|

시장보고서

상품코드

1982325

최소 침습 수술 기구 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Minimally Invasive Surgical Instrument Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

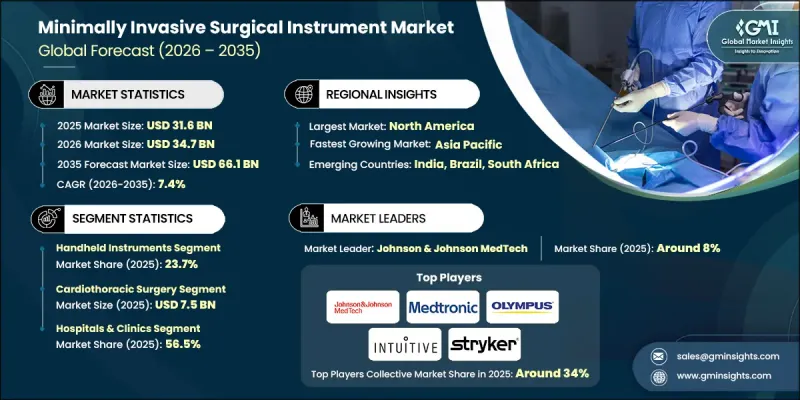

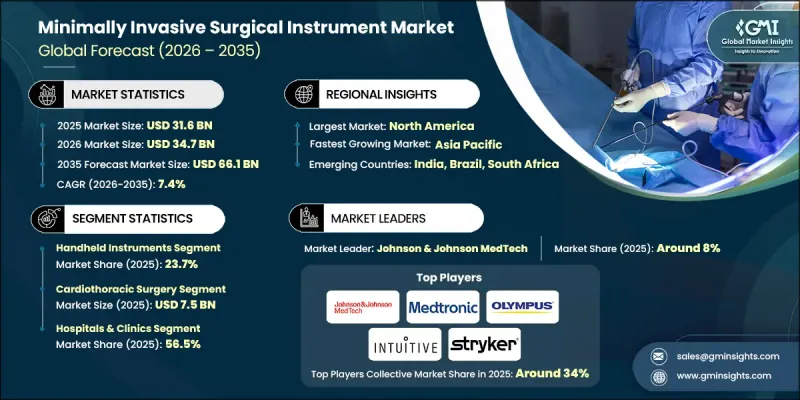

세계의 최소 침습 수술 기구 시장은 2025년 316억 달러로 평가되었고 CAGR은 7.4%를 나타낼 것으로 보이며, 2035년까지 661억 달러에 이를 것으로 추정됩니다.

이 시장은 최소 침습 수술에 대한 수요 급증, 로봇 보조 수술의 확산, 지속적인 기술 혁신, 그리고 만성 질환 유병률 증가에 힘입어 성장하고 있습니다. 선진국의 인구 고령화와 외래 수술 증가 추세는 시장 확장을 더욱 뒷받침하고 있습니다. 최근 수술 기구의 발전으로 인해 여러 전문 분야에 걸쳐 최소 침습적 시술의 범위가 확대되었습니다. 햅틱 피드백(haptic feedback)과 같은 기술은 외과의사의 촉각 인식을 향상시켰으며, 일회용 첨단 에너지 장치는 의료 시설의 무균 상태와 비용 효율성을 개선했습니다. 로봇 보조 플랫폼이 널리 보급됨에 따라, 과거 개복 수술로만 가능했던 시술도 이제 최소 침습적으로 수행할 수 있게 되었습니다. 전반적으로 첨단 기구, 시술 효율성, 병원 비용 절감 효과의 결합이 세계적으로 이러한 기술의 도입을 주도하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시장 규모 | 316억 달러 |

| 예측 금액 | 661억 달러 |

| CAGR | 7.4% |

2025년 기준 핸드헬드 기구 부문은 23.7%의 시장 점유율을 차지했습니다. 이 기구들의 혁신은 인체공학적 설계, 접근이 어려운 해부학적 부위를 위한 관절 가동 범위 확대, 티타늄 합금 및 첨단 폴리머와 같은 가볍고 내구성이 뛰어난 재료의 사용에 중점을 두고 있습니다. 주요 핸드헬드 도구로는 복강경 집게, 가위, 바늘 홀더 및 기타 특수 기구가 있습니다. 일회용 및 무감염 기구에 대한 강조 또한 이 부문의 성장을 뒷받침하고 있습니다.

2025년 심장흉부 수술 분야 시장 규모는 75억 달러에 달했습니다. 최소 침습 심장 시술은 일반적으로 기존 방식보다 작은 절개를 사용하여 회복 기간, 감염 위험 및 기능적 제한을 줄여줍니다. 로봇 보조 플랫폼은 3차원 시각화 및 향상된 기구 가동 범위를 제공하여 판막 수복과 같은 정밀한 시술을 보다 효율적이고 안전하게 수행할 수 있게 합니다.

