|

시장보고서

상품코드

1959637

공인 자동차 서비스 센터 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Authorized Car Service Center Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

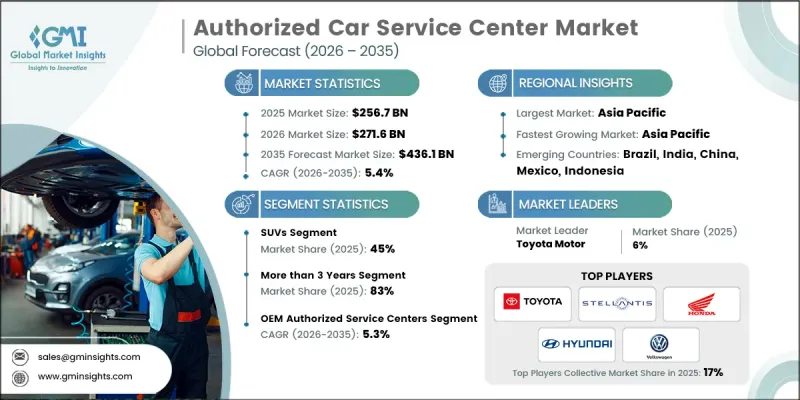

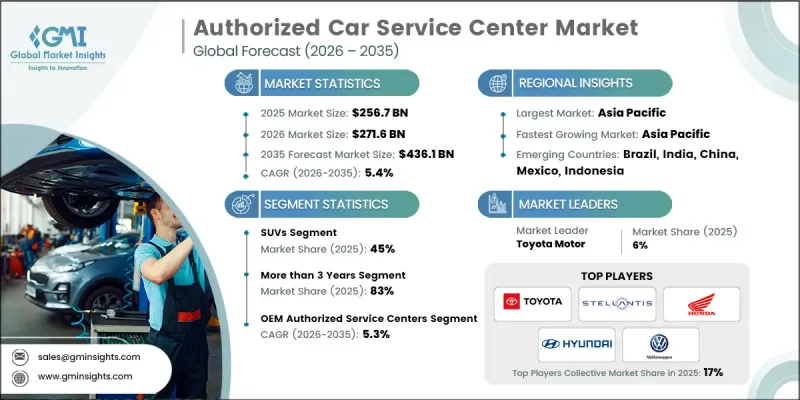

세계의 공인 자동차 서비스 센터 시장은 2025년에 2,567억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.4%로 성장하여 4,361억 달러에 이를 것으로 예측되고 있습니다.

공식 서비스 센터는 OEM 인증 유지보수, 수리, 업그레이드를 제공함으로써 차량의 안전, 성능, 내구성을 유지하는 데 중요한 역할을 담당하고 있습니다. 이 시장에는 딜러 서비스 센터, 여러 브랜드를 지원하는 공식 워크샵, 전문 유지 보수 체인이 포함되며, 모두 보증 수리, 진단 솔루션, 정품 예비 부품을 제공합니다. 차량 보유 대수가 증가하고 소유 주기가 길어짐에 따라 차량의 복잡성이 증가하여 전문 서비스 네트워크에 대한 수요가 증가하고 있습니다. OEM 제조업체는 고객 만족도 향상, 재판매 가치 유지, 보증 준수 보장을 위해 공인 서비스 센터에 대한 투자를 강화하고 있습니다. 커넥티드카 기술과 텔레매틱스의 통합은 예지보전을 가속화하고, 보다 빈번하고 예방적인 서비스 방문을 촉진하고 있습니다. 디지털화는 산업을 재구성하고 있으며, 서비스 센터는 통합 기술 플랫폼을 도입하여 고객 응대, 진단, 부품 조달, 서비스 관리의 효율화를 통해 업계 전반의 업무 흐름과 투자 전략을 근본적으로 변화시키고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 2,567억 달러 |

| 예측 금액 | 4,361억 달러 |

| CAGR | 5.4% |

SUV 부문은 2025년 45%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 5.7%의 성장률을 보일 것으로 전망됩니다. SUV는 다재다능함, 프리미엄 포지셔닝, 그리고 서비스별 수익을 높이는 복잡한 시스템으로 인해 선호되고 있습니다. 이러한 차량의 유지 보수에는 사륜구동 시스템, 대형 브레이크, 복잡한 서스펜션 진단, 더 빈번한 타이어 교체 등에 대한 전문적인 주의가 필요합니다.

OEM 인증 서비스 센터 부문은 2025년 57%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 5.3%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 이들 센터는 제조업체의 독점적인 승인을 받아 운영되며, 전용 진단 도구, 보증금 환불, OEM 교육을 제공합니다. 브랜드 신뢰도, 정품 부품에 대한 접근성, 제조업체 가이드라인을 엄격하게 준수함으로써 독립 서비스 제공업체에 비해 뚜렷한 경쟁 우위를 점하고 있습니다.

