|

시장보고서

상품코드

1982304

골프 카트 시장의 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Golf Cart Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

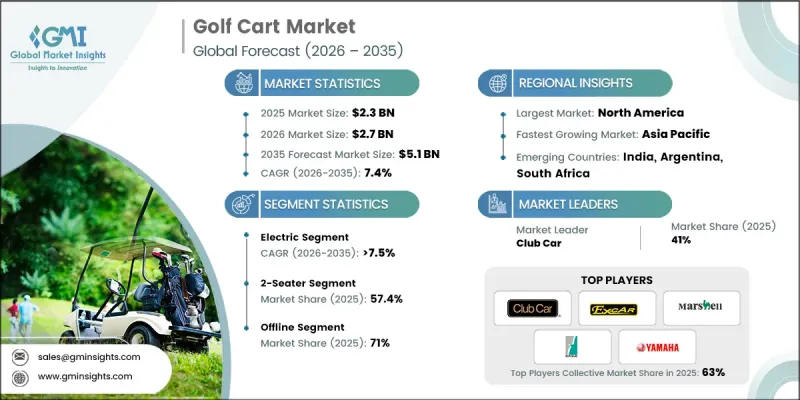

세계의 골프 카트 시장은 2025년 23억 달러로 평가되었고 CAGR은 7.4%를 나타낼 것으로 보이며, 2035년까지 51억 달러에 이를 것으로 추정됩니다.

이 시장의 성장은 게이트형 주택 단지, 은퇴자 주택 단지, 그리고 소형 저속 이동 수단을 우선시하는 계획형 스마트 타운십의 급속한 발전에 힘입고 있습니다. 골프 카트는 단거리 이동을 위한 비용 효율적이고 편리한 교통 수단으로서 통제된 주택 환경에 점차 통합되고 있습니다. 보행자 친화적인 배치와 저공해 교통 수단을 강조하는 도시 개발 전략은 이러한 도입을 더욱 가속화하고 있습니다. 그 결과, 종합 계획 단지는 전용 통로와 충전 인프라를 구축함으로써 세계적으로 꾸준한 교체 주기와 차량 확대 기회를 창출하고 있습니다. 이와 동시에 제조사들은 경쟁적 입지를 강화하기 위해 인수합병, 파트너십, 신제품 출시를 적극적으로 추진하고 있습니다. 리튬 이온 배터리 시스템 및 완전 전기화로의 지속적인 전환은 업계 지형을 재편하고 있습니다. 기존 배터리 기술에 비해 리튬 이온 솔루션은 수명 연장, 빠른 충전, 경량화, 낮은 유지보수 요구 사항을 제공하여 전반적인 소유 비용 효율성과 운영 효율성을 개선하는 동시에 장기적인 시장 지속 가능성을 강화합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시장 규모 | 23억 달러 |

| 예측 금액 | 51억 달러 |

| CAGR | 7.4% |

레저 용도를 넘어, 골프 카트는 상업 및 기관 시설 전반에 걸쳐 도입이 증가하면서 전체 잠재 시장을 확대하고 있습니다. 기업들은 골프 카트의 콤팩트한 구조, 기동성, 낮은 운영 비용 덕분에 내부 운송, 업무 이동, 경량 물류 용도로 이 차량을 활용하고 있습니다. 이러한 변화는 골프 카트를 순수한 레저용 차량에서 다양한 비즈니스 기능을 지원하는 실용적인 이동 솔루션으로 탈바꿈시키고 있습니다.

전기차 부문은 2025년 시장 점유율의 62%를 차지했으며, 2026년부터 2035년까지 연평균 성장률(CAGR) 7.5%로 성장할 것으로 전망됩니다. 무공해 이동 수단과 환경 친화적인 운송 솔루션에 대한 관심이 높아짐에 따라 전기차 도입이 가속화되고 있습니다. 전기차 모델은 배기 가스를 배출하지 않고 소음 수준을 현저히 낮추어, 지속 가능성 목표 및 환경 인증 이니셔티브와 부합합니다. 이러한 장점은 주택 및 상업 시설 전반에 걸쳐 장기적인 구매 수요를 강화하고 있습니다.