2025년 미국의 최소 침습 수술 기구 시장은 116억 달러로 평가되었습니다. 이 지역의 성장은 높은 1인당 의료비 지출, 정교한 보험 급여 제도, 그리고 첨단 의료 기술의 조기 도입에 힘입고 있습니다. 민간 보험과 메디케어(Medicare)가 최소 침습적 시술을 광범위하게 보장함에 따라 다양한 외과 전문 분야에서 수요가 뒷받침되고 있습니다. 또한, 의료 서비스 제공자들은 입원 기간 단축과 환자 예후 개선이 가져오는 비용상의 이점을 인식하고 있어, 최소 침습적 인프라에 대한 투자를 장려하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 조사 접근

- 품질에 관한 대처

- GMI AI 정책 및 데이터 무결성에 대한 노력

- 출처의 일관성에 관한 프로토콜

- GMI AI 정책 및 데이터 무결성에 대한 노력

- 조사의 경위와 신뢰도 평가

- 연구 경로 컴포넌트

- 평가의 컴포넌트

- 데이터 수집

- 1차 정보의 일부 리스트

- 데이터 마이닝 출처

- 유료 출처

- 지역별 출처

- 유료 출처

- 기본 추정 및 산출 방법

- 기준연도의 산출

- 예측 모델

- 정량화된 시장 영향 분석

- 성장 매개변수가 예측에 미치는 수학적 영향

- 정량화된 시장 영향 분석

- 조사의 투명성에 관한 보충

- 출처 표시 프레임워크

- 품질 보증 지표

- 신뢰에 대한 노력

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성질환의 유병률 증가

- 수술 기구의 기술적 진보

- 로봇 지원 수술의 보급 확대

- 최소 침습 수술에 대한 수요 급증

- 업계의 잠재적 위험 및 과제

- 수술기구의 높은 비용

- 개발도상국의 상환 과제

- 기회

- 전기 수술 및 에너지 장비의 기술 혁신

- 원격 수술 및 원격 지원 수술 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 가격 분석

- 상환 시나리오

- 북미

- 유럽

- 아시아태평양

- 정책 환경

- 공급망 분석

- 환경 및 지속가능성에 대한 노력

- 투자 기회와 벤처 캐피탈의 동향

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

- 장래 시장 동향

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 제품별(2022-2035년)

- 핸드헬드 기구

- 복강경 집게

- 주도기 및 거상기

- 확장기

- 봉합 기구

- 기타 핸드헬드 기구

- 모니터링 및 시각화 장치

- 수술용 스코프

- 복강경

- 관절경

- 비뇨기과용 내시경

- 신경 내시경

- 기타 내시경

- 팽창 장치

- 절단 기구

- 가이드 기구

- 가이드 카테터

- 가이드 와이어

- 보조 기구

- 전기수술 기구

제6장 시장 추계 및 예측 : 수술 유형별(2022-2035년)

- 심장흉부 수술

- 정형외과 수술

- 소화기 수술

- 비뇨기과 수술

- 부인과 수술

- 미용 및 비만 수술

- 기타

제7장 시장 추계 및 예측 : 최종 용도별(2022-2035년)

- 병원 및 진료소

- 외래수술센터(ASC)

- 기타 최종 사용자

제8장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Abbott

- B. Braun

- Becton, Dickinson and Company

- Biorad Medisys

- Boston Scientific

- CONMED

- FUJIFILM

- Intuitive Surgical Operations

- Johnson & Johnson MedTech

- KARL STORZ

- Medtronic

- OLYMPUS

- Smith Nephew

- Stryker

- WEXLER SURGICAL

- ZIMMER BIOMET

The Global Minimally Invasive Surgical Instrument Market was valued at USD 31.6 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 66.1 billion by 2035.

The market is propelled by a surge in demand for less invasive surgical procedures, wider adoption of robotic-assisted surgeries, ongoing technological innovation, and the increasing prevalence of chronic conditions. Aging populations and the rising trend of outpatient surgeries in developed countries are further supporting market expansion. Recent developments in surgical instruments have expanded the range of minimally invasive procedures across multiple specialties. Technologies such as haptic feedback have enhanced surgeons' tactile perception, while disposable advanced energy devices improve sterility and cost-effectiveness for healthcare facilities. Robotic-assisted platforms have become widely accessible, allowing procedures once limited to open surgeries to now be performed minimally invasively. Overall, the combination of advanced instrumentation, procedural efficiency, and hospital cost-saving benefits is driving the adoption of these technologies globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $31.6 Billion |

| Forecast Value | $66.1 Billion |

| CAGR | 7.4% |

The handheld instruments segment held a 23.7% share in 2025. Innovations in these devices focus on ergonomics, increased articulation for hard-to-reach anatomical areas, and the use of lightweight, durable materials like titanium alloys and advanced polymers. Core handheld tools include laparoscopic graspers, scissors, needle holders, and other specialty instruments. Emphasis on disposable and infection-free instruments is also supporting growth in this category.

