|

시장보고서

상품코드

1982294

고정형 연료전지 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Stationary Fuel Cell Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

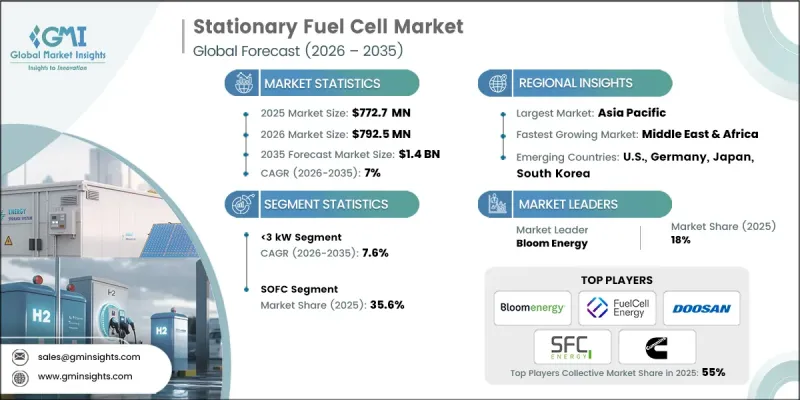

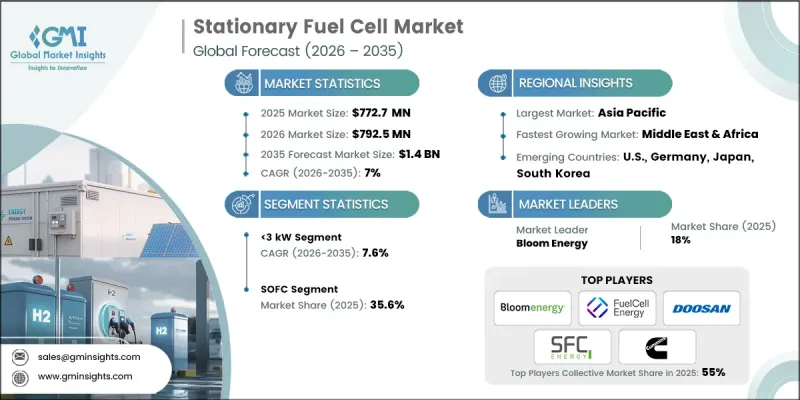

세계의 고정형 연료전지 시장은 2025년 7억 7,270만 달러로 평가되었고, CAGR은 7%를 나타낼 것으로 보이며, 2035년까지 14억 달러에 이를 것으로 추정됩니다.

시장 성장은 수소 인프라에 대한 투자 가속화, 복원력 있는 분산형 전력 시스템에 대한 수요 증가, 그리고 세계적인 탈탄소화 지원 정책에 힘입어 이루어지고 있습니다. 고정형 연료전지는 주거, 상업 및 산업 분야 전반에 걸쳐 깨끗하고 신뢰할 수 있으며 고효율적인 현장 발전의 핵심 기술로 부상하고 있습니다. 이러한 시스템은 전기화학적 과정을 통해 수소 또는 수소 함유 연료를 전기와 열로 변환하며, 기존의 화석 연료 기반 발전기에 비해 배출량을 현저히 낮춥니다. 전력망 신뢰성에 대한 우려 증가, 전기 요금 상승, 그리고 더욱 엄격해진 탄소 감축 목표는 전력 회사, 기업 및 가정이 분산형 에너지 솔루션으로 전환하도록 촉진하고 있습니다. 스택 내구성 향상, 효율 개선, 모듈식 시스템 설계, 비용 최적화 등의 기술 발전은 시장 도입을 더욱 가속화하고 있습니다. 또한, 유리한 정부 인센티브, 청정 수소 포트폴리오 기준, 재생 에너지 통합 이니셔티브는 선진국과 신흥 경제국 전반에 걸쳐 도입을 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시장 규모 | 7억 7,270만 달러 |

