|

시장보고서

상품코드

1982324

운송용 바이오연료 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Transportation Biofuel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

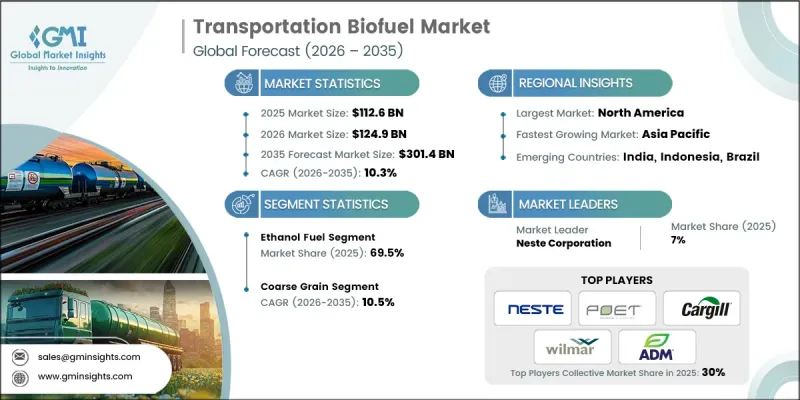

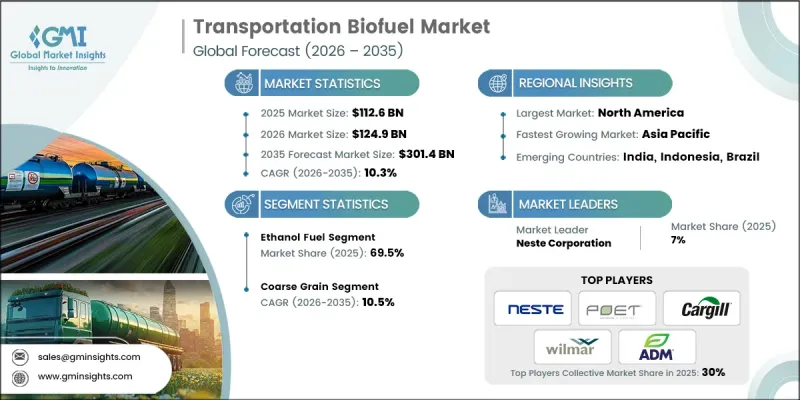

세계의 운송용 바이오연료 시장은 2025년 1,126억 달러로 평가되었고 CAGR은 10.3%를 나타낼 것으로 보이며, 2035년까지 3,014억 달러에 이를 것으로 추정됩니다.

주요 시장의 정책 체계는 광범위한 재생에너지 목표에서 벗어나, 바이오연료를 장기적인 운송 부문 탈탄소화 전략에 반영하는 구체적인 연료 의무화 정책으로 진화하고 있습니다. 이러한 전환은 항공, 도로 운송, 그리고 점차 확대되는 해운 부문 전반에서 뚜렷하게 나타나고 있으며, 각 부문에서는 적격성 규정과 지속가능성 기준에 따라 어떤 연료가 규정 준수 요건을 충족하는지 정의하고 있습니다. 각국이 이러한 프레임워크를 시행함에 따라, 전문화된 보고 체계, 등록 시스템, 그리고 기본값(default values)은 첨단 바이오연료 및 재생 가능 드롭인 연료에 대한 투자를 뒷받침하는 규칙 중심의 환경을 조성하고 있습니다. 항공 분야에서 액체 에너지의 대안이 제한적이라는 점을 고려할 때, 지속가능 항공 연료(SAF)는 주요 성장 동력입니다. 최소 혼합 요건 및 지속가능성 기준에 대한 규제적 확실성은 정유소 전환, 공동 처리 이니셔티브, 그리고 그린필드 프로젝트를 촉진하고 있습니다. 항공사, 공항, 연료 공급업체들은 통합 조달, 인증, 그리고 ‘북 앤 클레임(book-and-claim)’ 메커니즘을 도입하고 있습니다. SAF가 시범 프로그램에서 일상적인 공급으로 전환됨에 따라, 승인된 생산 경로 전반에 걸쳐 장기 공급 계약, 생산 능력 확대, 원료 다각화가 가속화되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시장 규모 | 1,126억 달러 |