2인승 부문은 2025년 57.4%의 점유율을 기록했으며, 2026년부터 2035년까지 연평균 성장률(CAGR) 7.5%를 기록할 것으로 예상됩니다. 이 모델들은 소형한 크기와 뛰어난 기동성으로 인해 전통적인 골프 코스 운영에 매우 적합합니다. 경량 구조는 지면 충격을 줄이고 에너지 효율을 높여 대규모 차량을 관리하는 운영자에게 비용 이점을 제공합니다. 교체용 차량 및 신규 구매에 대한 지속적인 수요가 세계적으로 이 부문의 성장을 뒷받침하고 있습니다.

미국의 골프 카트 시장은 2025년에 87%의 점유율을 차지했고, 14억 달러 시장 규모를 기록했습니다. 미국은 광범위한 골프 시설 네트워크를 바탕으로 꾸준한 차량 수요를 유지하고 있습니다. 다양한 연령층의 높은 참여율은 안정적인 구매 및 장비 교체 주기를 뒷받침합니다. 전기차 및 리튬이온 배터리 모델로의 업그레이드를 포함한 지속적인 차량 현대화 노력은 해당 지역에서 활동하는 제조업체들의 장기적인 매출 성장을 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 게이트 커뮤니티 및 스마트 타운십의 확장

- 골프 관광 및 레저 활동의 성장

- 전기화 및 리튬 이온 배터리 채택

- 상업 및 기관 시설의 사용 증가

- 맞춤형 및 커넥티드카의 기능

- 업계의 잠재적 위험 및 과제

- 리튬이온 모델의 높은 초기 비용

- 저속 차량에 대한 규제 제한

- 배터리 폐기 및 환경 문제

- 대체 마이크로 모빌리티 솔루션과의 경쟁

- 시장 기회

- 아시아태평양의 관광 부문에서 확대

- 전기자동차의 성장

- 차량 대여 및 렌탈 모델

- 배터리 관리 기술의 발전

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 환경보호청(EPA)

- 미국 도로 교통 안전국(NHTSA)-FMVSS 500

- 노동안전보건국(OSHA)

- 캐나다 자동차 안전 기준(CMVSS)

- 주 수준의 도로 이용 규제

- 유럽

- EU 기계 지령

- CE 마킹의 적합성

- 저전압 지령(LVD)

- 전자기 양립성(EMC) 지령

- 각국의 도로 인증 요건

- 아시아태평양

- 중국의 EV 및 LSV에 관한 규제 프레임워크

- 인도 중앙자동차규칙(CMVR)

- 일본의 도로 운송 차량법

- ASEAN의 EV정책 조화를 위한 노력

- 호주 설계 규칙(ADR)

- 라틴아메리카

- 브라질 국가 교통 평의회(CONTRAN)의 규제

- 멕시코의 NOM 규격

- 지역별 도시 모빌리티 및 EV 인센티브 프로그램

- 중동 및 아프리카

- GCC의 차량 적합성 및 형식 인정 규제

- 남아프리카공화국 도로 교통법(NRTA)

- 관광 및 프리존의 운영 기준

- 북미

- 주요 시장 동향과 변화

- 장래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 허브

- 소비 허브

- 수입 및 수출

- 원가 내역 분석

- 특허 분석

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산의 에너지 효율

- 환경 배려형 이니셔티브

- 탄소발자국에 관한 고찰

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카(MEA)

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 연료별(2022-2035년)

- 가솔린

- 전기

- 태양광

제6장 시장 추계 및 예측 : 용도별(2022-2035년)

- 골프장

- 호텔 및 리조트

- 공항

- 주택 프로젝트

- 기타

제7장 시장 추계 및 예측 : 판매 채널별(2022-2035년)

- 온라인

- 오프라인

제8장 시장 추계 및 예측 : 좌석수별(2022-2035년)

