|

시장보고서

상품코드

1982260

데이터센터 열교환기 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Data Center Heat Exchanger Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

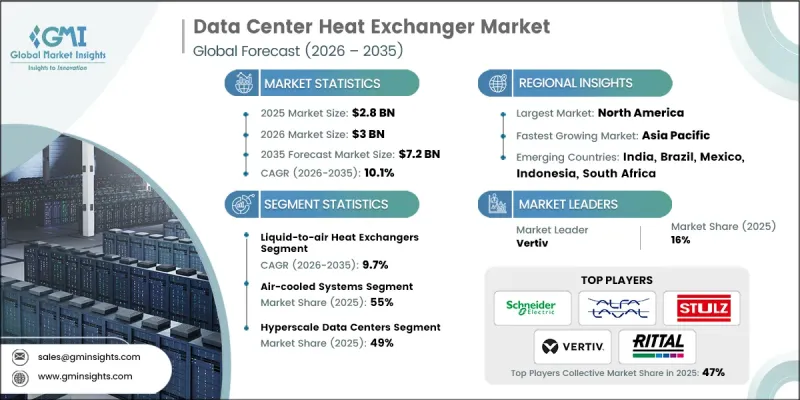

세계의 데이터센터 열교환기 시장은 2025년 28억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 10.1%를 나타낼 것으로 보이며, 72억 달러에 이를 것으로 추정됩니다.

첨단 열 관리 기술이 디지털 인프라 성능에 있어 핵심 요소로 부상함에 따라 해당 산업은 강력한 성장세를 보이고 있습니다. 인공지능(AI) 애플리케이션, 클라우드 환경 및 분산 컴퓨팅 아키텍처가 지속적으로 확장됨에 따라 데이터센터 운영업체들은 효율적이고 지속 가능한 냉각 기술을 최우선 과제로 삼고 있습니다. 열교환기는 이제 가동 시간 유지, 전력 사용 효율 최적화, 그리고 더 높은 랙 밀도 지원에 핵심적인 역할을 수행하고 있습니다. 이 시장은 후면 도어 시스템, 인-로우(in-row) 플랫폼 및 다이렉트-투-칩(direct-to-chip) 액체 냉각 아키텍처에 통합된 공기-공기, 액체-액체 및 냉매 기반 기술을 포괄합니다. 30-100kW를 초과하는 랙 전력 밀도의 증가는 기존 공기 기반 모델에서 액체 및 하이브리드 시스템으로의 전환을 가속화하고 있습니다. AI 프로세서와 고성능 컴퓨팅 컴포넌트의 광범위한 도입은 열 전달을 개선하면서 물과 에너지 소비를 최소화하도록 설계된 소형 판형 및 마이크로채널 열교환기에 대한 수요를 더욱 높이고 있습니다. 또한 규제 압력, 비용 효율성 목표, 하이퍼스케일 및 코로케이션 시설의 지속적인 혁신도 시장 성장을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시장 규모 | 28억 달러 |

| 예측 금액 | 72억 달러 |

| CAGR | 10.1% |

액체-공기 열교환기 부문은 2025년 시장 점유율의 54%를 차지했으며, 2026년부터 2035년까지 연평균 성장률(CAGR) 9.7%로 성장할 것으로 예상됩니다. 이 부문은 후면 도어 열교환기, 냉수 기반 공기 처리 시스템, 통합 코일 기술을 포함하여 많은 데이터센터의 기초적인 냉각 방식을 대표합니다. 이러한 솔루션은 물의 뛰어난 열 흡수 능력을 활용하여, 서버 배기 공기의 열 에너지를 특수 설계된 열교환 표면을 통해 전달한 후, 냉각된 공기를 시설 내부로 재순환시킵니다. 기존 인프라와의 호환성이 확립되어 있어 계속해서 광범위한 채택을 이끌고 있습니다.

