|

시장보고서

상품코드

1982299

산업용 서지 보호 기기 시장의 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Industrial Surge Protection Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

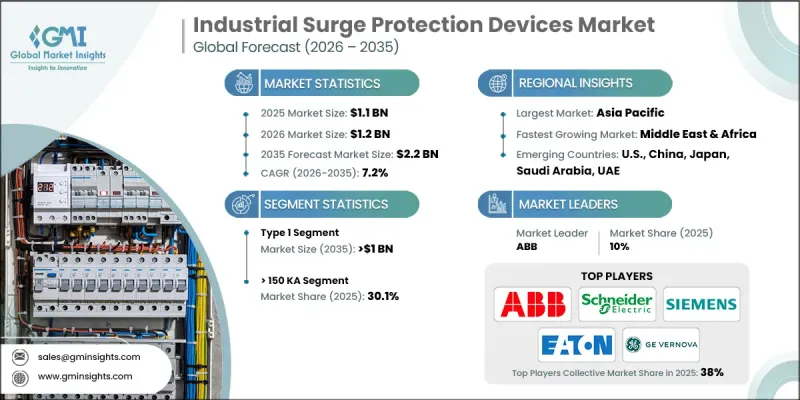

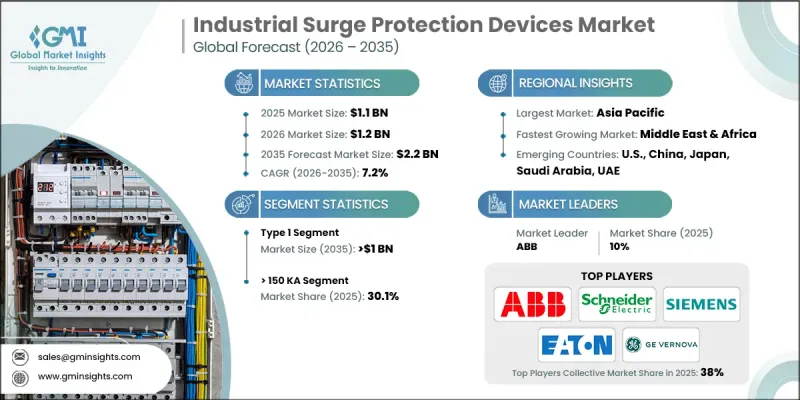

세계의 산업용 서지 보호 기기 시장은 2025년 11억 달러로 평가되었고 CAGR은 7.2%를 나타낼 것으로 보이며, 2035년까지 22억 달러에 이를 것으로 예측됩니다.

산업 전반에서 첨단 전자 시스템에 대한 의존도가 높아짐에 따라 신뢰할 수 있는 서지 보호 솔루션에 대한 수요가 크게 증가하고 있습니다. 전력망 변동 및 기상 조건으로 인한 전력 장애 발생이 증가함에 따라 다양한 산업 분야에서 해당 제품의 도입이 가속화되고 있습니다. 동시에, 더욱 엄격해진 전기 안전 규정과 IEC 및 UL 서지 보호 표준의 의무적 준수가 수요를 뒷받침하고 있습니다. 산업계가 운영을 지속적으로 디지털화하고 민감한 전기 인프라를 구축함에 따라, 전압 변동으로부터 미션 크리티컬 장비를 보호하는 것이 최우선 운영 과제가 되었습니다. 산업 시설들은 가동 중단 시간 최소화, 자산 손상 방지, 근로자 안전 확보에 더욱 중점을 두고 있습니다. 이와 더불어 전력 인프라의 현대화와 더욱 연결된 산업 생태계로의 전환이 유리한 성장 여건을 조성하고 있습니다. 또한 시장은 서지 억제 기능에 지능형 모니터링 및 광범위한 에너지 관리 기능을 결합한 첨단 통합 솔루션으로의 전환을 목격하고 있으며, 이는 산업의 장기적 전망을 더욱 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시장 규모 | 11억 달러 |

| 예측 금액 | 22억 달러 |

| CAGR | 7.2% |

산업용 서지 보호 기기는 낙뢰, 스위칭 작업, 갑작스러운 전력 변동으로 인한 과도 과전압으로부터 전기 시스템을 보호하는 데 중요한 역할을 합니다. 이러한 시스템은 과전압을 민감한 부품에서 우회시켜 장비 고장, 운영 중단 및 안전 위험의 가능성을 줄여줍니다. 전기적 신뢰성이 필수적인 산업 환경에서 서지 보호는 모터, 변압기, 자동 제어 시스템 등 고가 자산을 보존하는 데 필수적입니다. 스마트 그리드 인프라의 급속한 확장과 전기적 복원력에 대한 인식 제고는 시장 성장을 가속화할 것으로 예상됩니다. 제조사들은 운영 투명성을 높이기 위해 서지 보호 기능에 실시간 진단 및 시스템 모니터링을 통합한 다기능 기기를 점점 더 많이 제공하고 있습니다.

