|

시장보고서

상품코드

1982297

정맥내 면역글로불린 시장의 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Intravenous Immunoglobulin (IVIg) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

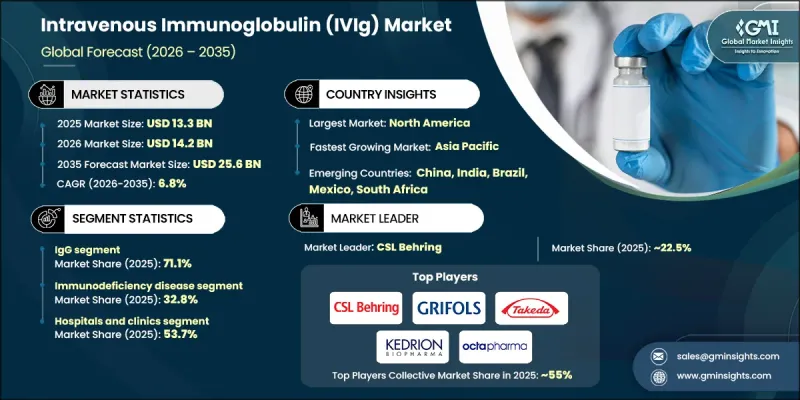

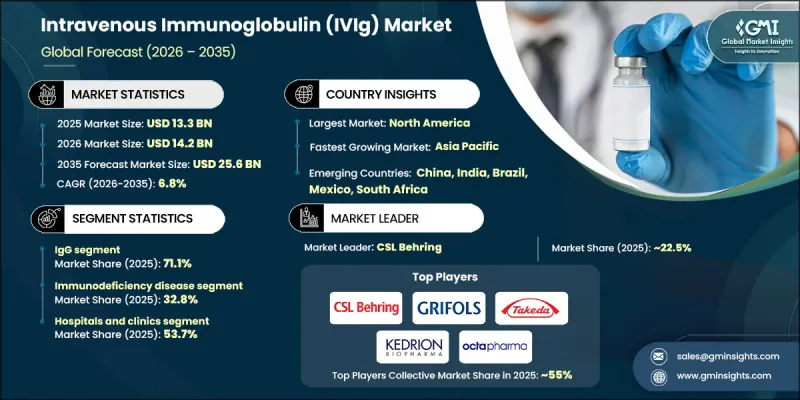

세계의 정맥내 면역글로불린(IVIg) 시장은 2025년에 133억 달러로 평가되었고 CAGR은 6.8%를 나타낼 것으로 보이며, 2035년까지 256억 달러에 이를 것으로 추정됩니다.

세계적으로 1차 및 2차 면역결핍 장애의 발병률이 증가함에 따라 시장이 성장하고 있습니다. IVIg 제품은 혼합 인간 혈장에서 추출한 무균 농축 항체 제제로, 수동 면역을 제공하기 위해 정맥 주입을 통해 투여됩니다. 이 제품은 유해한 병원체를 무력화하고 면역 반응을 조절하는 기성 항체를 공급함으로써 면역 체계를 지원합니다. IVIg의 치료적 적용 범위는 1차 면역결핍증을 넘어, 만성 염증성 탈수초성 다발신경병증, 길랭-바레 증후군, 중증근무력증과 같은 자가면역 및 신경계 질환으로 점차 확대되고 있습니다. 세계적인 수요를 충족하기 위해 주요 제조사들은 혈장 채취 센터를 빠르게 확장하고, 첨단 혈장 분리 장비에 투자하며, 지역별 혈장 조달 전략을 채택하고 있습니다. 임상 적용이 증가하고 공급망에 대한 꾸준한 투자가 더해지면서 정맥 내 면역글로불린(IVIg) 시장은 견고한 성장 궤도를 그려가고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시장 규모 | 133억 달러 |

| 예측 금액 | 256억 달러 |

| CAGR | 6.8% |

IgG 부문은 광범위한 임상적 수용과 면역 방어의 핵심적인 역할에 힘입어 2025년 71.1%의 점유율을 차지했습니다. IgG는 혈액 내 가장 널리 분포된 면역글로불린으로, 1차 및 2차 면역결핍증 치료에 선호되는 선택지입니다. 이에 대한 수요는 신경학, 혈액학, 내과를 포함한 다양한 전문 분야에 걸쳐 있으며, 확립된 규제 및 제조 기준에 의해 뒷받침되고 있습니다.