- 2인승

- 4인승

- 6인승

- 기타

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 폴란드

- 네덜란드

- 벨기에

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 동남아시아

- ANZ

- 라틴아메리카

- 브라질

- 아르헨티나

- 멕시코

- 중동 및 아프리카(MEA)

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제10장 기업 프로파일

- 세계 기업

- Club Car

- Columbia

- Cushman

- EZ-GO

- Garia

- Polaris

- Yamaha

- 지역 기업

- Advanced EV

- Bintelli

- Evolution EV

- Melex

- Pilotcar

- Star EV

- Tomberlin

- 신흥 기업

- Eco Planeta

- Guangdong Lvtong

- HDK

- Jinghang Sightseeing

- Langqing

- Marshell

- Suzhou Eagle

The Global Golf Cart Market was valued at USD 2.3 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 5.1 billion by 2035.

Market growth is supported by the rapid development of gated residential communities, retirement living projects, and planned smart townships that prioritize compact and low-speed mobility. Golf carts are increasingly integrated into controlled residential environments as a cost-effective and convenient transportation solution for short-distance travel. Urban development strategies that emphasize pedestrian-friendly layouts and low-emission transit options are further accelerating adoption. As a result, master-planned communities are incorporating dedicated pathways and charging infrastructure, creating steady replacement cycles and fleet expansion opportunities worldwide. In parallel, manufacturers are actively pursuing mergers, acquisitions, partnerships, and new product introductions to strengthen their competitive positioning. The ongoing transition toward lithium-ion battery systems and full electrification is reshaping the industry landscape. Compared to conventional battery technologies, lithium-ion solutions offer extended lifespan, faster charging, reduced weight, and lower maintenance requirements, improving overall ownership economics and operational efficiency while reinforcing long-term market sustainability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.3 Billion |

| Forecast Value | $5.1 Billion |

| CAGR | 7.4% |

Beyond recreational applications, golf carts are witnessing rising deployment across commercial and institutional facilities, expanding the overall addressable market. Organizations are utilizing these vehicles for internal transportation, operational mobility, and light-duty logistics due to their compact structure, maneuverability, and low operating expenses. This shift is transforming golf carts from purely leisure-oriented vehicles into practical mobility solutions supporting diverse business functions.

The electric segment accounted for 62% share in 2025 and is anticipated to grow at a CAGR of 7.5% from 2026 to 2035. Growing emphasis on zero-emission mobility and environmentally responsible transportation solutions is driving adoption. Electric models eliminate tailpipe emissions and significantly reduce noise levels, aligning with sustainability objectives and environmental certification initiatives. These advantages are strengthening long-term procurement demand across residential and commercial settings.

The 2-seater segment held 57.4% share in 2025 and is expected to register a CAGR of 7.5% during 2026-2035. Their compact dimensions and ease of handling make them highly suitable for traditional golf course operations. Lightweight construction reduces surface impact and enhances energy efficiency, delivering cost advantages for operators managing large fleets. Continuous demand for replacement units and new purchases is supporting segment growth globally.

U.S. Golf Cart Market held an 87% share in 2025, generating USD 1.4 billion. The country benefits from an extensive network of golf facilities, sustaining consistent fleet demand. Strong participation rates across multiple age demographics contribute to steady procurement and equipment replacement cycles. Ongoing fleet modernization initiatives, including upgrades to electric and lithium-ion-powered models, are reinforcing long-term revenue growth for manufacturers operating in the region.