| 예측 금액 | 3,014억 달러 |

| CAGR | 10.3% |

에탄올 부문은 2025년 69.5%의 점유율을 차지했으며, 2035년까지 연평균 성장률(CAGR) 10.5%로 성장할 것으로 예상됩니다. 이러한 성장은 농업 정책, 정유소 통합, 그리고 저탄소 옥탄가를 장려하는 운송 부문 탈탄소화 인센티브의 융합에 의해 주도되고 있습니다. 정부는 혼합 의무 비율과 허용 원료의 범위를 지속적으로 확대하고 있으며, 자동차 제조사들은 고농도 혼합 연료의 호환성을 검증하고, 연료 소매업체들은 공급량을 늘려 도입 장벽을 낮추고 있습니다. 생산자들은 변화하는 탄소 회계 체계 하에서 경쟁력을 강화하기 위해 공정 최적화, 탄소 집약도 감소, 부산물 가치 증대에 투자하고 있습니다.

2025년 기준 37.8%의 시장 점유율을 차지한 잡곡 부문은 2035년까지 연평균 성장률(CAGR) 10.5%로 성장할 것으로 전망됩니다. 지리적으로 분산된 대규모 공급망, 성숙한 전환 기술, 예측 가능한 부산물 경제성 덕분에 잡곡은 에탄올 생태계의 핵심을 이루고 있습니다. 경량 차량의 전기화 추세가 확대되고 있음에도 불구하고, 거친 곡물 에탄올은 옥탄가 향상 효과, 광범위한 차량 호환성, 그리고 미래 바이오 중간체 및 e-연료 전구체 플랫폼으로서의 잠재력 덕분에 가솔린 시장에서 구조적인 역할을 유지하고 있습니다.

미국의 운송용 바이오연료 시장은 93%의 점유율을 차지하며, 2025년에는 339억 달러 규모에 이를 것으로 전망됩니다. 미국의 재생 가능 연료 표준(RFS)은 크레딧 시장, 경로 적격성 및 연간 기준을 통해 생산자와 혼합업체의 행동을 뒷받침하며, 셀룰로오스 에탄올, 운송용 바이오가스, 저탄소 에탄올 및 바이오디젤에 대한 투자를 지원합니다. 연방 및 지방 정부 프로그램은 지속 가능성 측정 기준을 점차 정교화하여 공정 효율성, 탄소 집약도 감소, 열 통합, 탄소 포집 준비성 및 원료 다각화를 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- PESTEL 분석

- 새로운 기회와 동향

- 디지털화와 IoT의 통합

- 신흥 시장 진출

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 경쟁 벤치마킹

- 전략적 대시보드

- 혁신 및 기술 동향

제5장 시장 규모 및 예측 : 연료별(2022-2035년)

- 바이오디젤

- 에탄올

- 기타

제6장 시장 규모 및 예측 : 원료별(2022-2035년)

- 잡곡

- 사탕수수

- 식물성 기름

- 기타

제7장 시장 규모 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 스페인

- 영국

- 이탈리아

- 아시아태평양

- 중국

- 인도

- 인도네시아

- 호주

- 한국

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 라틴아메리카

- 브라질

- 아르헨티나

제8장 기업 프로파일

- ADM

- Borregaard

- BTG Bioliquids

- Cargill

- Chevron Corporation

- Clariant

- COFCO

- FutureFuel

- Inpasa

- Munzer Bioindustrie

- My Eco Energy

- Neste Corporation

- POET

- Praj Industries

- The Andersons

- TotalEnergies

- UPM

- Verbio

- Wilmar International

- Zilor

The Global Transportation Biofuel Market was valued at USD 112.6 billion in 2025 and is estimated to grow at a CAGR of 10.3% to reach USD 301.4 billion by 2035.