공기 냉각 시스템 부문은 2025년 55%의 점유율을 기록했으며, 2035년까지 연평균 성장률(CAGR) 9.8%로 성장할 것으로 전망됩니다. 이 부문에는 직접 팽창 냉매 기술, 냉수식 공기 처리기, 독립형 냉각기, 이코노마이저 기반 자연 냉각 구성이 포함됩니다. 업계 내 오랜 인지도, 입증된 신뢰성, 그리고 이중 바닥 공기 흐름 설계와의 호환성은 이들의 우위를 공고히 했습니다. 공기 냉각 플랫폼은 랙당 5-15kW로 운영되는 기업 환경에서 특히 효과적이며, 이러한 환경에서는 설치 비용과 운영의 간편성이 여전히 주요 고려 사항으로 남아 있습니다.

미국의 데이터센터 열교환기 시장은 2025년에 7억 8,210만 달러의 규모가 되어, 2026년부터 2035년에 걸쳐 CAGR 9.4%로 성장할 것으로 추정되고 있습니다. 시장 주도력은 지속적인 하이퍼스케일 개발, 엄격한 에너지 효율 규정, 연방 규제 기관의 감독에 힘입고 있습니다. 컴퓨팅 집약적 워크로드와 디지털 서비스에 대한 수요 증가로 고성능 냉각 기술로의 전환이 가속화되고 있으며, 액체-공기 열교환기는 안정적이고 에너지 효율적인 작동으로 인정받고 있습니다.

경쟁 구도에는 Airedale, Alfa Laval, CoolIT Systems, Eaton, Munters, Nortek Air, Rittal, Schneider Electric, STULZ, Vertiv와 같은 주요 업계 참여자들이 포함되어 있으며, 이들 모두 제품 혁신과 글로벌 시장 확장에 기여하고 있습니다. 글로벌 데이터센터 열교환기 시장에서 활동하는 기업들은 기술 혁신, 전략적 파트너십, 생산 능력 확대 계획을 통해 시장 입지를 강화하고 있습니다. 제연구들은 고밀도 데이터센터에 최적화된 첨단 액체 냉각 시스템, 소형 마이크로채널 설계, 에너지 효율적인 하이브리드 솔루션을 도입하기 위해 연구 개발에 막대한 투자를 하고 있습니다. 데이터센터 개발사 및 인프라 제산업체와의 전략적 협력을 통해 맞춤형 열 관리 시스템을 조기에 통합할 수 있게 되었습니다. 또한 기업들은 북미 및 기타 고성장 지역의 증가하는 수요를 충족하기 위해 제조 시설과 지역 유통망을 확장하고 있습니다. 아울러 기업들은 규제 당국의 기대와 기업의 ESG 약속에 부합하도록, 물 소비량과 탄소 배출량을 줄이는 지속 가능성 중심의 제품 개선에 주력하고 있습니다.

자주 묻는 질문

목차

제1장 연구 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- AI 및 고성능 컴퓨팅 워크로드의 기하급수적 증가

- 증가하는 열 밀도(50-100kW 랙) 및 GPU 발열량(칩당 1,200W 이상)

- 지속가능성 의무 및 탄소 중립 목표

- 현대적 워크로드에 대한 기존 공기 냉각 냉각 방식의 한계

- 하이퍼스케일 데이터센터 확장

- 에너지 비용 절감 압력

- 업계의 잠재적 위험 및 과제

- 액체 냉각 인프라에 대한 높은 초기 자본 투자 요구

- 물 사용량에 관한 우려

- 기존 공기 냉각 인프라와의 통합 과제

- 액체 냉각 설치 및 유지보수를 위한 숙련된 인력 부족

- 전자 기기 주변으로의 액체 유입에 대한 위험 회피

- 시장 기회

- 기존 데이터센터의 개조 시장

- 엣지 및 마이크로 데이터센터 냉각 솔루션

- 폐열 회수 및 재사용 용도

- 모듈형 및 조립식 냉각 장치

- 극한 기온 환경을 위한 기후 회복력 있는 냉각

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국 난방냉동공조학회(ASHRAE)

- 미국 에너지부(DOE)

- 유럽

- 유럽위원회

- Eurovent Certita 인증

- 아시아태평양

- 싱가포르 건설국(BCA)

- 일본산업규격(JIS)

