|

시장보고서

상품코드

1959661

항공기 낙뢰 방지 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Aircraft Lightning Protection Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

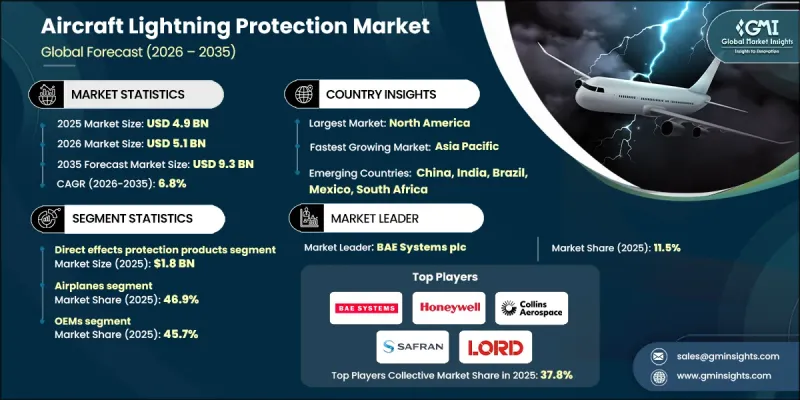

세계의 항공기 낙뢰 방지 시장은 2025년에 49억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 6.8%로 성장하여 93억 달러에 이를 것으로 예측됩니다.

시장 성장은 항공기 생산량 증가, 세계 항공 교통량 증가, 고도의 안전 통합이 필요한 차세대 항공기 플랫폼의 도입에 의해 주도되고 있습니다. 상업용 항공기가 확대되고 여행 수요가 증가함에 따라 항공기 제조업체들은 번개 보호 기술을 포함한 기내 안전 시스템을 강화하는 데 주력하고 있습니다. 보다 엄격한 규제 프레임워크와 인증 기준은 낙뢰와 전기 서지를 견딜 수 있는 고신뢰성 부품의 채택을 더욱 가속화하고 있습니다. 각 업체들은 정밀한 아비오닉스 및 구조 요소를 보호하는 저용량, 고내구성 과도전압 억제 시스템의 연구개발에 투자하고 있습니다. 현대의 기체 구조에 첨단 복합재료가 채택됨에 따라 방전 현상을 효과적으로 관리할 수 있는 전용 보호 시스템의 필요성도 높아지고 있습니다. 항공기 낙뢰 보호에는 전도성 재료, 본딩 네트워크, 보호 기술의 통합이 포함됩니다. 번개 에너지를 안전하게 유도하고, 구조적 무결성을 유지하며, 전기 아키텍처를 보호하고, 지속적인 내공성과 작동 안전성을 보장하도록 설계되었습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 49억 달러 |

| 예측 금액 | 93억 달러 |

| CAGR | 6.8% |

직접 효과 보호 제품 부문은 2025년 18억 달러 시장 규모를 기록할 것으로 예상되며, 2026년부터 2035년까지 연평균 5.8%의 성장률을 보일 것으로 예측됩니다. 항공기 제조업체들이 복합재 기체를 채택하는 경향이 강화되는 가운데, 낙뢰의 직접적인 물리적 영향으로부터 기체를 보호하는 강화 차폐재에 대한 수요가 증가함에 따라 이 부문이 주목받고 있습니다. 직접 효과 보호 솔루션은 고에너지 방전으로 인한 표면 손상, 구조적 약화, 재료 열화를 방지하도록 설계되었습니다. 이러한 시스템은 수리 빈도와 점검으로 인한 다운타임을 최소화하여 기체 신뢰성을 향상시키고 수명주기 비용 효율성을 개선하는 데 기여합니다. 낙뢰 저항에 대한 인증 요건이 강화되면서 첨단 구조 보호 기술에 대한 수요가 더욱 증가하고 있습니다.

2025년에는 항공기 부문이 46.9%의 점유율을 차지할 것으로 예상되며, 이는 고정익 항공기 플랫폼에 대한 피뢰 시스템의 보급을 반영합니다. 항공기 설계에서 복합재료의 사용이 증가하고 전자시스템이 고도화됨에 따라 직격뢰와 간접뢰에 대한 종합적인 보호가 필수적입니다. 통합 보호 아키텍처는 구조적 차폐와 첨단 전기적 접지 및 서지 억제 메커니즘을 결합하여 시스템 수준의 완벽한 안전성을 보장합니다. 항공기 수 증가, 항공기 수명 연장, 지속적인 기술 업그레이드로 인해 민간 항공 분야에서 낙뢰 보호 솔루션에 대한 장기적인 수요가 강화되고 있습니다.