면역결핍 질환 부문은 2025년 32.8%의 점유율을 기록했으며, 2026년부터 2035년까지 연평균 성장률(CAGR) 6.9%로 성장할 것으로 예상됩니다. 이 부문은 원발성 면역결핍, 2차성 면역결핍, 저감마글로불린혈증 및 특정 항체 결핍을 포괄합니다. 평생 지속되고 만성적인 특성을 지닌 이러한 질환들은 빈번한 IVIg 주입을 필요로 하여 지속적인 시장 수요를 보장합니다.

북미의 정맥내 면역글로불린(IVIg) 시장은 선진 의료 인프라, 자가면역 및 면역결핍 질환의 높은 유병률, 견고한 보험 급여 제도, 확립된 혈장 수집 네트워크에 힘입어 2025년 52.5%의 점유율을 기록했습니다. 주요 제약사의 진출, 지속적인 임상 연구, 혁신적인 치료 프로토콜의 조기 도입은 이 지역의 시장 성숙도를 더욱 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 면역 결핍 질환의 유병률 증가

- 고령 인구 증가

- 혈장 채취, 분획 및 정제 기술의 발전

- 신경계 및 자가면역 질환에서 IVIg의 임상적 적용 증가

- 면역글로불린에 대한 의료비 지출 증가

- 업계의 잠재적 위험 및 과제

- IVIg 치료의 높은 비용

- 잠재적인 부작용 및 알레르기 반응

- 시장 기회

- 재조합 면역글로불린 개발

- 신흥국 수요 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술적 진보

- 현재의 기술 동향

- 신흥 기술

- 상환 상황

- 장래 시장 동향

- 파이프라인 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 기업의 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 공동 사업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 제품 유형별(2022-2035년)

- IgG

- IgA

- IgM

- IgD

- IgE

제6장 시장 추계 및 예측 : 용도별(2022-2035년)

- 면역 결핍 질환

- 원발성 면역결핍

- 2차성 면역 결핍증

- 저감마글로불린혈증

- 특이적 항체 결핍증

- 만성 염증성 탈수초성 다발신경병증

- 중증근무력증

- 다소성 운동신경장애

- 특발성 혈소판 감소성 자반병(ITP)

- 염증성 미오파티

- 길랭-바레 증후군

- 기타 용도

제7장 시장 추계 및 예측 : 최종 용도별(2022-2035년)

- 병원 및 진료소

- 외래수술센터(ASC)

- 재택치료 시설

- 기타 최종 사용자

제8장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 일본

- 중국

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- ADMA Biologics

- Baxter International

- Biotest

- CSL Behring

- China Biologics Products

- Grifols SA

- Intas Pharmaceuticals

- Kedrion Biopharma

- LFB Biotechnologies

- Omrix Biopharmaceuticals(Johnson & Johnson)

- Octapharma AG

- Pfizer

- Shanghai RAAS Blood Products

- Takeda Pharmaceutical Company

The Global Intravenous Immunoglobulin (IVIg) Market was valued at USD 13.3 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 25.6 billion by 2035.

The market is propelled by the rising incidence of both primary and secondary immunodeficiency disorders worldwide. IVIg products are sterile, concentrated antibody formulations derived from pooled human plasma, administered via intravenous infusion to provide passive immunity. They support the immune system by supplying ready-made antibodies that neutralize harmful pathogens and regulate immune responses. The therapeutic applications of IVIg have expanded beyond primary immunodeficiencies, increasingly addressing autoimmune and neurological disorders such as chronic inflammatory demyelinating polyneuropathy, Guillain-Barre syndrome, and myasthenia gravis. To meet global demand, leading manufacturers are rapidly expanding plasma collection centers, investing in advanced plasmapheresis equipment, and adopting regional plasma sourcing strategies. Increasing clinical adoption, combined with steady supply chain investments, is shaping a robust growth trajectory for the Intravenous Immunoglobulin (IVIg) Market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.3 Billion |

| Forecast Value | $25.6 Billion |

| CAGR | 6.8% |

The IgG segment held a 71.1% share in 2025, driven by its broad clinical acceptance and key role in immune defense. IgG is the most prevalent immunoglobulin in circulation, making it the preferred choice for treating both primary and secondary immunodeficiencies. Its demand spans multiple specialties, including neurology, hematology, and internal medicine, reinforced by well-established regulatory and manufacturing standards.