- 라틴아메리카

- 브라질 기술 표준 협회

- 국가에너지위원회

- 중동 및 아프리카

- 아랍에미리트(UAE)(UAE) 에너지 및 인프라성

- 사우디아라비아 규격 및 계량 및 품질 기구(SASO)

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 특허 분석

- 특허출원 동향(2021-2025)

- 주요 특허 보유자

- 가격 분석 및 비용 구조

- 기술 유형별 가격 동향

- 지역별 가격 변동

- 원가 내역 분석

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고찰

- 총소유비용(TCO) 분석

- 이용 사례와 성공 사례

- 앞으로의 전망과 새로운 동향

- 차세대 냉각 솔루션(액침 냉각, 2상 냉각, 극저온 냉각)

- AI를 활용한 예측 열 관리

- 순환형 경제와 열재사용 가능성

- 스마트 모듈형 및 엣지 대응 인프라

- 운영 효율과 최적화

- 에너지 최적화 기법

- 수명 주기 비용 관리

- 보수 및 예측 유지보수의 실천

- 빌딩 관리 시스템(BMS)과의 제휴

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카(MEA)

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 열교환기 기술별(2022-2035년)

- 액체-공기 열교환기

- 액체-액체 열교환기

- 하이브리드 열교환기

제6장 시장 추계 및 예측 : 냉각 방식별(2022-2035년)

- 공기 냉각 시스템

- 액체 냉각 시스템

- 하이브리드 공기/액체 솔루션

제7장 시장 추계 및 예측 : 냉각 도입 구성별(2022-2035년)

- 후면 도어 열교환기(RDHx)

- 인로우 냉각 장치

- 콜드 플레이트

- 침지 냉각 시스템

제8장 시장 추계 및 예측 : 용도별(2022-2035년)

- 서버 냉각

- 파워 일렉트로닉스 냉각(UPS, PDU)

- HVAC 시스템 통합

- 환기 및 공기 교환

- 에너지 회수/폐열 재사용

- 기타

제9장 시장 추계 및 예측 : 데이터센터별(2022-2035년)

- 하이퍼스케일 데이터센터

- 엔터프라이즈 데이터센터

- 코로케이션 및 데이터센터

- 엣지/마이크로 데이터센터

제10장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 네덜란드

- 스웨덴

- 덴마크

- 폴란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 싱가포르

- 태국

- 인도네시아

- 베트남

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 중동 및 아프리카(MEA)

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 이스라엘

제11장 기업 프로파일

- 세계 기업

- Airedale

- Alfa Laval

- Emerson

- Mitsubishi Heavy Industries

- Munters

- Nortek Air

- Rittal

- Schneider Electric

- STULZ

- Vertiv

- 지역 기업

- Baltimore Aircoil Company(BAC)

- Coolcentric

- Fujitsu

- Hitachi

- Legrand(ColdLogik)

- Motivair

- USystems

- 신흥 기업 및 기술 기반 기업

- CoolIT Systems

- Green Revolution Cooling(GRC)

- ZutaCore

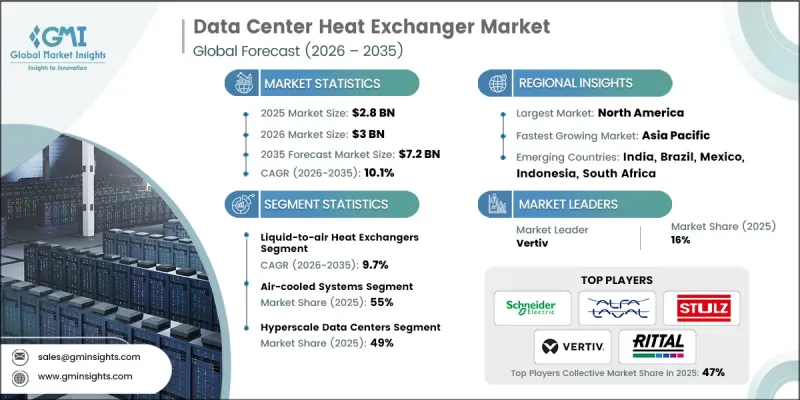

The Global Data Center Heat Exchanger Market was valued at USD 2.8 billion in 2025 and is estimated to grow at a CAGR of 10.1% to reach USD 7.2 billion by 2035.

