|

시장보고서

상품코드

1982278

전분석 자동화 시장 : 성장 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Pre Analytical Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

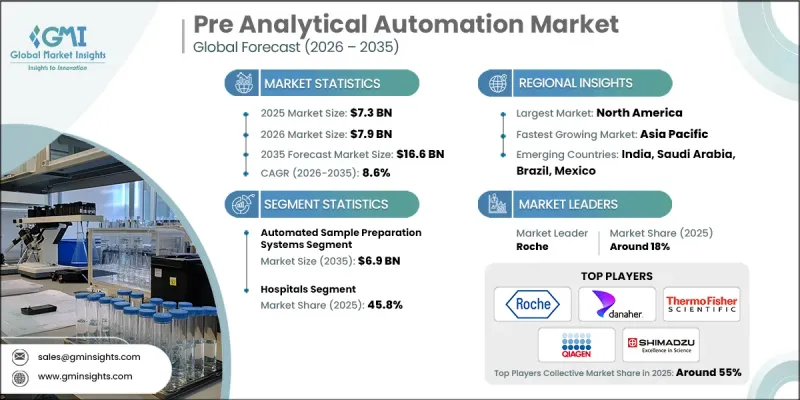

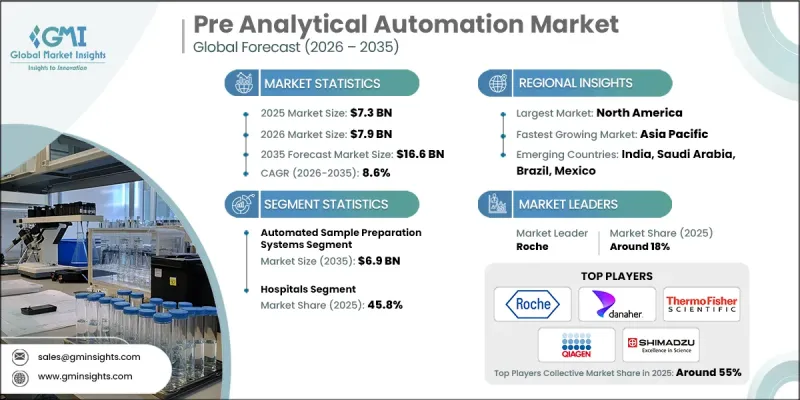

세계의 전분석 자동화 시장은 2025년 73억 달러로 평가되었고, CAGR은 8.6%를 나타낼 것으로 보이며, 2035년까지 166억 달러에 이를 것으로 추정됩니다.

시장 성장은 진단 검사 건수의 꾸준한 증가, 실험실 자동화에 대한 수요 확대, 그리고 검사 결과 제공 속도를 높이기 위한 첨단 실험실 장비에 대한 자본 투자 증가에 힘입어 가속화되고 있습니다. 세계의 임상 실험실은 정확성과 품질 기준을 유지하면서 운영 효율성을 높여야 한다는 압박을 점점 더 많이 받고 있습니다. 조기 질병 발견에 대한 요구와 만성 및 급성 질환의 증가하는 부담이 맞물리면서 매일 처리되는 검사 건수가 크게 늘어났습니다. 현재 및 예상되는 업무량을 관리하기 위해 실험실들은 디지털 전환 이니셔티브를 가속화하고 운영 체계 내에 상호 연결된 자동화 플랫폼을 도입하고 있습니다. 최신 전분석 자동화 시스템은 검체 처리 과정을 간소화하고, 워크플로우의 연속성을 개선하며, 수동 개입을 줄여줍니다. 이러한 솔루션은 더 높은 처리 용량을 지원하고, 검체 이동을 최적화하며, 긴급 사례를 우선 처리하고, 인력 요구량을 비례적으로 늘리지 않으면서 처리 속도를 향상시켜 전반적인 실험실 생산성을 강화합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시장 규모 | 73억 달러 |

| 예측 금액 | 166억 달러 |

| CAGR | 8.6% |

2025년 자동 시료 전처리 시스템 부문은 39.5%의 시장 점유율을 차지했습니다. 더 빠른 검사 결과 제공에 대한 수요는 복잡하고 대량 검사가 이루어지는 환경을 다루는 실험실 전반에서 도입을 지속적으로 주도하고 있습니다. 자동화 시스템은 표준화되고 프로그래밍 가능한 워크플로우를 통해 필수적인 전처리 작업을 수행함으로써 복잡한 전분석 절차를 간소화합니다. 수동 처리를 최소화하고 인적 오류 위험을 줄임으로써, 이러한 플랫폼은 일관성과 운영 정밀도를 향상시킵니다. 정교한 검사 프로토콜을 관리하는 실험실들은 효율성, 재현성 및 품질 관리를 유지하기 위해 자동화된 시료 전처리 기술에 점점 더 의존하고 있습니다.