Key companies operating in the Global Golf Cart Market include Club Car, Yamaha, E-Z-GO, Cushman, Columbia, Marshell Green, Suzhou Eagle, Dongguan Excar, LANGQING, and Aoxiang. Companies in the Global Golf Cart Market are reinforcing their competitive strength through product innovation, battery technology advancements, and strategic partnerships. Manufacturers are investing in lithium-ion platforms, smart connectivity features, and improved vehicle design to enhance performance and user experience. Strategic alliances with residential developers and commercial operators are expanding distribution channels and long-term supply agreements. Many firms are introducing customized configurations tailored to specific end-user requirements, improving brand differentiation and customer loyalty. Geographic expansion and localized manufacturing initiatives are also being implemented to reduce production costs and strengthen regional presence.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fuel

- 2.2.3 Application

- 2.2.4 Sales channel

- 2.2.5 Seating capacity

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of gated communities and smart townships

- 3.2.1.2 Growth in golf tourism and leisure activities

- 3.2.1.3 Electrification and lithium-ion battery adoption

- 3.2.1.4 Increasing use in commercial & institutional facilities

- 3.2.1.5 Customization and connected vehicle features

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High upfront cost of lithium-ion models

- 3.2.2.2 Regulatory restrictions on low-speed vehicles

- 3.2.2.3 Battery disposal and environmental concerns

- 3.2.2.4 Competition from alternative micro-mobility solutions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in Asia Pacific tourism sector

- 3.2.3.2 Growth of electric utility vehicles

- 3.2.3.3 Fleet leasing and rental models

- 3.2.3.4 Technological advancements in battery management

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental Protection Agency (EPA)

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA) - FMVSS 500

- 3.4.1.3 Occupational Safety and Health Administration (OSHA)

- 3.4.1.4 Canadian Motor Vehicle Safety Standards (CMVSS)

- 3.4.1.5 State-Level Road Use Regulations

- 3.4.2 Europe

- 3.4.2.1 EU Machinery Directive

- 3.4.2.2 CE Marking Compliance

- 3.4.2.3 Low Voltage Directive (LVD)

- 3.4.2.4 Electromagnetic Compatibility (EMC) Directive

- 3.4.2.5 National Road Homologation Requirements

- 3.4.3 Asia Pacific

- 3.4.3.1 Chinese EV & LSV Regulatory Framework

- 3.4.3.2 Indian Central Motor Vehicle Rules (CMVR)

- 3.4.3.3 Japanese Road Transport Vehicle Act

- 3.4.3.4 ASEAN EV Policy Harmonization Efforts

- 3.4.3.5 Australian Design Rules (ADR)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Traffic Council (CONTRAN) Regulations

- 3.4.4.2 Mexican NOM Standards

- 3.4.4.3 Regional Urban Mobility & EV Incentive Programs

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Vehicle Compliance & Type Approval Regulations

- 3.4.5.2 South African National Road Traffic Act (NRTA)

- 3.4.5.3 Tourism & Free-Zone Operational Standards

- 3.4.1 North America

- 3.5 Major market trends and disruptions

- 3.6 Future market trends

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By product

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Cost breakdown analysis

- 3.13 Patent analysis

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Fuel, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Gasoline

- 5.3 Electric

- 5.4 Solar-powered

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Golf Course

- 6.3 Hotels and Resorts

- 6.4 Airports

- 6.5 Housing Projects

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Online

- 7.3 Offline

Chapter 8 Market Estimates & Forecast, By Seating Capacity, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 2-Seater

- 8.3 4-Seater

- 8.4 6-Seater

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Poland

- 9.3.7 Netherlands

- 9.3.8 Belgium

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Southeast Asia

- 9.4.6 ANZ

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Club Car

- 10.1.2 Columbia

- 10.1.3 Cushman

- 10.1.4 E-Z-GO

- 10.1.5 Garia

- 10.1.6 Polaris

- 10.1.7 Yamaha

- 10.2 Regional Players

- 10.2.1 Advanced EV

- 10.2.2 Bintelli

- 10.2.3 Evolution EV

- 10.2.4 Melex

- 10.2.5 Pilotcar

- 10.2.6 Star EV

- 10.2.7 Tomberlin

- 10.3 Emerging Players

- 10.3.1 Eco Planeta

- 10.3.2 Guangdong Lvtong

- 10.3.3 HDK

- 10.3.4 Jinghang Sightseeing

- 10.3.5 Langqing

- 10.3.6 Marshell

- 10.3.7 Suzhou Eagle