|

시장보고서

상품코드

1959645

첨단 바이오연료 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Advanced Biofuel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

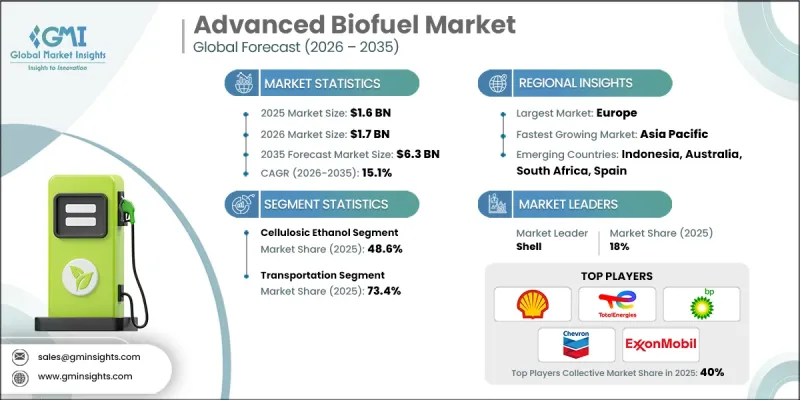

세계의 첨단 바이오연료 시장은 2025년에 16억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 15.1%로 성장하여 63억 달러에 이를 것으로 예측됩니다.

이러한 성장은 수입 원유 의존도를 낮추고 국가 에너지 안보를 강화하려는 각국 정부의 이니셔티브에 힘입은 바 큽니다. 각국은 공급망 취약성 완화, 가격 변동 리스크 헤지, 에너지 자립도 강화를 위해 국내 생산 재생가능 연료를 우선적으로 도입하고 있습니다. 선진 바이오연료는 기존 연료 인프라와 호환되는 확장 가능한 재생 가능한 대체 연료를 제공하기 때문에 강력한 에너지 시스템을 추구하는 선진국과 신흥국 모두에게 매우 중요합니다. 지속 가능한 연료 생산을 지원하는 정책적 인센티브, 재정적 보조금, 규제적 의무가 시장을 촉진하고 있습니다. 농업 잔재, 조류, 폐유, 리그노셀룰로오스 등 비식량 바이오매스 원료의 활용도가 높아짐에 따라 바이오연료 가치사슬 전반의 지속가능성이 향상되고 식량 생산과의 경쟁은 최소화되고 있습니다. 기술 발전, 지원 정책, 민관 협력의 조합이 전 세계적으로 보급을 가속화하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 16억 달러 |

| 예측 금액 | 63억 달러 |

| CAGR | 15.1% |

첨단 바이오연료는 농업 잔재, 임업 폐기물, 조류, 폐유 등 비식량 바이오매스로부터 생산됩니다. 이들 연료는 우수한 온실가스 감축 효과, 에너지 효율 향상, 기존 수송, 발전 및 산업용 연료 인프라와의 높은 호환성을 제공합니다. 정부의 이니셔티브와 재정적 인센티브를 통해 도입이 가속화되고, 상업화 리스크가 감소하며, 신기술 프로젝트의 자금 조달 가능성이 높아졌습니다. 원료 공급원의 확대는 순환경제의 원칙을 지지하고 화석연료 의존도를 낮추며 국가 에너지 안보를 강화합니다. 업계는 또한 보다 효율적인 바이오매스 전처리, 효소 가수분해, 발효 기술 등 공정 개선의 혜택을 누리고 있으며, 이는 비용 절감과 생산 규모 확대를 촉진하고 있습니다.