북미 항공 지뢰 보호 시장은 2025년 39.5%의 점유율을 차지하며 주요 지역 시장으로서의 지위를 유지할 것으로 예측됩니다. 이 지역은 항공우주 제조 생태계가 잘 구축되어 있고, 첨단 항공기 생산에 중점을 두고 있다는 장점이 있습니다. 복합재료를 많이 사용하는 항공기 플랫폼의 생산이 증가함에 따라 가볍고 전도성이 높은 보호 소재에 대한 수요가 증가하고 있습니다. 규제 감독과 혁신 주도형 개발이 경쟁 구도를 형성하고 있으며, 제조업체들은 무게 최적화, 성능 신뢰성, 엄격한 안전 기준 준수를 최우선 과제로 삼고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별, 2022-2035

제6장 시장 추산 및 예측 : 기종별, 2022-2035

제7장 시장 추산 및 예측 : 적용 형태별, 2022-2035

제8장 시장 추산 및 예측 : 최종사용자별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

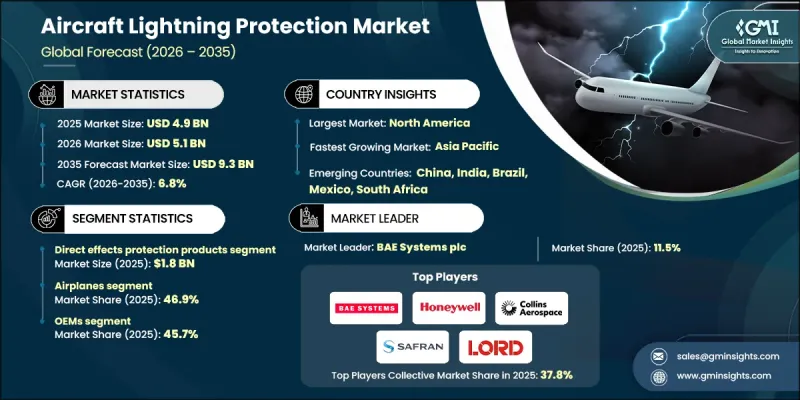

LSH 26.03.16The Global Aircraft Lightning Protection Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 9.3 billion by 2035.

Market growth is fueled by rising aircraft production, increasing global air traffic, and the introduction of next-generation aircraft platforms that require advanced safety integration. As commercial fleets expand and travel demand strengthens, aircraft manufacturers are intensifying efforts to enhance onboard safety systems, including lightning protection technologies. Stricter regulatory frameworks and certification standards are further accelerating the adoption of high-reliability components capable of withstanding lightning strikes and electrical surges. Companies are investing in research and development to engineer low-capacitance, high-durability transient voltage suppression systems that safeguard sensitive avionics and structural elements. The incorporation of advanced composite materials in modern airframes has also elevated the need for specialized protection systems to manage electrical discharge effectively. Aircraft lightning protection involves the integration of conductive materials, bonding networks, and protective technologies designed to safely channel lightning energy, preserving structural integrity, protecting electrical architecture, and maintaining continuous airworthiness and operational safety.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $9.3 Billion |

| CAGR | 6.8% |

The direct effects protection products segment generated USD 1.8 billion in 2025 and is expected to grow at a CAGR of 5.8% between 2026 and 2035. This segment is gaining traction as aircraft manufacturers increasingly utilize composite airframes that require enhanced shielding from the immediate physical impact of lightning strikes. Direct effects protection solutions are engineered to prevent surface damage, structural weakening, and material degradation caused by high-energy electrical discharge. By minimizing repair frequency and inspection downtime, these systems contribute to improved fleet reliability and lifecycle cost efficiency. Rising certification requirements related to lightning strike resilience are further strengthening demand for advanced structural protection technologies.

The airplanes segment accounted for 46.9% share in 2025, reflecting widespread integration of lightning protection systems in fixed-wing aircraft platforms. As aircraft designs incorporate higher volumes of composite materials and more sophisticated electronic systems, comprehensive protection against both direct and indirect lightning effects has become essential. Integrated protection architectures combine structural shielding with advanced electrical grounding and surge suppression mechanisms to ensure complete system-level safety. Growing fleet sizes, extended service life of aircraft, and continuous technological upgrades are reinforcing long-term demand for lightning protection solutions across commercial aviation.