2025년 병원 부문은 45.8%의 점유율을 차지했습니다. 병원 내 실험실의 진단 업무량이 증가함에 따라, 기관들은 효율성과 정확성을 유지하기 위해 주요 전분석 단계를 자동화하고 있습니다. 많은 입원 및 외래 환자를 처리하는 대형 의료 시설들은 최적의 검사 소요 시간을 유지하고 인력 부담을 완화하기 위해 자동화 시스템을 도입하고 있습니다. 전분석 기능을 통합하는 포괄적인 자동화 라인은 운영 표준화를 강화하고 시료 처리의 변동성을 최소화했습니다. 병원 실험실의 자동화 도입은 신속한 결과 보고, 강화된 품질 보증 조치, 그리고 수동 프로세스에 대한 의존도 감소에 기여합니다.

2025년 북미의 전분석 자동화 시장은 38.6%의 점유율을 기록했습니다. 이 지역의 성장은 진단 수요 증가와 대규모 및 중규모 의료 기관 모두의 연구, 인프라, 실험실 현대화에 대한 상당한 투자에 힘입고 있습니다. 고처리량 검사 능력, 첨단 분자 진단, AI 강화 실험실 시스템에 대한 수요가 증가함에 따라 이 지역의 선도적 위상이 더욱 공고해지고 있습니다. 워크플로우 효율성과 분석 정확도 향상을 목표로 하는 지속적인 기술 도입은 북미를 실험실 자동화 혁신의 최전선에 계속 위치시키고 있습니다.

자주 묻는 질문

목차

제1장 연구 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 실험실 자동화에 대한 수요 증가

- 임상 진단 분야의 검사량 증가

- 처리 시간 단축을 위한 임상 실험실 투자 증가

- 업계의 잠재적 위험 및 과제

- 고액의 자본 비용 및 도입 비용

- 기존 LIS 시스템과의 통합 문제

- 기회

- 신흥 시장의 자동화 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황(1차 연구에 기초)

- 북미

- 유럽

- 아시아태평양

- 기술 및 혁신 동향(1차 연구에 기초)

- 현재의 기술 동향

- 신흥 기술

- 소비자 인사이트

- 전처리 자동화 - 솔루션 아키텍처 개요

- 공급망 분석

- 투자환경

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

- 장래 시장 동향(1차 연구에 근거)

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 제품 유형별(2022-2035년)

- 자동 시료 전처리 시스템

- 자동 시료 컨베이어 시스템

- 자동 시료 선별 시스템

- 자동 시료 보관 시스템

- 기타 제품 유형

제6장 시장 추계 및 예측 : 최종 용도별(2022-2035년)

- 병원

- 임상 실험실

- 연구기관

- 기타 최종 사용자

제7장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제8장 기업 프로파일

- Abbott

- Beckman Coulter(Danaher Corporation)

- Becton, Dickinson and Company

- Copan Diagnostics

- Greiner Bio-One

- HAMILTON

- Inpeco

- QIAGEN

- Roche

- SARSTEDT

- SHIMADZU

- SIEMENS Healthineers

- Sysmex

- TECAN

- Thermo Fisher SCIENTIFIC

The Global Pre Analytical Automation Market was valued at USD 7.3 billion in 2025 and is estimated to grow at a CAGR of 8.6% to reach USD 16.6 billion by 2035.