셀룰로오스계 에탄올 분야는 2025년 48.6%의 점유율을 차지하며 2035년까지 연평균 복합 성장률(CAGR) 14.8%로 확대될 것으로 예측됩니다. 전처리 공정, 효소 가수분해, 발효 기술의 발전으로 전환 효율, 효소 성능, 원료 이용률이 향상되고 경제성이 개선되었습니다. 비식량계 바이오연료에 대한 규제적 지원도 보급에 힘을 보태고 있습니다. 셀룰로오스계 에탄올은 혼합 의무를 충족하고, 식량 작물과의 경쟁을 줄이며, 전체 수명 주기에서 온실가스 감축 효과가 높기 때문입니다. 기존 연료 인프라와의 호환성으로 인해 수송용 연료의 탈탄소화에서 중요한 솔루션으로 자리매김하고 있습니다.

운송 용도 부문은 2025년 73.4%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 14.7%의 성장률을 보일 것으로 전망됩니다. 넷제로 목표 달성을 위한 국가 및 기업의 노력이 강화되면서 첨단 바이오연료의 도입이 촉진되고 있습니다. 이들 연료는 기존 연료에 비해 CO2를 크게 줄일 수 있으며, 전기화가 제한적인 분야에서 실용적인 탈탄소화 경로로 작용할 수 있습니다. 첨단 바이오연료는 장기적인 지속가능성 및 배출 감소 전략에 점점 더 많이 통합되어 차량 운영자, 대중 교통 및 물류 사업자가 규제 및 환경 목표를 달성할 수 있도록 돕고 있습니다.

미국의 첨단 바이오연료 시장은 2025년 93.4%의 점유율을 차지하며 2035년까지 20억 달러 규모로 성장할 것으로 예측됩니다. 풍부한 농업 원료, 기후 변화에 대한 관심 증가, 강력한 국내 생명공학 혁신이 도입을 촉진하고 있습니다. 미국의 주요 기업들은 정책적 지원, 연구 장려책, 첨단 생산 기술을 활용하여 사업 규모를 확장하고 배출량을 크게 줄이기 위해 셀룰로오스 및 조류 기반 연료에 집중하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모와 예측 : 연료 유형별, 2022-2035

제6장 시장 규모와 예측 : 원료별, 2022-2035

제7장 시장 규모와 예측 : 용도별, 2022-2035

제8장 시장 규모와 예측 : 지역별, 2022-2035

제9장 기업 개요

LSH 26.03.16The Global Advanced Biofuel Market was valued at USD 1.6 billion in 2025 and is estimated to grow at a CAGR of 15.1% to reach USD 6.3 billion by 2035.

Growth is driven by governments' focus on reducing reliance on imported crude oil and strengthening national energy security. Countries are prioritizing domestically produced renewable fuels to reduce supply chain vulnerabilities, hedge against price volatility, and enhance energy independence. Advanced biofuels offer scalable, renewable alternatives compatible with existing fuel infrastructure, making them critical for both developed and emerging economies seeking resilient energy systems. The market is benefiting from policy incentives, financial grants, and regulatory mandates that support sustainable fuel production. Increasing availability of non-food biomass feedstocks such as agricultural residues, algae, waste oils, and lignocellulosic materials is improving sustainability across the biofuel value chain while minimizing competition with food production. The combination of technological progress, supportive policies, and public-private collaborations is accelerating adoption globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Billion |

| Forecast Value | $6.3 Billion |

| CAGR | 15.1% |

Advanced biofuels are derived from non-food biomass, including agricultural residues, forestry waste, algae, and waste oils. These fuels offer superior greenhouse gas reductions, improved energy efficiency, and high compatibility with existing transport, power generation, and industrial fuel infrastructure. Government initiatives and fiscal incentives are accelerating adoption, mitigating commercialization risks, and enhancing project bankability for emerging technologies. Expanding feedstock availability supports circular economy principles, reduces reliance on fossil fuels, and strengthens national energy security. The industry is also benefiting from process improvements, such as more efficient biomass pretreatment, enzymatic hydrolysis, and fermentation techniques, which are driving cost reductions and increasing production scalability.

