|

시장보고서

상품코드

1982322

자동차 전기 구동계 부품 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Electric Drivetrain Components Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

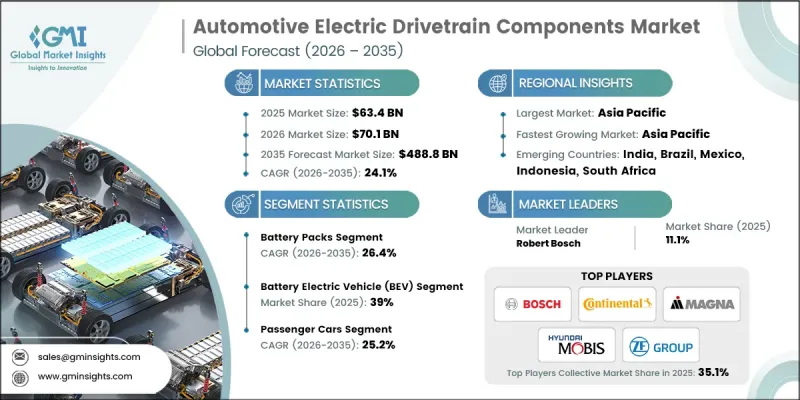

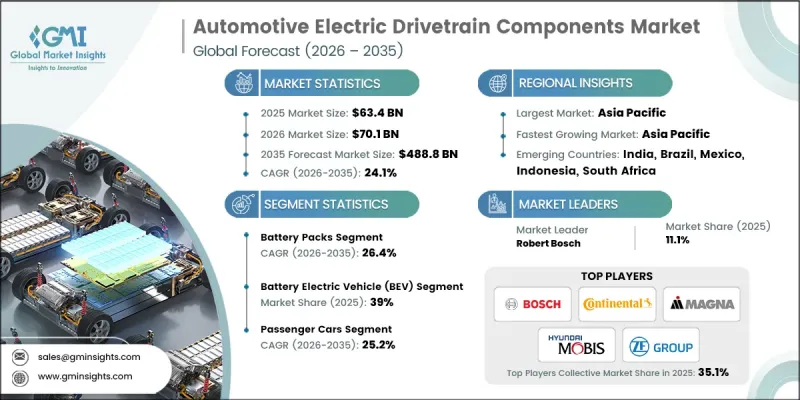

세계의 자동차 전기 구동계 부품 시장은 2025년 634억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR)은 24.1%를 나타낼 것으로 보이며, 4,888억 달러에 이를 것으로 추정됩니다.

자동차 산업 전반에 걸친 급속한 전기화는 첨단 전기 구동계 시스템에 대한 수요를 가속화하고 있습니다. 세계적으로 강화되는 배출 규제로 인해 자동차 제조사들은 전기차 플랫폼으로의 전환을 더욱 빠르게 추진하고 있습니다. 이러한 규제 압력으로 인해 전기 구동 장치, 인버터, 전력 전자 장치 및 통합 전기 추진 모듈의 생산이 크게 증가하고 있습니다. 리튬이온 배터리 제조 비용의 지속적인 감소와 생산 효율성 향상은 차량 가격 구조를 재편하여 전기차의 경쟁력을 더욱 높이고 있습니다. 배터리 비용이 하락함에 따라 제조사들은 증가하는 글로벌 수요를 충족하기 위해 경량 전기 모터와 고효율 인버터 시스템의 생산을 확대하고 있습니다. 구동계 기술의 발전은 또한 차량 주행 거리, 충전 호환성 및 전반적인 시스템 성능을 향상시켜 전기차의 광범위한 보급을 뒷받침하고 있습니다. 자동차 제조사들은 실시간 모니터링과 에너지 관리를 최적화하기 위해 지능형 e-액슬, 커넥티드 제어 모듈 및 첨단 진단 기능을 전기 구동계 아키텍처에 통합하고 있습니다. 규제 의무, 배터리 비용 하락, 성능 중심의 혁신이 결합되면서 전기 구동계 부품은 글로벌 자동차 산업 내 핵심 성장 동력으로 자리매김하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시장 규모 | 634억 달러 |