| 예측 금액 | 14억 달러 |

| CAGR | 7% |

PEMFC(양자 교환막 연료전지) 부문은 높은 전력 밀도, 낮은 작동 온도, 신속한 시동 능력에 힘입어 2035년까지 연평균 성장률(CAGR) 7%로 성장할 것으로 예상됩니다. PEMFC 시스템은 일반적으로 100°C 미만의 온도에서 작동하므로 응답 시간이 더 빠르며, 주거용, 상업용 및 소규모 분산형 전력 용도에 매우 적합합니다. 소형한 설계, 모듈식 구성, 그리고 수소를 주 연료원으로 사용할 수 있는 호환성 덕분에 PEMFC는 분산형 에너지 생산 및 백업 전력 시스템을 위한 이상적인 솔루션으로 자리매김하고 있습니다.

3kW 부문은 2025년 시장 점유율 35.5%를 차지했으며, 2035년까지 연평균 성장률(CAGR) 7.6%로 성장할 것으로 전망됩니다. 소규모 전력 솔루션에 대한 수요 증가로 인해, 특히 주거용 및 휴대용 백업 전원 용도에서 3kW 미만 연료전지의 채택이 활발히 이루어지고 있습니다. 주택 소유자들은 에너지 자립성, 지속 가능성, 신뢰성을 제공하는 시스템을 찾고 있으며, 이에 따라 기업들은 소형화되고 효율적인 솔루션 개발에 주력하고 있습니다. 이러한 연료전지는 작은 설치 공간, 낮은 작동 소음, 태양광 발전 시스템과의 원활한 통합 덕분에 특히 매력적이며, 분산형 발전에 이상적입니다. 또한 정전 시 신뢰할 수 있는 에너지원을 제공하여 가정이나 소규모 기업의 필수적인 전력 수요를 지원합니다.

아시아태평양의 고정형 연료전지 시장은 2035년까지 11억 달러 규모에 달할 것으로 예상됩니다. 이 지역의 선도적 위상은 강력한 정책 지원, 대규모 수소 로드맵, 그리고 일본과 한국의 조기 상용화 노력에 기인합니다. 청정 수소 촉진에 대한 정부 정책, 스마트 그리드 인프라 확장, 재생에너지 통합에 대한 투자가 이 지역의 경쟁 우위를 강화하고 있습니다. 또한 급속한 산업화, 증가하는 전력 수요, 전력망 불안정성에 대한 취약성 증대는 아시아태평양 전역에서 분산형 발전 도입을 가속화하고 있습니다. 북미와 유럽 역시 수소 자금 지원 프로그램, 탈탄소화 목표, 데이터센터, 병원, 통신 시설과 같은 핵심 인프라에서 디젤 백업 시스템의 점진적인 대체에 힘입어 꾸준한 도입이 이어지고 있습니다.

자주 묻는 질문

목차

제1장 연구 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계의 생태계

- 원재료 가용성 및 조달 분석

- 생산 능력 평가

- 공급망의 탄력성과 위험요인

- 유통 네트워크 분석

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- 비용 구조 분석

- 가격 동향 분석

- 용량별

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- PESTEL 분석

- 새로운 기회와 동향

- 디지털화와 IoT의 통합

- 신흥 시장 진출

- 투자 분석 및 미래 전망

제4장 경쟁 구도

- 소개

- 지역별 기업의 시장 점유율

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 전략적 대시보드

- 전략적 노력

- 경쟁 벤치마킹

- 혁신 및 기술 동향

제5장 시장 규모 및 예측 : 기술별(2022-2035년)

- PEMFC

- SOFC

- PAFC

- MCFC

- DMFC

- 기타

제6장 시장 규모 및 예측 : 용량별(2022-2035년)

- 3kW 미만

- 3-10kW

- 10-50kW

- >50-200kW

- 200-500kW

- 500kW 초과-1MW

- 1MW 이상

제7장 시장 규모 및 예측 : 최종 용도별(2022-2035년)

