|

시장보고서

상품코드

1982262

청각 및 전정 진단 장비 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Audiology and Vestibular Diagnostic Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

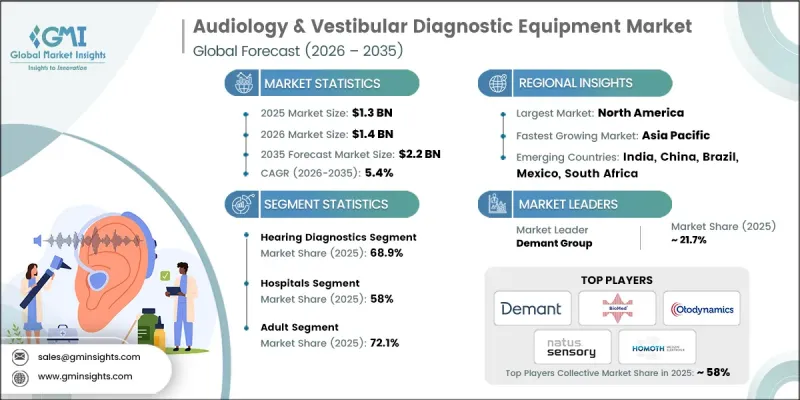

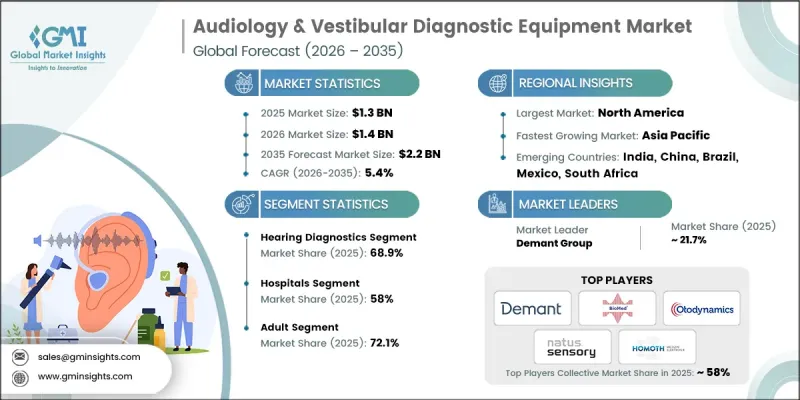

세계의 청각 및 전정 진단 장비 시장은 2025년에 13억 달러로 평가되었고, CAGR은 5.4%를 나타낼 것으로 보이며, 2035년까지 22억 달러에 이를 것으로 추정되고 있습니다.

시장 확대는 청각 및 전정 장애의 발생률 증가, 급속히 확대되는 고령 인구, 그리고 진단 플랫폼의 지속적인 기술 발전에 힘입고 있습니다. 이러한 의료 기기는 임상 및 병원 환경에서 청력 능력과 균형 기능을 평가하도록 설계되었습니다. 이 산업은 정밀도와 운영 효율성을 높이는 자동화 및 휴대용 시스템, 무선 지원 솔루션, 그리고 인공지능 기반 진단 플랫폼의 개발로 인해 혜택을 보고 있습니다. 최신 장비는 전자 의료 기록 시스템과의 연동성을 개선하는 동시에, 간소화되고 환자 중심적이며 데이터 지향적인 평가를 지원합니다. 현장 진단(Point-of-Care Diagnostics)에 대한 수요 증가, 의료 전반의 디지털 전환, 소아 및 노인 인구의 조기 발견에 대한 관심 증대가 업계 성장 동력에 기여하고 있습니다. 시장은 점차 연결되고 소프트웨어 중심의 진단 기술로 전환되고 있으며, 실시간 분석 및 장기적인 환자 모니터링을 가능하게 하는 스마트 클라우드 기반 시스템으로 기존의 독립형 장치를 대체하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시장 규모 | 13억 달러 |

| 예측 금액 | 22억 달러 |

| CAGR | 5.4% |

2025년 청력 진단 부문은 68.9%의 점유율을 차지했습니다. 이러한 선도적 위상은 세계적으로 높은 청각 장애 부담, 조기 검진 프로그램의 광범위한 시행, 정기적인 청력 평가에 대한 꾸준한 수요, 그리고 의료 시설 전반에 걸친 임상적 활용이 뒷받침하고 있습니다. 청력 진단 시스템은 또한 청각 보조 기술의 보정, 최적화 및 지속적인 관리를 지원하는 데 중요한 역할을 합니다. 보조 청각 기기의 채택이 증가함에 따라 정확한 역치 측정 및 언어 평가 도구에 대한 필요성도 계속 커지고 있습니다. 지속적인 모니터링 요구 사항은 진단 플랫폼의 반복 사용에 더욱 기여하고 있습니다.