Type 1 산업용 서지 보호 기기 시장은 2035년까지 10억 달러에 이를 것으로 예측됩니다. 고에너지 서지로부터 중장비 산업 설비를 보호하려는 수요가 증가함에 따라 경쟁 구도가 재편되고 있습니다. 이러한 기기는 중요 인프라를 보호하고 막대한 비용이 드는 가동 중단이나 안전 문제의 발생 가능성을 줄이기 위해 서비스 입구에 널리 배치됩니다. 산업 자동화의 확대와 산업용 IoT 프레임워크의 확장은 다양한 시설 전반에 걸친 제품 보급 확대에 기여하고 있습니다.

2025년 기준 150kA 이상의 정격 용량을 가진 기기가 시장 점유율의 30.1%를 차지했다. 기업들이 심각한 전기적 장애에 대한 복원력을 최우선으로 삼으면서 고용량 서지 보호 기기가 주목받고 있습니다. 기업들은 서지 관련 손상을 예방함으로써 얻을 수 있는 경제적 이점을 점점 더 인식하고 있으며, 이는 장기적인 신뢰성과 운영 연속성을 강화하는 고정격 보호 시스템에 대한 투자를 촉진하고 있습니다.

2025년 미국의 산업용 서지 보호 기기 시장은 1억 5,780만 달러에 달했습니다. 규제 체계의 강화와 운영 안전 기준에 대한 관심 증대는 산업 확장을 뒷받침하고 있습니다. 지속적인 인프라 업그레이드, 첨단 기술의 광범위한 도입, 민감한 전자 장비의 증가된 배치는 주요 성장 동력입니다. 노후화된 전력망과 반복되는 기상 관련 정전은 산업 전반에 걸쳐 견고한 서지 보호 시스템의 필요성을 더욱 강조하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 원재료 가용성 및 조달 분석

- 제조 능력 평가

- 공급망의 탄력성과 위험요인

- 유통 네트워크 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 규제 상황

- 성장 가능성 분석

- 가격 동향 분석(달러/유닛)

- 지역별

- 용량별

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- PESTEL 분석

- 산업용 서지 보호 기기의 비용 구조 분석

- 새로운 기회와 동향

- 디지털화와 IoT의 통합

- 미개척 시장 및 용도의 성장

- 투자분석과 전망

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석 : 지역별

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획 및 자금 조달

제5장 시장 규모 및 예측 : 제품별(2022-2035년)

- 하드 와이어

- 플러그인

- 전원 코드

- 전력 제어 기기

제6장 시장 규모 및 예측 : 기술별(2022-2035년)

- Type 1

- Type 2

- Type 3

제7장 시장 규모 및 예측 : 정격전류별(2022-2035년)

- 50kA 이하

- 50-100kA

- >100-150kA

- >150kA

제8장 시장 규모 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 러시아

- 영국

- 이탈리아

- 스페인

- 네덜란드

- 오스트리아

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 뉴질랜드

- 말레이시아

- 인도네시아

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 이집트

- 남아프리카

- 나이지리아

- 쿠웨이트

- 오만

- 라틴아메리카

- 브라질

- 페루

- 아르헨티나

제9장 기업 프로파일

- ABB

- Belkin

- CAPE Electric

- CG Power and Industrial Solutions

- CITEL

- DEHN

- Eaton

- Emerson Electric

- GE Vernova

- Havells

- Hubbell

- Legrand

- Leviton Manufacturing

- Maxivolt

- Mersen

- nVent

- Phoenix Contact

- Prosurge

- Raycap

- Rockwell Automation

- Saltek

- Schneider Electric

- Siemens

- Socomec

- Weidmuller Electronics

The Global Industrial Surge Protection Devices Market was valued at USD 1.1 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 2.2 billion by 2035.

Growing dependence on advanced electronic systems across industrial environments is significantly increasing the need for reliable surge protection solutions. Rising incidents of grid fluctuations and weather-driven power disturbances are accelerating product adoption across multiple sectors. At the same time, stricter electrical safety mandates and compulsory compliance with IEC and UL surge protection standards are reinforcing demand. As industries continue to digitize operations and deploy sensitive electrical infrastructure, safeguarding mission-critical equipment from voltage irregularities has become a top operational priority. Industrial facilities are placing greater emphasis on minimizing downtime, preventing asset damage, and ensuring workforce safety. In parallel, modernization of power infrastructure and the transition toward more connected industrial ecosystems are creating favorable growth conditions. The market is also witnessing a shift toward advanced, integrated solutions that combine surge suppression with intelligent monitoring and broader energy management capabilities, further strengthening long-term industry prospects.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.1 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 7.2% |

Industrial surge protection devices play a crucial role in shielding electrical systems from transient overvoltage caused by lightning events, switching operations, and sudden power fluctuations. These systems function by diverting excess voltage away from sensitive components, reducing the risk of equipment failure, operational disruption, and safety hazards. In industrial settings where electrical reliability is essential, surge protection is vital to preserving high-value assets, including motors, transformers, and automated control systems. The rapid expansion of smart grid infrastructure and heightened awareness of electrical resilience are expected to accelerate market growth. Manufacturers are increasingly offering multifunctional devices that integrate surge protection with real-time diagnostics and system monitoring to enhance operational transparency.