The immunodeficiency disease segment accounted for 32.8% share in 2025 and is expected to grow at a CAGR of 6.9% during 2026-2035. This segment encompasses primary immunodeficiencies, secondary immunodeficiencies, hypogammaglobulinemia, and specific antibody deficiencies. Lifelong and chronic in nature, these conditions require frequent IVIg infusions, ensuring sustained market demand.

North America Intravenous Immunoglobulin (IVIg) Market held 52.5% share in 2025, supported by advanced healthcare infrastructure, high prevalence of autoimmune and immunodeficiency disorders, robust reimbursement systems, and an established plasma collection network. The presence of leading pharmaceutical companies, ongoing clinical research, and early adoption of innovative treatment protocols further strengthen market maturity in the region.

Key players in the Global Intravenous Immunoglobulin (IVIg) Market include Baxter International, CSL Behring, Octapharma AG, Grifols SA, Pfizer, Takeda Pharmaceutical Company, ADMA Biologics, Biotest, China Biologics Products, Omrix Biopharmaceuticals (Johnson & Johnson), LFB Biotechnologies, Kedrion Biopharma, Intas Pharmaceuticals, and Shanghai RAAS Blood Products. To strengthen the Intravenous Immunoglobulin (IVIg) Market position, companies are focusing on expanding plasma collection and fractionation capacities, investing in state-of-the-art plasmapheresis equipment, and developing regional sourcing strategies to ensure a stable supply of raw materials. They are also diversifying their product portfolios to target autoimmune and neurological disorders, while optimizing manufacturing processes to reduce costs and enhance efficiency. Strategic partnerships with hospitals, specialty clinics, and healthcare networks expand distribution channels.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of immunodeficiency disorders

- 3.2.1.2 Increasing geriatric population

- 3.2.1.3 Growing advances in plasma collection, fractionation, and purification technologies

- 3.2.1.4 Rising clinical applications of IVIg in neurological and autoimmune disorders

- 3.2.1.5 Increasing healthcare expenditure for immunoglobulins

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of IVIg therapy

- 3.2.2.2 Potential adverse effects and allergic reactions

- 3.2.3 Market opportunities

- 3.2.3.1 Development of recombinant immunoglobulins

- 3.2.3.2 Rising demand in emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Future market trends

- 3.8 Pipeline analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 IgG

- 5.3 IgA

- 5.4 IgM

- 5.5 IgD

- 5.6 IgE

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Immunodeficiency diseases

- 6.2.1 Primary immunodeficiencies

- 6.2.2 Secondary immunodeficiencies

- 6.2.3 Hypogammaglobulinemia

- 6.2.4 Specific antibody deficiency

- 6.3 Chronic Inflammatory demyelinating polyneuropathy (CIDP)

- 6.4 Myasthenia gravis

- 6.5 Multifocal motor neuropathy

- 6.6 Idiopathic thrombocytopenic purpura (ITP)

- 6.7 Inflammatory myopathies

- 6.8 Guillain-Barre syndrome

- 6.9 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Ambulatory surgical centers

- 7.4 Homecare settings

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ADMA Biologics

- 9.2 Baxter International

- 9.3 Biotest

- 9.4 CSL Behring

- 9.5 China Biologics Products

- 9.6 Grifols SA

- 9.7 Intas Pharmaceuticals

- 9.8 Kedrion Biopharma

- 9.9 LFB Biotechnologies

- 9.10 Omrix Biopharmaceuticals (Johnson & Johnson)

- 9.11 Octapharma AG

- 9.12 Pfizer

- 9.13 Shanghai RAAS Blood Products

- 9.14 Takeda Pharmaceutical Company