| 예측 금액 | 4,888억 달러 |

| CAGR | 24.1% |

배터리 팩 부문은 2025년 26%의 점유율을 기록했으며, 2026년부터 2035년까지 연평균 성장률(CAGR) 26.4%로 성장할 것으로 예상됩니다. 에너지 밀도, 배터리 관리 시스템(BMS), 차세대 전지 화학 성분 분야의 지속적인 발전은 주행 거리와 운행 안전성을 향상시키고 있습니다. 업계의 관심은 여전히 더 빠른 충전 능력, 내구성 강화, 비용 최적화에 집중되어 있습니다. 신흥 배터리 기술과 진화하는 재료 구성은 예측 기간 동안 성능 기준과 제조 확장성을 더욱 강화할 것으로 예상됩니다.

승용차 부문은 2025년에 65%의 점유율을 차지하고 2026년부터 2035년에 걸쳐 CAGR 25.2%를 나타낼 것으로 예측됩니다. 배출량 감축 목표와 효율성 향상을 위한 노력은 승용차 부문 내 전기화 확산을 주도하고 있습니다. 자동차 제조사들은 주행 거리와 차량 동역학을 최적화하기 위해 경량 구동계 모듈, 모듈식 아키텍처, 대용량 배터리 시스템을 도입하고 있습니다. 소비자들은 확대되는 충전 네트워크와 정부의 지원 정책의 혜택을 누리고 있으며, 이는 도시 및 교외 지역 전반에 걸쳐 전기차 채택을 가속화하고 있습니다. 최신 승용 전기차에는 회생 제동, 실시간 에너지 최적화, 커넥티드 카 시스템과 같은 통합 기술이 적용되어 있으며, 이 모든 기술은 첨단 전기 구동계 부품에 의존하고 있습니다.

북미의 자동차 전기 구동계 부품 시장은 2025년 172억 달러에 달했습니다. 주요 시장 간 전기차 표준을 조화시키려는 지역적 노력은 국경을 넘는 공급 제약을 완화하고 구동계 시스템의 대량 생산을 가능하게 하고 있습니다. 공급업체 간의 산업 협력은 차세대 e-액슬 기술 및 통합 추진 플랫폼의 개발을 촉진하고 있습니다. 동시에, 2025년 내내 지속되는 충전 인프라 확장은 소비자 신뢰를 강화하고 전기 구동계 부품에 대한 추가 수요를 자극하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전기차(EV)의 급속한 보급 및 전기화 추진

- 엄격한 배출규제 및 정부 정책

- 배터리 비용 저하와 기술 성능 향상

- EV 충전 인프라 확충

- 업계의 잠재적 위험 및 과제

- 높은 생산 비용 및 부품 비용

- 공급망 취약성 및 원자재 제약

- 시장 기회

- 고급 파워 일렉트로닉스 및 경량 모듈 설계

- 신흥 및 개발도상국 시장

- 지속가능성 및 재활용 솔루션

- 협업 및 산업 간 파트너십

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 자동차 혁신 연합(Alliance for Automotive Innovation)

- 자동차 산업 행동 그룹(Automotive Industry Action Group)

- 유럽

- 유럽 자동차 공업회

- 유엔 유럽 경제위원회(UNECE) 자동차 규제 조화 세계 포럼(WP.29)

- 아시아태평양

- APEC 자동차 대화

- ASEAN 자동차연맹

- 라틴아메리카

- 멕시코 전기자동차진흥협회

- 브라질 전기자동차협회

- 중동 및 아프리카

- 걸프 협력 회의 표준화기구

- 남아프리카 규격국

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 가격 분석

- 제품별 가격 설정

- 지역별 가격 설정

- 생산 통계

- 생산 허브

- 소비 허브

- 수출과 수입

- 원가 내역 분석

- 벤더의 비용 구조

- 비용 부품 적용

- 지속적인 운영 비용

- 고객 간접 비용

- 특허 분석

- 지속가능성 및 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고찰

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카(MEA)

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 부품별(2022-2035년)

- 배터리 팩

- 전동 드라이브 모듈

- DC/AC 인버터

- DC/DC 컨버터

- 열 시스템

- 배전 모듈(PDM)