- 주택용

- 상업용

- 산업 및 유틸리티

- 데이터센터

- 반도체

- 마이크로그리드 및 분산형 에너지 시스템(DES)

- 물류 창고

- 공항

- 병원

- 통신

- 운송

- 기타

제8장 시장 규모 및 예측 : 용도별(2022-2035년)

- 주전원

- 백업/긴급용

- CHP

- 원격/오프 그리드

- 기타

제9장 시장 규모 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 오스트리아

- 아시아태평양

- 일본

- 한국

- 중국

- 인도

- 필리핀

- 베트남

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 라틴아메리카

- 브라질

- 페루

- 멕시코

제10장 기업 프로파일

- AFC Energy

- Aris Renewable Energy

- Ballard Power Systems

- Bloom Energy

- Ceres Power Holding

- Cummins

- Denso Corporation

- Doosan Fuel Cell

- FuelCell Energy

- Fuji Electric

- GenCell

- Honda Motor

- Horizon Fuel Cell Technologies

- Mitsubishi Heavy Industries

- Nuvera Fuel Cells

- Panasonic Holding Corporation

- Plug Power

- Poscoenergy

- SFC Energy

- Siemens Energy

- Toshiba Corporation

The Global Stationary Fuel Cell Market was valued at USD 772.7 million in 2025 and is estimated to grow at a CAGR of 7% to reach USD 1.4 billion by 2035.

Market growth is driven by accelerating investments in hydrogen infrastructure, increasing demand for resilient distributed power systems, and supportive decarbonization policies worldwide. Stationary fuel cells are emerging as a cornerstone technology for clean, reliable, and high-efficiency onsite power generation across residential, commercial, and industrial applications. These systems convert hydrogen or hydrogen-rich fuels into electricity and heat through electrochemical processes, offering significantly lower emissions compared to conventional fossil-fuel-based generators. Growing concerns over grid reliability, rising electricity prices, and stricter carbon reduction targets are pushing utilities, enterprises, and households toward decentralized energy solutions. Technological advancements in stack durability, efficiency improvements, modular system designs, and cost optimization are further strengthening market adoption. In addition, favorable government incentives, clean hydrogen portfolio standards, and renewable energy integration initiatives are accelerating deployments across developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $772.7 Million |

| Forecast Value | $1.4 Billion |

| CAGR | 7% |

The PEMFC (Proton Exchange Membrane Fuel Cell) segment is anticipated to grow at a CAGR of 7% through 2035, driven by its high-power density, low operating temperature, and rapid start-up capabilities. PEMFC systems typically operate at temperatures below 100°C, enabling faster response times and making them highly suitable for residential, commercial, and small-scale distributed power applications. Their compact design, modular configuration, and compatibility with hydrogen as a primary fuel source position them as an ideal solution for decentralized energy generation and backup power systems.

The 3 kW segment accounted for 35.5% share in 2025 and is projected to grow at a CAGR of 7.6% through 2035. The increasing demand for small-scale power solutions is driving strong adoption of fuel cells under 3 kW, especially for residential use and portable backup power applications. Homeowners are seeking systems that offer energy independence, sustainability, and reliability, prompting businesses to focus on compact and efficient solutions. These fuel cells are particularly appealing due to their small footprint, low operational noise, and seamless integration with solar photovoltaic systems, making them ideal for decentralized power generation. Additionally, they provide a dependable energy source during outages, supporting critical household or small business needs.

Asia Pacific Stationary Fuel Cell Market is expected to reach USD 1.1 billion by 2035. The region's leadership is attributed to strong policy support, large-scale hydrogen roadmaps, and early commercialization efforts in Japan and South Korea. Government mandates promoting clean hydrogen, expansion of smart grid infrastructure, and investments in renewable integration are reinforcing the region's competitive advantage. In addition, rapid industrialization, rising electricity demand, and increasing vulnerability to grid instability are accelerating distributed generation adoption across Asia Pacific. North America and Europe also continue to witness steady deployment, supported by hydrogen funding programs, decarbonization targets, and increasing replacement of diesel backup systems in critical infrastructure such as data centers, hospitals, and telecommunications facilities.

