접 판매(B2B) 부문은 2025년 58.1%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 복합 성장률(CAGR) 2.8%로 성장할 것으로 전망됩니다. 대규모 산업 구매자와 제조업체는 안정적인 공급, 맞춤형 기술 지원, 장기 계약 체제를 보장하기 위해 직접 조달 채널을 선호합니다. 이 유통 모델은 자동차, 건설, 특수화학 산업에서 전략적 파트너십을 지원하고 있습니다. 화학제품 유통업체는 지역 기반의 재고 관리와 신속한 배송 솔루션을 필요로 하는 중간 규모 구매자를 위한 물류 유연성을 제공함으로써 지역 공급망에서 중요한 역할을 하고 있습니다.

북미 비닐 시클로헥산 시장은 2025년 21.7%의 점유율을 차지할 것으로 예상되며, 이는 꾸준한 지역적 성장을 반영합니다. 지속 가능한 소재와 저배출 화학 솔루션에 초점을 맞추고 있는 이 지역의 노력은 전 세계 탈탄소화 목표와 일치하며, 고순도 및 친환경 배합 기술에 대한 기회를 창출하고 있습니다. R&D에 대한 지속적인 투자와 통합된 공급망 역량으로 북미 특수화학 분야에서 입지를 강화하고, 비닐사이클로헥산에 대한 혁신 주도형 수요를 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 순도 레벨별, 2022-2035

제6장 시장 추산 및 예측 : 제조 공정별, 2022-2035

제7장 시장 추산 및 예측 : 용도별, 2022-2035

제8장 시장 추산 및 예측 : 유통 채널별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.03.16The Global Vinyl Cyclohexane Market was valued at USD 70.2 million in 2025 and is estimated to grow at a CAGR of 3.9% to reach USD 104.6 million by 2035.

Demand for vinyl cyclohexane has steadily increased as manufacturers expand its use across advanced material applications. The compound serves as a critical intermediate in the production of high-performance polymers, specialty coatings, adhesives, and other value-added chemical formulations. Its chemical stability and compatibility with diverse formulations make it highly suitable for applications that require durability, structural integrity, and long-term performance. Industries seeking enhanced thermal resistance, corrosion protection, and mechanical strength are increasingly incorporating vinyl cyclohexane into their product development processes. Key end-use sectors include automotive, electronics, healthcare, and industrial manufacturing, where performance-driven materials remain a priority. Ongoing research and development initiatives aimed at improving formulation efficiency and expanding functional properties are expected to unlock additional growth opportunities. Regionally, Asia-Pacific maintains a strong presence due to its established polymer manufacturing base, while North America and Europe emphasize innovation, sustainability, and environmentally responsible chemistry aligned with evolving regulatory standards.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $70.2 Million |

| Forecast Value | $104.6 Million |

| CAGR | 3.9% |

The high-purity vinyl cyclohexane grades (>=98%) accounted for 41.3% share in 2025 and are anticipated to grow at a CAGR of 5% through 2035. These premium grades are widely adopted in advanced applications where optical clarity, thermal stability, and chemical resistance are essential. High-purity formulations are particularly valued in specialty polymers, precision coatings, and high-performance resins, where consistent quality and reliability are critical.

The direct sales (B2B) segment held 58.1% share in 2025 and is projected to grow at a CAGR of 2.8% by 2035. Large-scale industrial buyers and manufacturers prefer direct procurement channels to ensure stable supply, customized technical support, and long-term contractual arrangements. This distribution model supports strategic partnerships across automotive, construction, and specialty chemical industries. Chemical distributors continue to play an important role in regional supply chains by managing localized inventories and offering logistical flexibility for mid-sized buyers requiring responsive delivery solutions.

North America Vinyl Cyclohexane Market accounted for 21.7% share in 2025, reflecting steady regional growth. The region's focus on sustainable materials and lower-emission chemical solutions aligns with global decarbonization objectives, creating opportunities for high-purity and environmentally conscious formulations. Continued investments in research and development, along with integrated supply chain capabilities, reinforce North America's position within the specialty chemicals sector and support innovation-driven demand for vinyl cyclohexane.

Key companies operating in the Global Vinyl Cyclohexane Market include Sigma-Aldrich (Merck Group), Tokyo Chemical Industry Co., Ltd., FUJIFILM Wako Pure Chemical Corporation, Alfa Aesar (Thermo Fisher Scientific), Santa Cruz Biotechnology, Inc., Hangzhou Keying Chem Co., Ltd, Dayang Chem (Hangzhou) Co., Ltd, Henan Tianfu Chemical Co., Ltd, Beantown Chemical Corporation, and Hebei Chuanghai Biotechnology Co., Ltd. Companies in the vinyl cyclohexane market are strengthening their competitive position through product quality enhancement, strategic distribution partnerships, and targeted research initiatives. Leading manufacturers are investing in advanced purification technologies to meet rising demand for high-purity grades used in performance-sensitive applications. Many firms are expanding global distribution networks to improve supply reliability and regional accessibility. Collaboration with downstream polymer and specialty chemical producers enables customized formulation development. Sustainability-focused investments, including cleaner production processes and environmentally compliant materials, are also gaining prominence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Purity level

- 2.2.3 Manufacturing process

- 2.2.4 End-use

- 2.2.5 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for specialty chemicals in various industries

- 3.2.1.2 Rising applications in polymer and resin manufacturing

- 3.2.1.3 Advancements in production technologies improving efficiency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Stringent environmental regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Growing adoption in emerging markets

- 3.2.3.2 Development of eco-friendly and sustainable production methods

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Purity level

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Purity Level, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 High purity (≥98%)

- 5.3 Medium purity (97%)

- 5.4 Standard purity (95%)

- 5.5 Commercial grade (>97% with inhibitor)

- 5.6 Research grade (≥99%)

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Manufacturing Process, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Catalytic dimerization of 1,3-butadiene

- 6.3 Thermal/non-catalytic dimerization

- 6.4 Co-production from butadiene refining

- 6.5 Photochemical dimerization

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End-Use, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive industry

- 7.3 Electronics & semiconductors

- 7.3.1 semiconductor packaging adhesives

- 7.3.2 LED encapsulants & opto-electronic devices

- 7.4 Construction & building materials

- 7.4.1 PVC plastisol applications

- 7.4.2 VOC compliance & green building standards

- 7.5 Pharmaceuticals

- 7.5.1 Active pharmaceutical ingredient (API) synthesis

- 7.6 Agrochemicals

- 7.7 Aerospace

- 7.8 Textiles & carpets

- 7.8.1 Styrene-butadiene latex adhesives

- 7.9 Medical devices

- 7.10 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Direct sales (B2B)

- 8.3 Chemical distributors

- 8.4 Online chemical marketplaces

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Sigma-Aldrich (Merck Group)

- 10.2 Tokyo Chemical Industry Co., Ltd.

- 10.3 FUJIFILM Wako Pure Chemical Corporation

- 10.4 Alfa Aesar (Thermo Fisher Scientific)

- 10.5 Santa Cruz Biotechnology, Inc.

- 10.6 Hangzhou Keying Chem Co., Ltd

- 10.7 Dayang Chem (Hangzhou) Co., Ltd

- 10.8 Henan Tianfu Chemical Co., Ltd

- 10.9 Beantown Chemical Corporation

- 10.10 Hebei Chuanghai Biotechnology Co., Ltd