성인 부문은 2025년 72.1%의 점유율을 차지했으며, 2026년부터 2035년 사이에 15억 달러에 달할 것으로 전망됩니다. 40세 이상 인구 중 노화 관련 요인, 환경적 노출 및 생활 방식의 영향으로 청력 저하를 경험하는 비율이 증가함에 따라 정기적인 진단 검사에 대한 수요가 높아지고 있습니다. 청각 문제를 조기에 발견하면 의사소통 능력과 전반적인 삶의 질이 향상되어 전문적인 평가에 대한 참여가 증가합니다. 또한 나이가 들수록 균형 관련 문제가 더 흔해지면서 전문적인 전정 기능 평가 기술에 대한 필요성이 커지고 있습니다. 이러한 진단 요구 사항은 성인 중심 의료 서비스 전반에 걸쳐 수요를 강화하고 있습니다.

북미의 청각 및 전정 진단 장비 시장은 2025년 35.3%의 점유율을 차지했습니다. 이 지역 전반에 걸친 강력한 의료 지출은 첨단 진단 인프라에 대한 투자를 뒷받침하고 있습니다. 기존 전문 진료과들은 고정밀도 및 디지털 통합 시스템을 우선시하여 지속적인 업그레이드와 현대화를 촉진하고 있습니다. 견고한 보험 급여 체계는 공공 및 민간 의료 환경 모두에서 장비 활용도를 높입니다. 또한 이 지역은 원격 진단 기능과 환자의 전문 서비스 접근성을 확대하는 연결형 진료 모델을 포함한 디지털 헬스 혁신 분야에서 선도적인 위치를 차지하고 있습니다.

자주 묻는 질문

목차

제1장 연구 방법

- 연구 접근

- 품질에 관한 대처

- GMI AI 정책 및 데이터 무결성에 대한 노력

- 출처 일관성 프로토콜

- GMI AI 정책 및 데이터 무결성에 대한 노력

- 연구의 경위와 신뢰도 평가

- 연구 경로 컴포넌트

- 평가 컴포넌트

- 데이터 수집

- 1차 정보의 일부 리스트

- 데이터 마이닝 출처

- 유료 출처

- 지역별 출처

- 유료 출처

- 기본 추정 및 산출 방법

- 특정 접근 방식에 대한 기준 연도 계산

- 예측 모델

- 정량화된 시장 영향 분석

- 성장 매개변수가 예측에 미치는 수학적 영향

- 정량화된 시장 영향 분석

- 연구의 투명성에 관한 보충

- 출처의 귀속 프레임워크

- 품질 보증 지표

- 신뢰에 대한 노력

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 청력 손실 및 전정 장애 유병률 증가

- 각학 및 전정 진단 분야의 기술 발전

- 조기 청력 및 전정 장애 진단에 대한 인식 제고

- 신생아 및 소아 청력 선별 검사 프로그램 확대

- 업계의 잠재적 위험 및 과제

- 첨단 진단 장비의 높은 비용

- 저소득 및 중소득 지역의 낮은 도입률

- 시장 기회

- 원격 청각학 및 원격 진단 솔루션의 확대

- 휴대용 및 현장 진단 기기에 대한 수요 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술 동향

- 현재의 기술 동향

- 신흥 기술

- 상환 시나리오

- 장래 시장 동향

- 투자환경

- Porter's Five Forces 분석

- PESTEL 분석

- 고객 인사이트

- 스타트업 시나리오

- 갭 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 제품별(2022-2035년)

- 청각 진단

- 청력 측정 시스템

- 고막 측정 시스템

- 이음파 방출(OAE) 시스템

- 기타 청각 진단

- 전정 기능 진단

- VNG 시스템

- VEMP 시스템

- 자세 평가 시스템

- vHIT 시스템

- 기타 전정기능 진단

제6장 시장 추계 및 예측 : 환자별(2022-2035년)

- 성인

- 소아

제7장 시장 추계 및 예측 : 최종 용도별(2022-2035년)

- 병원

- 청각 클리닉

- 기타 최종 사용자

제8장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Bertec

- BioMed Jena

- Demant Group

- Echodia

- Guangzhou Melison Medical Instrument

- hearX

- Homoth Medizinelektronik

- Intelligent Hearing Systems

- Labat Asia

- Natus Sensory

- Neurosoft

- Otodynamics

- Otopront

- PATH MEDICAL

- RION

The Global Audiology & Vestibular Diagnostic Equipment Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 2.2 billion by 2035.