The industry is gaining strong momentum as advanced thermal management becomes critical to digital infrastructure performance. As artificial intelligence applications, cloud environments, and distributed computing architectures continue to scale, data center operators are prioritizing efficient and sustainable cooling technologies. Heat exchangers now play a central role in maintaining uptime, optimizing power usage effectiveness, and supporting higher rack densities. The market covers air-to-air, liquid-to-liquid, and refrigerant-based technologies integrated into rear-door systems, in-row platforms, and direct-to-chip liquid cooling architectures. Increasing rack power densities exceeding 30-100 kW are accelerating the transition from legacy air-based models toward liquid and hybrid systems. The widespread deployment of AI processors and high-performance computing components is further elevating demand for compact plate and microchannel heat exchangers designed to improve thermal transfer while minimizing water and energy consumption. Growth is also supported by regulatory pressure, cost efficiency goals, and continuous innovation in hyperscale and colocation facilities.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.8 Billion |

| Forecast Value | $7.2 Billion |

| CAGR | 10.1% |

The liquid-to-air heat exchangers segment accounted for 54% share in 2025 and is anticipated to grow at a CAGR of 9.7% between 2026 and 2035. This category represents the foundational cooling approach within many data centers, incorporating rear-door heat exchangers, chilled-water-based air handling systems, and integrated coil technologies. These solutions rely on water's strong heat absorption capacity, transferring thermal energy from server exhaust air through engineered exchange surfaces before recirculating conditioned air back into the facility. Their established infrastructure compatibility continues to drive widespread adoption.

The air-cooled systems segment held a 55% share in 2025 and is forecast to grow at a CAGR of 9.8% through 2035. This segment includes direct expansion refrigerant technologies, chilled water air handlers, standalone chillers, and economizer-based free cooling configurations. Long-standing industry familiarity, proven reliability, and compatibility with raised-floor airflow designs have reinforced their dominance. Air-cooled platforms remain particularly effective for enterprise environments operating at 5-15 kW per rack, where installation costs and operational simplicity remain primary considerations.

United States Data Center Heat Exchanger Market generated USD 782.1 million in 2025 and is estimated to grow at a CAGR of 9.4% during 2026-2035. Market leadership is supported by continued hyperscale development, strict energy efficiency mandates, and oversight from federal regulatory bodies. Rising demand for compute-intensive workloads and digital services is accelerating the shift toward high-performance cooling technologies, with liquid-to-air heat exchangers recognized for dependable and energy-efficient operation.

The competitive landscape includes key industry participants such as Airedale, Alfa Laval, CoolIT Systems, Eaton, Munters, Nortek Air, Rittal, Schneider Electric, STULZ, and Vertiv, all contributing to product innovation and global market expansion. Companies operating in the Global Data Center Heat Exchanger Market are strengthening their market position through technology innovation, strategic partnerships, and capacity expansion initiatives. Manufacturers are investing heavily in research and development to introduce advanced liquid cooling systems, compact microchannel designs, and energy-efficient hybrid solutions tailored for high-density data centers. Strategic collaborations with data center developers and infrastructure providers enable early integration of customized thermal management systems. Firms are also expanding manufacturing facilities and regional distribution networks to meet growing demand across North America and other high-growth regions. In addition, companies are focusing on sustainability-driven product enhancements that reduce water consumption and carbon emissions, aligning with regulatory expectations and enterprise ESG commitments.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Heat Exchanger Technology

- 2.2.3 Cooling Mechanisms

- 2.2.4 Cooling Deployment Configuration

- 2.2.5 Application

- 2.2.6 Data Centers

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Exponential growth in AI and high-performance computing workloads

- 3.2.1.2 Rising thermal density (50-100 kW racks) and GPU heat generation (1,200 W+ per chip)

- 3.2.1.3 Sustainability mandates and net-zero carbon emission targets

- 3.2.1.4 Inadequacy of traditional air-cooling for modern workloads

- 3.2.1.5 Hyperscale data center expansion

- 3.2.1.6 Energy cost reduction pressure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital investment requirements for liquid-cooling infrastructure