중국의 정식 자동차 서비스센터 시장은 2025년 414억 달러에 달할 것으로 예상되며, 2035년까지 연평균 5.9%의 성장률을 보일 것으로 전망됩니다. 이러한 성장은 지방 도시에서의 자동차 보유량 증가, 차량 1대당 서비스 지출 증가, 고급 차량에 대한 높은 수준의 유지보수 수요 증가에 의해 주도되고 있습니다. 온라인 예약, 모바일 결제, 커넥티드카 진단 등 디지털 서비스 도입이 보편화되고 있습니다. 중국의 주요 OEM 업체들은 정규 서비스 센터, 이동식 서비스 유닛, 배터리 교체 스테이션을 통해 서비스 제공의 혁신을 추진하여 편의성과 효율성을 높이고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 차종별, 2022-2035

제6장 시장 추산 및 예측 : 차량 연식별, 2022-2035

제7장 시장 추산 및 예측 : 추진력별, 2022-2035

제8장 시장 추산 및 예측 : 서비스별, 2022-2035

제9장 시장 추산 및 예측 : 서비스 제공업체별, 2022-2035

제10장 시장 추산 및 예측 : 최종 용도별, 2022-2035

제11장 시장 추산 및 예측 : 지역별, 2022-2035

제12장 기업 개요

LSH 26.03.16The Global Authorized Car Service Center Market was valued at USD 256.7 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 436.1 billion by 2035.

Authorized service centers play a vital role in maintaining vehicle safety, performance, and longevity by offering OEM-certified maintenance, repairs, and upgrades. The market encompasses dealership service centers, multi-brand authorized workshops, and specialized maintenance chains, all providing warranty-backed repairs, diagnostic solutions, and genuine spare parts. As vehicle fleets grow and ownership cycles lengthen, vehicle complexity rises, driving demand for professional service networks. OEMs are increasingly focusing on authorized service centers to improve customer satisfaction, preserve resale value, and ensure warranty compliance. The integration of connected vehicle technologies and telematics has accelerated predictive maintenance, encouraging more frequent and proactive service visits. Digitalization is reshaping the sector, with service centers adopting integrated technology platforms to streamline customer interactions, diagnostics, parts sourcing, and service management, fundamentally transforming operational workflows and investment strategies across the industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $256.7 Billion |

| Forecast Value | $436.1 Billion |

| CAGR | 5.4% |

The SUV segment held a 45% share in 2025 and is expected to grow at a CAGR of 5.7% through 2035. SUVs are favored due to their versatility, premium positioning, and complex systems, which increase per-service revenue. Maintenance for these vehicles involves specialized attention to all-wheel-drive systems, larger brakes, complex suspension diagnostics, and more frequent tire replacements.

The OEM-authorized service centers segment held 57% share in 2025, with a 5.3% CAGR forecast through 2035. These centers operate under exclusive manufacturer authorization, offering proprietary diagnostics, warranty reimbursement, and OEM training. Their brand trust, access to genuine parts, and adherence to manufacturer guidelines give them a clear competitive advantage over independent service providers.

China Authorized Car Service Center Market reached USD 41.4 billion in 2025 and will grow at a CAGR of 5.9% through 2035. Growth is fueled by rising vehicle ownership in lower-tier cities, increasing service expenditure per vehicle, and higher demand for advanced maintenance in premium vehicles. Digital service adoption, including online booking, mobile payment, and connected vehicle diagnostics, is becoming standard. Leading Chinese OEMs are innovating service delivery through authorized centers, mobile units, and battery swap stations, enhancing convenience and efficiency.

Key players in the Global Authorized Car Service Center Market include Toyota Motor, Mercedes-Benz, Ford Motor, Honda Motor, Volkswagen, BMW, Stellantis, Hyundai Motor, Robert Bosch, and General Motors. Companies in the Authorized Car Service Center Market are strengthening their presence through multiple strategies, including expanding geographically into emerging markets, integrating digital platforms for booking, payment, and service tracking, and investing in mobile service solutions. They are forming partnerships with local operators to increase reach, leveraging data analytics to offer predictive maintenance, and improving customer experience with faster turnaround times. OEMs focus on enhancing brand loyalty by providing training, proprietary tools, and genuine parts to maintain service quality, while adopting flexible pricing and subscription-based maintenance plans to attract a broader customer base. Continuous innovation in diagnostics, connected vehicle services, and energy-efficient repairs further reinforces their competitive foothold.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicles

- 2.2.3 Vehicles Age

- 2.2.4 Propulsion

- 2.2.5 Service

- 2.2.6 Service Providers

- 2.2.7 End Use

- 2.3 TAM Analysis, 2026-2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Aging vehicle fleet and extended ownership cycles

- 3.2.1.2 Rising vehicle complexity and technology integration

- 3.2.1.3 Increasing vehicle miles traveled (VMT)

- 3.2.1.4 Stringent emission and safety standards

- 3.2.1.5 Growing consumer preference for authorized services

- 3.2.1.6 Expansion of vehicle warranty programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure and equipment costs

- 3.2.2.2 Skilled technician shortage and training costs

- 3.2.2.3 Economic uncertainties and inflation impact

- 3.2.2.4 Supply chain disruptions and parts availability

- 3.2.3 Market opportunities

- 3.2.3.1 Electric vehicle service market emergence

- 3.2.3.2 Digital transformation and online service booking

- 3.2.3.3 Subscription-based maintenance programs

- 3.2.3.4 Expansion in emerging markets

- 3.2.3.5 Fleet management services

- 3.2.3.6 Used vehicle servicing growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Federal vehicle safety, emissions, and post-repair service regulations

- 3.4.1.2 Canada - Certified maintenance and EV servicing framework

- 3.4.2 Europe

- 3.4.2.1 Germany- EU vehicle safety regulations & national service standards

- 3.4.2.2 UK- Post-Brexit service compliance & connected vehicle guidance

- 3.4.2.3 France- National vehicle inspection & EV servicing policy

- 3.4.2.4 Italy- ITS pilots & smart-service regulations

- 3.4.3 Asia Pacific

- 3.4.3.1 China- MIIT vehicle servicing mandates & standards

- 3.4.3.2 India- Emerging automotive service & connectivity regulations

- 3.4.3.3 Japan- ITS connect & certified service policies

- 3.4.3.4 Australia- Technology neutral ITS policies

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM vehicle safety standards

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Digital service booking platforms

- 3.7.1.2 AI-powered diagnostic systems

- 3.7.2 Emerging technologies

- 3.7.2.1 Predictive maintenance technologies

- 3.7.2.2 EV service technologies & infrastructure

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.9 Pricing analysis

- 3.9.1 Service pricing models

- 3.9.2 Labor cost trends

- 3.9.3 Parts markup analysis

- 3.9.4 Competitive pricing strategies

- 3.10 Use cases & success stories

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Vehicle fleet demographics & age analysis

- 3.12.1 Global vehicle parc statistics

- 3.12.2 Average vehicle age trends

- 3.12.3 Impact on service demand

- 3.13 Unit Economics & Service Center Profitability Benchmarking

- 3.14 EV Impact on Authorized Service Business Models

- 3.15 Digital Customer Journey & Experience Benchmarking

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicles, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Hatchbacks

- 5.3 SUVs

- 5.4 Sedan

Chapter 6 Market Estimates & Forecast, By Vehicles Age, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Less than 3 years

- 6.3 More than 3 years

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 ICE

- 7.3 HEV/PHEV

- 7.4 EVs

Chapter 8 Market Estimates & Forecast, By Service, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Engine

- 8.3 Transmission

- 8.4 Brakes

- 8.5 Suspension

- 8.6 Electrical

- 8.7 Body

- 8.8 Tire

- 8.9 Belts & accessories

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Service Providers, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 OEM authorized service centers

- 9.3 Multi-brand service centers

- 9.4 Independent garages

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 Individual customers

- 10.3 Fleet operators

- 10.4 Corporate customers

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.3.9 Denmark

- 11.3.10 Poland

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Israel

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 3M

- 12.1.2 BMW

- 12.1.3 Castrol

- 12.1.4 Ford Motor

- 12.1.5 General Motors

- 12.1.6 Groupe Renault

- 12.1.7 Honda Motor

- 12.1.8 Hyundai Motor

- 12.1.9 Mercedes-Benz

- 12.1.10 Mobivia

- 12.1.11 Robert Bosch

- 12.1.12 Stellantis

- 12.1.13 Suzuki Motor

- 12.1.14 Toyota Motor

- 12.1.15 Volkswagen

- 12.2 Regional Players

- 12.2.1 Automovill Technologies

- 12.2.2 Carxpert Garage

- 12.2.3 Lansdowne Automobile

- 12.2.4 Mahindra First Choice

- 12.2.5 Meineke Car Care Centers

- 12.2.6 Mobil1 Car Care

- 12.2.7 TVS Automobile Solutions

- 12.3 Emerging Players & Technology Enablers

- 12.3.1 GoMechanic

- 12.3.2 Wrench

- 12.3.3 YourMechanic