Market growth is propelled by the steady rise in diagnostic test volumes, increasing demand for laboratory automation, and growing capital investments in advanced laboratory instrumentation aimed at accelerating result delivery. Clinical laboratories worldwide are under mounting pressure to enhance operational efficiency while maintaining accuracy and quality standards. The push for early disease detection, coupled with the rising burden of chronic and acute health conditions, has significantly increased the number of tests processed daily. To manage current and anticipated workloads, laboratories are accelerating digital transformation initiatives and implementing interconnected automation platforms within their operational frameworks. Modern pre-analytical automation systems streamline sample handling processes, improve workflow continuity, and reduce manual intervention. These solutions support higher throughput capacity, optimize sample routing, prioritize urgent cases, and enhance processing speed without proportionally increasing staffing requirements, thereby strengthening overall laboratory productivity.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.3 Billion |

| Forecast Value | $16.6 Billion |

| CAGR | 8.6% |

The automated sample preparation systems segment captured a 39.5% share in 2025. The demand for faster turnaround times continues to drive adoption across laboratories handling complex and high-volume testing environments. Automated systems simplify intricate pre-analytical procedures by executing essential preparation tasks through standardized and programmable workflows. By minimizing manual handling and reducing the risk of human error, these platforms enhance consistency and operational precision. Laboratories managing sophisticated testing protocols increasingly rely on automated sample preparation technologies to maintain efficiency, reproducibility, and quality control.

The hospitals segment accounted for 45.8% share in 2025. Rising diagnostic workloads within hospital-based laboratories are prompting institutions to automate key pre-analytical stages to preserve efficiency and accuracy. Large healthcare facilities processing high inpatient and outpatient volumes are integrating automation to sustain optimal turnaround times and alleviate workforce strain. Comprehensive automation lines that unify pre-analytical functions have strengthened operational standardization and minimized variability in sample processing. Automation deployment in hospital laboratories contributes to timely reporting, reinforced quality assurance measures, and reduced reliance on manual processes.

North America Pre Analytical Automation Market held a 38.6% share in 2025. The region's growth is supported by rising diagnostic demand and substantial investments in research, infrastructure, and laboratory modernization by both large-scale and mid-sized healthcare institutions. The increasing need for high-throughput testing capabilities, advanced molecular diagnostics, and AI-enhanced laboratory systems is reinforcing regional leadership. Ongoing technological adoption aimed at improving workflow efficiency and analytical accuracy continues to position North America at the forefront of laboratory automation innovation.

Key companies operating in the Global Pre Analytical Automation Market include Roche, Beckman Coulter (Danaher Corporation), Abbott, SIEMENS Healthineers, Thermo Fisher SCIENTIFIC, Becton Dickinson and Company, QIAGEN, Sysmex, HAMILTON, TECAN, SHIMADZU, SARSTEDT, Inpeco, Copan Diagnostics, and Greiner Bio-One. Companies in the Global Pre Analytical Automation Market are reinforcing their competitive positions through sustained investment in innovation, strategic collaborations, and global expansion initiatives. Market leaders are prioritizing the development of integrated and scalable automation platforms designed to accommodate rising test volumes and evolving laboratory requirements. Partnerships with healthcare institutions and diagnostic networks are enhancing system interoperability and long-term service contracts. Organizations are also incorporating artificial intelligence and advanced data analytics to optimize workflow management and predictive maintenance capabilities. Expansion into emerging healthcare markets and strengthening regional distribution networks remain key growth strategies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for laboratory automation

- 3.2.1.2 Increasing test volumes in clinical diagnostics

- 3.2.1.3 Growing investments in clinical laboratories for faster turnaround times

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital and installation costs

- 3.2.2.2 Integration challenges with existing LIS systems

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of automation in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape (Driven by Primary Research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Consumer insights

- 3.7 Pre analytical automation - Solution Architecture overview

- 3.8 Supply chain analysis

- 3.9 Investment landscape

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Automated sample preparation systems

- 5.3 Automated sample transport systems

- 5.4 Automated sample sorting systems

- 5.5 Automated sample storage systems

- 5.6 Other product types

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Clinical laboratories

- 6.4 Research institutes

- 6.5 Other end users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott

- 8.2 Beckman Coulter (Danaher Corporation)

- 8.3 Becton, Dickinson and Company

- 8.4 Copan Diagnostics

- 8.5 Greiner Bio-One

- 8.6 HAMILTON

- 8.7 Inpeco

- 8.8 QIAGEN

- 8.9 Roche

- 8.10 SARSTEDT

- 8.11 SHIMADZU

- 8.12 SIEMENS Healthineers

- 8.13 Sysmex

- 8.14 TECAN

- 8.15 Thermo Fisher SCIENTIFIC