The cellulosic ethanol segment held 48.6% share in 2025 and is expected to grow at a CAGR of 14.8% through 2035. Technological advancements in pretreatment processes, enzymatic hydrolysis, and fermentation are improving economic feasibility by enhancing conversion efficiencies, enzyme performance, and feedstock utilization. Regulatory support for non-food-based biofuels is further boosting adoption, as cellulosic ethanol meets blending mandates, reduces competition with food crops, and achieves deeper lifecycle greenhouse gas reductions. Its compatibility with existing fuel infrastructure positions it as a key solution for decarbonizing transport fuels.

The transportation applications segment accounted for 73.4% share in 2025 and is projected to grow at a CAGR of 14.7% through 2035. Rising national and corporate commitments to achieve net-zero targets are driving advanced biofuel adoption. These fuels deliver significant CO2 reductions over conventional fuels and serve as a practical decarbonization pathway in sectors where electrification remains limited. Advanced biofuels are increasingly integrated into long-term sustainability and emission reduction strategies, supporting fleet operators, public transport authorities, and logistics providers in meeting regulatory and environmental targets.

U.S Advanced Biofuel Market held a 93.4% share in 2025 and is projected to generate USD 2 billion by 2035. Abundant agricultural feedstocks, growing climate change concerns, and strong domestic biotechnology innovation are driving adoption. Key players in the U.S. focus on cellulosic and algae-based fuels to achieve deeper emission reductions, leveraging policy support, research incentives, and advanced production technologies to scale operations.

Leading companies in the Global Advanced Biofuel Market include Advance Biofuel, Aemetis, Blue Biofuels, Borregaard, BP, Byogy Renewables, Chevron, Clariant, Enerkem, ExxonMobil, Gevo, GranBio, Green Plains, Galp, Indian Oil Corporation Limited, Logen, Praj Industries, Shell, TotalEnergies, and Votion Biorefineries. Key strategies employed by companies in the Global Advanced Biofuel Market to strengthen their presence include investing in R&D to improve conversion efficiency and feedstock utilization, forming joint ventures with agricultural and industrial partners to secure reliable biomass supply chains, and expanding production facilities globally to reduce delivery times and costs. Firms are leveraging government incentives, blending mandates, and sustainability certification programs to enhance market credibility. They are also deploying innovative process technologies for cellulosic ethanol and algae-based fuels to achieve higher yield and cost-effectiveness. Strategic acquisitions, partnerships, and licensing agreements enable companies to access new technologies, expand market reach, and accelerate commercialization.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Fuel type trends

- 2.4 Feedstock trends

- 2.5 Application trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Cost structure analysis

- 3.6 Price trend analysis (USD/Tons)

- 3.6.1 By fuel type

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Legal factors

- 3.8.6 Environmental factors

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Fuel type, 2022 - 2035 (USD Million & MT)

- 5.1 Key trends

- 5.2 Cellulosic ethanol

- 5.3 Biodiesel

- 5.4 Biobutanol

- 5.5 Others

Chapter 6 Market Size and Forecast, By Feedstock, 2022 - 2035 (USD Million & MT)

- 6.1 Key trends

- 6.2 Agriculture

- 6.3 Forestry

- 6.4 Waste

- 6.5 Others

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & MT)

- 7.1 Key trends

- 7.2 Transportation

- 7.3 Aviation

- 7.4 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MT)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 Spain

- 8.3.4 UK

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Indonesia

- 8.4.4 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 Advance Biofuel

- 9.2 Aemetis

- 9.3 Blue Biofuels

- 9.4 Borregaard

- 9.5 BP

- 9.6 Byogy Renewables

- 9.7 Chevron

- 9.8 Clariant

- 9.9 Enerkem

- 9.10 ExxonMobil

- 9.11 Gevo

- 9.12 GranBio

- 9.13 Green Plains

- 9.14 Galp

- 9.15 Indian Oil Corporation Limited

- 9.16 Logen

- 9.17 Praj Industries

- 9.18 Shell

- 9.19 TotalEnergies

- 9.20 Votion Biorefineries