- 기타

제6장 시장 추계 및 예측 : 용도별(2022-2035년)

- 배터리식 전기자동차(BEV)

- 하이브리드 전기자동차(HEV)

- 플러그인 하이브리드 자동차(PHEV)

- 연료전지자동차(FCEV)

제7장 시장 추계 및 예측 : 차량별(2022-2035년)

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- LCV(소형 상용차)

- MCV(중형 상용차)

- HCV(대형 상용차)

제8장 시장 추계 및 예측 : 판매 채널별(2022-2035년)

- OEM

- 애프터마켓

제9장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 폴란드

- 루마니아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ANZ

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카(MEA)

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계 기업

- Aisin

- BorgWarner

- Continental

- Denso

- Eaton

- Hitachi Astemo

- Hyundai Mobis

- Magna International

- Marelli

- Robert Bosch

- Valeo

- ZF Friedrichshafen

- 지역 기업

- BYD Company

- Contemporary Amperex Technology

- Dana

- Infineon Technologies

- LG Energy Solution

- MAHLE

- Nidec

- Panasonic(Automotive Division)

- 신흥 기업

- American Axle &Manufacturing

- GKN Automotive(Dowlais Group)

- Mitsubishi Electric

- QuantumScape

- WiTricity

The Global Automotive Electric Drivetrain Components Market was valued at USD 63.4 billion in 2025 and is estimated to grow at a CAGR of 24.1% to reach USD 488.8 billion by 2035.

Rapid electrification across the automotive sector is accelerating demand for advanced electric drivetrain systems. Tightening emission standards worldwide compel original equipment manufacturers to transition toward electric vehicle platforms at a faster pace. This regulatory pressure is significantly increasing the production of e-drives, inverters, power electronics, and integrated electric propulsion modules. Continuous cost reductions in lithium-ion battery manufacturing and improvements in production efficiency are further reshaping vehicle pricing structures, making electric vehicles more competitive. As battery costs decline, manufacturers are scaling production of lightweight electric motors and high-efficiency inverter systems to meet growing global demand. Advancements in drivetrain technology are also enhancing vehicle range, charging compatibility, and overall system performance, which supports broader EV adoption. Automakers are integrating intelligent e-axles, connected control modules, and advanced diagnostics into electric drivetrain architectures to optimize real-time monitoring and energy management. The combination of regulatory mandates, falling battery costs, and performance-driven innovation is positioning electric drivetrain components as a core growth engine within the global automotive industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $63.4 Billion |

| Forecast Value | $488.8 Billion |

| CAGR | 24.1% |

The battery packs segment held a 26% share in 2025 and is anticipated to grow at a CAGR of 26.4% from 2026 to 2035. Ongoing advancements in energy density, battery management systems, and next-generation cell chemistries are improving driving range and operational safety. Industry focus remains centered on faster charging capabilities, enhanced durability, and cost optimization. Emerging battery technologies and evolving material compositions are expected to further strengthen performance benchmarks and manufacturing scalability throughout the forecast period.

The passenger cars segment accounted for 65% share in 2025 and is forecast to grow at a CAGR of 25.2% between 2026 and 2035. Emission reduction targets and the pursuit of improved efficiency drive increasing electrification within the passenger vehicle segment. Automakers are deploying lightweight drivetrain modules, modular architectures, and high-capacity battery systems to optimize range and vehicle dynamics. Consumers are benefiting from expanding charging networks and supportive government incentives, which are accelerating adoption across urban and suburban regions. Modern passenger electric vehicles incorporate integrated technologies such as regenerative braking, real-time energy optimization, and connected vehicle systems, all of which rely on advanced electric drivetrain components.

North America Automotive Electric Drivetrain Components Market reached USD 17.2 billion in 2025. Regional efforts to harmonize electric vehicle standards across major markets are reducing cross-border supply constraints and enabling higher-volume manufacturing of drivetrain systems. Industry collaboration among suppliers is fostering the development of next-generation e-axle technologies and integrated propulsion platforms. At the same time, continued expansion of charging infrastructure throughout 2025 is strengthening consumer confidence and stimulating further demand for electric drivetrain components.