Policy frameworks across key markets are evolving from broad renewable targets to precise fuel mandates that embed biofuels into long-term transport decarbonization strategies. This transition is evident across aviation, road transport, and increasingly maritime sectors, where eligibility rules and sustainability criteria define which fuels qualify for compliance. As nations implement these frameworks, professionalized reporting, registry systems, and default values create a rules-driven environment that supports investment in advanced biofuels and renewable drop-in fuels. Sustainable aviation fuel (SAF) is a major growth driver, given the limited alternatives to liquid energy in aviation. Regulatory certainty around minimum blending requirements and sustainability standards is encouraging refinery conversions, co-processing initiatives, and greenfield projects. Airlines, airports, and fuel suppliers are adopting integrated procurement, certification, and book-and-claim mechanisms. As SAF moves from pilot programs to routine supply, long-term offtake agreements, capacity expansion, and feedstock diversification are accelerating across approved production pathways.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $112.6 Billion |

| Forecast Value | $301.4 Billion |

| CAGR | 10.3% |

The ethanol segment held 69.5% share in 2025 and is expected to grow at a CAGR of 10.5% through 2035. Growth is driven by the convergence of agricultural policy, refinery integration, and transport decarbonization incentives rewarding low-carbon octane. Governments continue expanding blending mandates and eligible feedstocks, while automakers validate higher blend compatibility and fuel retailers increase availability, reducing adoption barriers. Producers are investing in process optimization, carbon intensity reduction, and coproduct valorization to enhance competitiveness under evolving carbon accounting frameworks.

The coarse grain segment accounted for 37.8% share in 2025 and is projected to grow at a CAGR of 10.5% by 2035. Its large, geographically diversified supply, mature conversion technologies, and predictable coproduct economics make coarse grains central to the ethanol ecosystem. Despite growing electrification in light-duty fleets, coarse-grain ethanol maintains a structural role in gasoline pools due to octane contribution, broad vehicle compatibility, and potential as a platform for future bio-intermediates and e-fuel precursors.

U.S. Transportation Biofuel Market held 93% share, generating USD 33.9 billion in 2025, driven by a robust compliance framework, mature supply chains, and focus on lifecycle performance. The U.S. Renewable Fuel Standard (RFS) underpins producer and blender behavior through credit markets, pathway eligibility, and annual standards, supporting investment in cellulosic ethanol, biogas for transport, and low-carbon ethanol and biodiesel. Federal and subnational programs increasingly refine sustainability measurement, promoting process efficiency, carbon intensity reduction, heat integration, carbon capture readiness, and feedstock diversification.

Key players in the Global Transportation Biofuel Market include Neste Corporation, POET, ADM, Praj Industries, Borregaard, FutureFuel, My Eco Energy, Wilmar International, Clariant, TotalEnergies, BTG Bioliquids, Chevron Corporation, Cargill, UPM, Inpasa, Verbio, The Andersons, Munzer Bioindustrie, COFCO, and Zilor. Companies in the Global Transportation Biofuel Market are employing multiple strategies to solidify their market position. They are investing in R&D to optimize conversion efficiency, reduce carbon intensity, and expand eligible feedstocks. Strategic partnerships with OEMs, fuel distributors, and aviation stakeholders enhance market access and long-term offtake agreements. Firms are also modernizing production infrastructure, adopting co-processing and integrated refinery approaches, and expanding geographically to capture emerging demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Fuel trends

- 2.1.3 Feedstock trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive benchmarking

- 4.4 Strategic dashboard

- 4.5 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million, Mtoe)

- 5.1 Key trends

- 5.2 Biodiesel

- 5.3 Ethanol

- 5.4 Others

Chapter 6 Market Size and Forecast, By Feedstock, 2022 - 2035 (USD Million, Mtoe)

- 6.1 Key trends

- 6.2 Coarse grain

- 6.3 Sugar crop

- 6.4 Vegetable oil

- 6.5 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million, Mtoe)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Spain

- 7.3.4 UK

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Indonesia

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ADM

- 8.2 Borregaard

- 8.3 BTG Bioliquids

- 8.4 Cargill

- 8.5 Chevron Corporation

- 8.6 Clariant

- 8.7 COFCO

- 8.8 FutureFuel

- 8.9 Inpasa

- 8.10 Munzer Bioindustrie

- 8.11 My Eco Energy

- 8.12 Neste Corporation

- 8.13 POET

- 8.14 Praj Industries

- 8.15 The Andersons

- 8.16 TotalEnergies

- 8.17 UPM

- 8.18 Verbio

- 8.19 Wilmar International

- 8.20 Zilor