The cardiothoracic surgery segment reached USD 7.5 billion in 2025. Minimally invasive cardiac procedures typically use smaller incisions rather than traditional approaches, reducing recovery times, infection risk, and functional limitations. Robotic-assisted platforms provide three-dimensional visualization and enhanced instrument articulation, enabling precise procedures such as valve repairs to be conducted more efficiently and safely.

U.S. Minimally Invasive Surgical Instrument Market was valued at USD 11.6 billion in 2025. Growth in the region is fueled by high per-capita healthcare spending, sophisticated reimbursement systems, and early adoption of cutting-edge medical technologies. The widespread coverage of minimally invasive procedures by private insurance and Medicare supports demand across multiple surgical specialties. Additionally, healthcare providers recognize the cost benefits of shorter hospital stays and improved patient outcomes, encouraging investment in minimally invasive infrastructure.

Key players in the Global Minimally Invasive Surgical Instrument Market include Johnson & Johnson MedTech, Intuitive Surgical Operations, Medtronic, B. Braun, Boston Scientific, Stryker, Abbott, OLYMPUS, Smith + Nephew, Becton, Dickinson and Company, KARL STORZ, ZIMMER BIOMET, WEXLER SURGICAL, FUJIFILM, and Biorad Medisys. Market leaders adopt several strategies to strengthen their presence. They focus heavily on research and development to launch advanced, ergonomically designed instruments and integrate robotic-assisted technology. Companies expand both direct and indirect distribution networks while forming strategic collaborations with hospitals and surgical centers to increase adoption. Marketing campaigns highlight clinical efficacy, procedural efficiency, and cost benefits, while training programs ensure surgeon proficiency with new devices. Firms also pursue mergers, acquisitions, and geographic expansion to gain market share and enhance global competitiveness, leveraging innovation and strong brand recognition to maintain leadership in the rapidly growing minimally invasive surgical instruments sector.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Surgery type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Technological advancements in surgical instruments

- 3.2.1.3 Growing adoption of robotic-assisted surgeries

- 3.2.1.4 Surging demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of surgical instruments

- 3.2.2.2 Reimbursement challenges in developing countries

- 3.2.3 Opportunities

- 3.2.3.1 Technological innovations in electrosurgical and energy devices

- 3.2.3.2 Expansion of tele-surgery and remote-assisted operations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis

- 3.7 Reimbursement scenario

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.8 Policy landscape

- 3.9 Supply chain analysis

- 3.10 Environmental and sustainability initiatives

- 3.11 Investment opportunities and venture capital trends

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Gap analysis

- 3.15 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Handheld instruments

- 5.2.1 Graspers

- 5.2.2 Retractors/elevators

- 5.2.3 Dilators

- 5.2.4 Suturing instruments

- 5.2.5 Other handheld instruments

- 5.3 Monitoring & visualization devices

- 5.4 Surgical scopes

- 5.4.1 Laparoscopes

- 5.4.2 Arthroscopes

- 5.4.3 Urology endoscopes

- 5.4.4 Neuroendoscopes

- 5.4.5 Other scopes

- 5.5 Inflation devices

- 5.6 Cutter instruments

- 5.7 Guiding devices

- 5.7.1 Guiding catheters

- 5.7.2 Guidewires

- 5.8 Auxiliary devices

- 5.9 Electrosurgical devices

Chapter 6 Market Estimates and Forecast, By Surgery Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Cardiothoracic surgery

- 6.3 Orthopedic surgery

- 6.4 Gastrointestinal surgery

- 6.5 Urological surgery

- 6.6 Gynecological surgery

- 6.7 Cosmetic & bariatric surgery

- 6.8 Other surgery types

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals & clinics

- 7.3 Ambulatory surgical centers

- 7.4 Other end-users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 B. Braun

- 9.3 Becton, Dickinson and Company

- 9.4 Biorad Medisys

- 9.5 Boston Scientific

- 9.6 CONMED

- 9.7 FUJIFILM

- 9.8 Intuitive Surgical Operations

- 9.9 Johnson & Johnson MedTech

- 9.10 KARL STORZ

- 9.11 Medtronic

- 9.12 OLYMPUS

- 9.13 Smith + Nephew

- 9.14 Stryker

- 9.15 WEXLER SURGICAL

- 9.16 ZIMMER BIOMET