Key players operating in the Global Stationary Fuel Cell Market include Ballard Power Systems, Bloom Energy, Cummins Inc., DENSO Corporation, FuelCell Energy, Plug Power, Toshiba Corporation, SFC Energy AG, Fuji Electric Co., Ltd., and POSCO Energy. Companies in the Stationary Fuel Cell Market are strengthening their foothold through strategic partnerships, product innovation, and hydrogen ecosystem development. Leading players are investing in advanced solid oxide and proton exchange membrane technologies to enhance efficiency, durability, and scalability. Many firms are entering long-term supply agreements and power purchase contracts to secure recurring revenue streams. Expansion into green hydrogen production and electrolyzer integration is enabling vertically integrated solutions. Strategic collaborations with utilities, industrial operators, and government bodies are accelerating project deployments. Companies are also focusing on modular designs that allow flexible capacity expansion, improving cost competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.3.1 Key trends for market estimates

- 1.3.1.1 Quantified market impact analysis

- 1.3.1.2 Mathematical impact of growth parameters on forecast

- 1.3.2 Scenario analysis framework

- 1.3.1 Key trends for market estimates

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360-degree synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Technology trends

- 2.4 Capacity trends

- 2.5 End Use trends

- 2.6 Application trends

- 2.7 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Cost structure analysis

- 3.6 Price trend analysis

- 3.6.1 By Capacity

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Legal factors

- 3.8.6 Environmental factors

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & MW)

- 5.1 Key trends

- 5.2 PEMFC

- 5.3 SOFC

- 5.4 PAFC

- 5.5 MCFC

- 5.6 DMFC

- 5.7 Others

Chapter 6 Market Size and Forecast, By Capacity, 2022 - 2035 (USD Million & MW)

- 6.1 Key trends

- 6.2 < 3 kW

- 6.3 3 kW - 10 kW

- 6.4 10 kW - 50 kW

- 6.5 > 50 kW-200 KW

- 6.6 >200-500 KW

- 6.7 >500 kW - 1 MW

- 6.8 >1 MW

Chapter 7 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million & MW)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Industry/Utility

- 7.5 Data Centers

- 7.6 Semiconductors

- 7.7 Microgrid & DES

- 7.8 Logistics warehouse

- 7.9 Airports

- 7.10 Hospitals

- 7.11 Telecommunication

- 7.12 Transport

- 7.13 Others

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & MW)

- 8.1 Key trends

- 8.2 Prime Power

- 8.3 Backup/emergency

- 8.4 CHP

- 8.5 Remote/off grid

- 8.6 Others

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MW)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Austria

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 South Korea

- 9.4.3 China

- 9.4.4 India

- 9.4.5 Philippines

- 9.4.6 Vietnam

- 9.5 Middle East & Africa

- 9.5.1 South Africa

- 9.5.2 Saudi Arabia

- 9.5.3 UAE

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Peru

- 9.6.3 Mexico

Chapter 10 Company Profiles

- 10.1 AFC Energy

- 10.2 Aris Renewable Energy

- 10.3 Ballard Power Systems

- 10.4 Bloom Energy

- 10.5 Ceres Power Holding

- 10.6 Cummins

- 10.7 Denso Corporation

- 10.8 Doosan Fuel Cell

- 10.9 FuelCell Energy

- 10.10 Fuji Electric

- 10.11 GenCell

- 10.12 Honda Motor

- 10.13 Horizon Fuel Cell Technologies

- 10.14 Mitsubishi Heavy Industries

- 10.15 Nuvera Fuel Cells

- 10.16 Panasonic Holding Corporation

- 10.17 Plug Power

- 10.18 Poscoenergy

- 10.19 SFC Energy

- 10.20 Siemens Energy

- 10.21 Toshiba Corporation