- 3.2.2.2 Water consumption concerns

- 3.2.2.3 Integration challenges with legacy air-cooled infrastructure

- 3.2.2.4 Skilled workforce shortage for liquid-cooling installation and maintenance

- 3.2.2.5 Risk aversion to liquid near electronic equipment

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit market for legacy data centers

- 3.2.3.2 Edge and micro data center cooling solutions

- 3.2.3.3 Waste heat recovery and reuse applications

- 3.2.3.4 Modular and prefabricated cooling units

- 3.2.3.5 Climate-resilient cooling for extreme-temperature environments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 American society of heating, refrigerating and air-conditioning engineers (ASHRAE)

- 3.4.1.2 US department of energy (DOE)

- 3.4.2 Europe

- 3.4.2.1 European commission

- 3.4.2.2 Eurovent certita certification

- 3.4.3 Asia Pacific

- 3.4.3.1 Building and construction authority (BCA), Singapore

- 3.4.3.2 Japanese industrial standards (JIS)

- 3.4.4 LATAM

- 3.4.4.1 Brazilian association of technical standards

- 3.4.4.2 National energy commission

- 3.4.5 MEA

- 3.4.5.1 UAE ministry of energy and infrastructure

- 3.4.5.2 Saudi standards, metrology and quality organization (SASO)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.8.1 Patent filing trends (2021-2025)

- 3.8.2 Key patent holders

- 3.9 Pricing analysis & cost structure

- 3.9.1 Price trends by technology type

- 3.9.2 Regional price variations

- 3.9.3 Cost breakdown analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Total cost of ownership (tco) analysis

- 3.12 Use cases & success stories

- 3.13 Future outlook & emerging trends

- 3.13.1 Next-generation cooling solutions (immersion, two-phase, cryogenic)

- 3.13.2 AI-enabled predictive thermal management

- 3.13.3 Circular economy & heat reuse potential

- 3.13.4 Smart modular & edge-ready infrastructure

- 3.14 Operational efficiency & optimization

- 3.14.1 Energy optimization techniques

- 3.14.2 Lifecycle cost management

- 3.14.3 Maintenance & predictive monitoring practices

- 3.14.4 Integration with building management systems (BMS)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Heat Exchanger Technology, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Liquid-to-air heat exchangers

- 5.3 Liquid-to-liquid heat exchangers

- 5.4 Hybrid heat exchangers

Chapter 6 Market Estimates & Forecast, By Cooling Mechanisms, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Air-cooled systems

- 6.3 Liquid-cooled systems

- 6.4 Hybrid air/liquid solutions

Chapter 7 Market Estimates & Forecast, By Cooling Deployment Configuration, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Rear door heat exchangers (RDHx)

- 7.3 In-row cooling units

- 7.4 Direct-to-chip liquid cooling (Cold Plates)

- 7.5 Immersion cooling systems

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Server cooling

- 8.3 Power electronics cooling (UPS, PDUs)

- 8.4 HVAC systems integration

- 8.5 Ventilation & air exchange

- 8.6 Energy recovery / waste heat reuse

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Data Centers, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Hyperscale data centers

- 9.3 Enterprise data centers

- 9.4 Colocation data centers

- 9.5 Edge/micro data centers

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Airedale

- 11.1.2 Alfa Laval

- 11.1.3 Emerson

- 11.1.4 Mitsubishi Heavy Industries

- 11.1.5 Munters

- 11.1.6 Nortek Air

- 11.1.7 Rittal

- 11.1.8 Schneider Electric

- 11.1.9 STULZ

- 11.1.10 Vertiv

- 11.2 Regional Players

- 11.2.1 Baltimore Aircoil Company (BAC)

- 11.2.2 Coolcentric

- 11.2.3 Fujitsu

- 11.2.4 Hitachi

- 11.2.5 Legrand (ColdLogik)

- 11.2.6 Motivair

- 11.2.7 USystems

- 11.3 Emerging Players & Technology Enablers

- 11.3.1 CoolIT Systems

- 11.3.2 Green Revolution Cooling (GRC)

- 11.3.3 ZutaCore