The Type 1 industrial surge protection devices segment is forecast to reach USD 1 billion by 2035. Increasing demand to protect heavy-duty industrial equipment from high-energy surges is reshaping the competitive landscape. These devices are widely deployed at service entrances to secure critical infrastructure and reduce the likelihood of costly shutdowns or safety concerns. Growing industrial automation and the expansion of industrial IoT frameworks are contributing to stronger product penetration across diverse facilities.

The devices rated above 150 kA accounted for 30.1% share in 2025. High-capacity surge protection units are gaining traction as organizations prioritize resilience against severe electrical disturbances. Businesses are increasingly recognizing the financial advantages of preventing surge-related damage, prompting investment in higher-rated protection systems that enhance long-term reliability and operational continuity.

U.S. Industrial Surge Protection Devices Market reached USD 157.8 million in 2025. Strengthening regulatory frameworks and heightened focus on operational safety standards are reinforcing industry expansion. Ongoing infrastructure upgrades, wider adoption of advanced technologies, and increased deployment of sensitive electronic equipment are major growth drivers. Aging electrical networks and recurring weather-related power disruptions further underscore the necessity of robust surge protection systems across industrial applications.

Prominent companies operating in the Global Industrial Surge Protection Devices Market include Schneider Electric, ABB, Siemens, Eaton, Legrand, Phoenix Contact, Emerson Electric, Rockwell Automation, GE Vernova, Hubbell, Belkin, Raycap, Socomec, Mersen, Havells, Weidmuller Electronics, Prosurge, DEHN, CG Power and Industrial Solutions, CAPE Electric, Saltek, nVent, Leviton Manufacturing, CITEL, and Maxivolt. Companies in the industrial surge protection devices market are reinforcing their market foothold through continuous product innovation, regulatory alignment, and strategic collaborations. Manufacturers are investing in advanced surge suppression technologies, higher discharge capacity systems, and smart monitoring features to differentiate their portfolios. Expanding global distribution networks and strengthening partnerships with industrial contractors enhance market reach and customer engagement. Many players are focusing on certification compliance and adherence to evolving electrical safety standards to build credibility and trust. Localization of production facilities and supply chain optimization helps reduce lead times and operational costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates and forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 Technology trends

- 2.1.4 Power rating trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Price trend analysis (USD/Unit)

- 3.5.1 By region

- 3.5.2 By capacity

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Cost structure analysis of industrial surge protection devices

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Growth in untapped markets & applications

- 3.10 Investment analysis & future prospects

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Million & ‘000 Units)

- 5.1 Key trends

- 5.2 Hard-wired

- 5.3 Plug-in

- 5.4 Line cord

- 5.5 Power control devices

Chapter 6 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & ‘000 Units)

- 6.1 Key trends

- 6.2 Type 1

- 6.3 Type 2

- 6.4 Type 3

Chapter 7 Market Size and Forecast, By Power Rating, 2022 - 2035 (USD Million & ‘000 Units)

- 7.1 Key trends

- 7.2 ≤ 50 kA

- 7.3 > 50 kA to 100 kA

- 7.4 > 100 kA to 150 kA

- 7.5 > 150 kA

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & ‘000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 Russia

- 8.3.4 UK

- 8.3.5 Italy

- 8.3.6 Spain

- 8.3.7 Netherlands

- 8.3.8 Austria

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Australia

- 8.4.6 New Zealand

- 8.4.7 Malaysia

- 8.4.8 Indonesia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Egypt

- 8.5.5 South Africa

- 8.5.6 Nigeria

- 8.5.7 Kuwait

- 8.5.8 Oman

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Peru

- 8.6.3 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Belkin

- 9.3 CAPE Electric

- 9.4 CG Power and Industrial Solutions

- 9.5 CITEL

- 9.6 DEHN

- 9.7 Eaton

- 9.8 Emerson Electric

- 9.9 GE Vernova

- 9.10 Havells

- 9.11 Hubbell

- 9.12 Legrand

- 9.13 Leviton Manufacturing

- 9.14 Maxivolt

- 9.15 Mersen

- 9.16 nVent

- 9.17 Phoenix Contact

- 9.18 Prosurge

- 9.19 Raycap

- 9.20 Rockwell Automation

- 9.21 Saltek

- 9.22 Schneider Electric

- 9.23 Siemens

- 9.24 Socomec

- 9.25 Weidmuller Electronics