North America Aircraft Lightning Protection Market held 39.5% share in 2025, maintaining its position as the leading regional market. The region benefits from a well-established aerospace manufacturing ecosystem and a strong focus on advanced aircraft production. The increasing output of composite-intensive aircraft platforms has elevated demand for lightweight and highly conductive protection materials. Regulatory oversight and innovation-driven development continue to shape the competitive landscape, with manufacturers prioritizing weight optimization, performance reliability, and compliance with rigorous safety standards.

Key companies operating in the Global Aircraft Lightning Protection Market include Honeywell International Inc., BAE Systems plc, Collins Aerospace (Raytheon Technologies), Safran S.A., LORD Corporation, Spirit AeroSystems, Inc., Meggitt PLC, GKN Aerospace, Triumph Group, Inc., Elbit Systems Ltd., Moog Inc., Ferrostaal GmbH, ATEC GmbH, and Aero Vodochody AEROSPACE a.s. Companies in the Aircraft Lightning Protection Market are strengthening their competitive position through continuous technological advancement and strategic partnerships with airframe manufacturers. Investment in research and development remains a primary strategy, with firms focusing on lightweight conductive materials, advanced bonding techniques, and enhanced transient voltage suppression systems. Collaboration with OEMs during early aircraft design phases ensures system integration and long-term supply agreements. Businesses are also expanding manufacturing capabilities to meet rising aircraft production rates while maintaining strict compliance with aviation safety certifications. Portfolio diversification across direct and indirect protection systems enables companies to address evolving aircraft architecture requirements.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Aircraft type trends

- 2.2.3 Protection type trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing aircraft production and R&D for lightning protection

- 3.2.1.2 Growing demand for low-cost carriers and development of cost-effective solutions

- 3.2.1.3 Growing air passenger traffic and defense aircrafts

- 3.2.1.4 Increasing demand for single aisle aircraft fleet coupled with infrastructure development

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with aircraft manufacturing set up for lightning protection

- 3.2.2.2 Complexity in retrofitting

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of composite-intensive aircraft structures

- 3.2.3.2 Aftermarket retrofitting and MRO-driven upgrades

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Supply chain resilience

- 3.11 Geopolitical analysis

- 3.12 Workforce analysis

- 3.13 Digital transformation

- 3.14 Mergers, acquisitions, and strategic partnerships landscape

- 3.15 Risk assessment and management

- 3.16 Major contract awards (2022-2025)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.2 Direct effects protection products

- 5.2.1 Expanded metal foils

- 5.2.2 Conductive meshes

- 5.2.3 Diverter strips & strike terminals

- 5.2.4 Others

- 5.3 Indirect effects protection products

- 5.3.1 Transient voltage suppressors

- 5.3.2 Lightning-specific shielded connectors

- 5.3.3 Others

- 5.4 Bonding & grounding products

- 5.4.1 Bonding straps & jumpers

- 5.4.2 Grounding straps & bus bars

- 5.4.3 Static discharge wicks

Chapter 6 Market Estimates and Forecast, By Aircraft Type, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Airplanes

- 6.2.1 Commercial transport aircraft

- 6.2.2 Military transport

- 6.2.3 Others

- 6.3 Rotorcraft

- 6.3.1 Civil helicopters

- 6.3.2 Government & military helicopters

- 6.4 Unmanned aerial systems (UAS)

- 6.4.1 Tactical drones

- 6.4.2 Hale/male UAVs

- 6.4.3 Commercial drones

- 6.5 Electric & hybrid-electric aircraft

- 6.6 Powered-lift aircraft

- 6.7 Gliders

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Fit, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 Line-fit

- 7.3 Retrofit

Chapter 8 Market Estimates and Forecast, By End User, 2022 - 2035 ($ Bn)

- 8.1 Key trends

- 8.2 OEMs (original equipment manufacturers)

- 8.3 Tier 1 & tier 2 suppliers

- 8.4 MRO (maintenance, repair & overhaul)

- 8.5 Aftermarket & retrofit

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 BAE Systems plc

- 10.1.2 Honeywell International Inc.

- 10.1.3 Collins Aerospace (Raytheon Technologies)

- 10.1.4 Safran S.A.

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 LORD Corporation

- 10.2.1.2 Spirit AeroSystems, Inc.

- 10.2.1.3 Triumph Group, Inc.

- 10.2.2 Europe

- 10.2.2.1 ATEC GmbH

- 10.2.2.2 Meggitt PLC

- 10.2.2.3 GKN Aerospace

- 10.2.3 APAC

- 10.2.3.1 Elbit Systems Ltd.

- 10.2.3.2 Moog Inc.

- 10.2.3.3 Aero Vodochody AEROSPACE a.s.

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Ferrostaal GmbH