Key companies operating in the Global Automotive Electric Drivetrain Components Market include Robert Bosch, BorgWarner, ZF Friedrichshafen, Magna International, Denso, Continental, GKN Automotive, Hyundai Mobis, Dana, and Hitachi Astemo. Companies competing in the Global Automotive Electric Drivetrain Components Market are reinforcing their competitive edge through sustained investment in research and development, strategic partnerships, and vertical integration. Manufacturers are advancing high-efficiency e-drive systems, compact inverters, and integrated e-axle platforms to enhance performance and reduce system weight. Collaborations with automakers secure long-term supply agreements and early-stage integration into new electric vehicle platforms. Firms are expanding production capacity and localizing supply chains to mitigate risk and improve responsiveness.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Application

- 2.2.4 Vehicle

- 2.2.5 Sales channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid EV adoption & electrification push

- 3.2.1.2 Strict emission regulations & government policies

- 3.2.1.3 Declining battery costs & improving tech performance

- 3.2.1.4 Expansion of EV charging infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production & component costs

- 3.2.2.2 Supply chain vulnerabilities & raw material constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Advanced power electronics & lightweight modular designs

- 3.2.3.2 Emerging & developing markets

- 3.2.3.3 Sustainability & recycling solutions

- 3.2.3.4 Collaborations & cross industry partnerships

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Alliance for Automotive Innovation

- 3.4.1.2 Automotive Industry Action Group

- 3.4.2 Europe

- 3.4.2.1 European Automobile Manufacturers’ Association

- 3.4.2.2 UNECE World Forum for Harmonization of Vehicle Regulations (WP.29)

- 3.4.3 Asia Pacific

- 3.4.3.1 APEC Automotive Dialogue

- 3.4.3.2 ASEAN Automotive Federation

- 3.4.4 Latin America

- 3.4.4.1 Mexican Association for the Promotion of Electric Vehicles

- 3.4.4.2 Brazilian Electric Vehicle Association

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Cooperation Council Standardization Organization

- 3.4.5.2 South African Bureau of Standards

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis

- 3.8.1 Pricing by product

- 3.8.2 Pricing by region

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.10.1 Vendor cost structure

- 3.10.2 Implementation of cost components

- 3.10.3 Ongoing operational costs

- 3.10.4 Indirect customer costs

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Thousand units)

- 5.1 Key trends

- 5.2 Battery packs

- 5.3 Electric drive module

- 5.4 DC/AC inverter

- 5.5 DC/DC converter

- 5.6 Thermal system

- 5.7 Power distribution module (PDM)

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Thousand units)

- 6.1 Key trends

- 6.2 Battery electric vehicle (BEV)

- 6.3 Hybrid electric vehicle (HEV)

- 6.4 Plug-in hybrid electric vehicle (PHEV)

- 6.5 Fuel cell electric vehicle (FCEV)

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV (Light commercial vehicle)

- 7.3.2 MCV (Medium commercial vehicle)

- 7.3.3 HCV (Heavy commercial vehicle)

Chapter 8 Market Estimates & Forecast, By Sales channel, 2022 - 2035 ($Mn, Thousand units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 Aisin

- 10.1.2 BorgWarner

- 10.1.3 Continental

- 10.1.4 Denso

- 10.1.5 Eaton

- 10.1.6 Hitachi Astemo

- 10.1.7 Hyundai Mobis

- 10.1.8 Magna International

- 10.1.9 Marelli

- 10.1.10 Robert Bosch

- 10.1.11 Valeo

- 10.1.12 ZF Friedrichshafen

- 10.2 Regional players

- 10.2.1 BYD Company

- 10.2.2 Contemporary Amperex Technology

- 10.2.3 Dana

- 10.2.4 Infineon Technologies

- 10.2.5 LG Energy Solution

- 10.2.6 MAHLE

- 10.2.7 Nidec

- 10.2.8 Panasonic (Automotive Division)

- 10.3 Emerging players

- 10.3.1 American Axle & Manufacturing

- 10.3.2 GKN Automotive (Dowlais Group)

- 10.3.3 Mitsubishi Electric

- 10.3.4 QuantumScape

- 10.3.5 WiTricity