Market expansion is driven by the increasing incidence of auditory and vestibular disorders, a rapidly expanding aging population, and continuous technological advancements in diagnostic platforms. These medical devices are designed to assess hearing capability and balance function in clinical and hospital environments. The industry is benefiting from the development of automated and portable systems, wireless-enabled solutions, and artificial intelligence-based diagnostic platforms that enhance precision and operational efficiency. Modern equipment supports streamlined, patient-centric, and data-oriented assessments while improving integration with electronic medical record systems. Growing demand for point-of-care diagnostics, digital transformation across healthcare, and stronger focus on early detection in pediatric and geriatric populations are contributing to industry momentum. The market is steadily transitioning toward connected and software-driven diagnostic technologies, replacing conventional standalone devices with smart, cloud-enabled systems that enable real-time analytics and long-term patient monitoring.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 5.4% |

The hearing diagnostics segment accounted for a 68.9% share in 2025. This leadership position is supported by the high global burden of hearing disorders, broad implementation of early screening initiatives, consistent demand for routine hearing evaluations, and widespread clinical utilization across healthcare facilities. Hearing diagnostic systems also play a critical role in supporting the calibration, optimization, and ongoing management of hearing assistance technologies. As the adoption of supportive auditory devices increases, the need for accurate threshold measurement and speech assessment tools continues to grow. Ongoing monitoring requirements further contribute to repeat usage of diagnostic platforms.

The adult segment represented a 72.1% share in 2025 and is projected to reach USD 1.5 billion during 2026-2035. A growing proportion of individuals aged 40 and above are experiencing auditory decline due to age-related factors, environmental exposure, and lifestyle influences, prompting higher demand for routine diagnostic testing. Early identification of hearing challenges enhances communication outcomes and overall quality of life, encouraging greater participation in professional evaluations. Balance-related concerns also become more prevalent with age, driving the need for specialized vestibular assessment technologies. These diagnostic requirements are strengthening demand across adult-focused healthcare services.

North America Audiology & Vestibular Diagnostic Equipment Market captured 35.3% share in 2025. Strong healthcare expenditure across the region supports investment in advanced diagnostic infrastructure. Established specialty departments prioritize high-accuracy and digitally integrated systems, encouraging ongoing upgrades and modernization. Robust reimbursement structures enhance equipment utilization across both public and private healthcare settings. The region also demonstrates leadership in digital health innovation, including remote diagnostic capabilities and connected care models that expand patient access to specialized services.

Key participants in the Global Audiology & Vestibular Diagnostic Equipment Market include PATH MEDICAL, Demant Group, Natus Sensory, hearX, Otodynamics, Neurosoft, Bertec, Homoth Medizinelektronik, Otopront, Guangzhou Melison Medical Instrument, Echodia, Intelligent Hearing Systems, Labat Asia, RION, and BioMed Jena. Companies operating in the Audiology & Vestibular Diagnostic Equipment Market are reinforcing their competitive positions through continuous product innovation, strategic collaborations, and global expansion initiatives. Significant investments in research and development are enabling the introduction of AI-driven and digitally connected diagnostic platforms that enhance clinical accuracy and workflow efficiency. Many organizations are expanding their portable and point-of-care product portfolios to address rising demand for flexible diagnostic solutions. Partnerships with healthcare providers and technology firms are strengthening integration with electronic medical records and telehealth systems. Market players are also focusing on geographic expansion into emerging healthcare markets while enhancing distribution networks.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Patient trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of hearing loss and balance disorders

- 3.2.1.2 Technological advancements in audiology and vestibular diagnostics

- 3.2.1.3 Growing awareness of early hearing and vestibular disorder diagnosis

- 3.2.1.4 Expansion of newborn and pediatric hearing screening programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced diagnostic equipment

- 3.2.2.2 Low adoption in low- and middle-income regions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of tele-audiology and remote diagnostic solutions

- 3.2.3.2 Growing demand for portable and point-of-care diagnostic devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Future market trends

- 3.8 Investment landscape

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Customer insights

- 3.12 Start-up scenarios

- 3.13 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Hearing diagnostics

- 5.2.1 Audiometry systems

- 5.2.2 Tympanometry systems

- 5.2.3 Otoacoustic emissions (OAE) systems

- 5.2.4 Other hearing diagnostics

- 5.3 Vestibular diagnostics

- 5.3.1 VNG systems

- 5.3.2 VEMP systems

- 5.3.3 Posturography systems

- 5.3.4 vHIT systems

- 5.3.5 Other vestibular diagnostics

Chapter 6 Market Estimates and Forecast, By Patient, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Adult

- 6.3 Pediatric

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Audiology clinics

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Bertec

- 9.2 BioMed Jena

- 9.3 Demant Group

- 9.4 Echodia

- 9.5 Guangzhou Melison Medical Instrument

- 9.6 hearX

- 9.7 Homoth Medizinelektronik

- 9.8 Intelligent Hearing Systems

- 9.9 Labat Asia

- 9.10 Natus Sensory

- 9.11 Neurosoft

- 9.12 Otodynamics

- 9.13 Otopront

- 9.14 PATH MEDICAL

- 9.15 RION