|

시장보고서

상품코드

1982328

자동차 스프링 시장의 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Spring Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

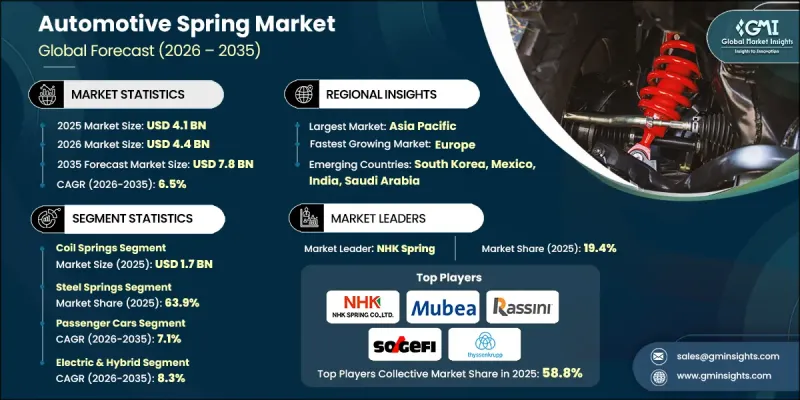

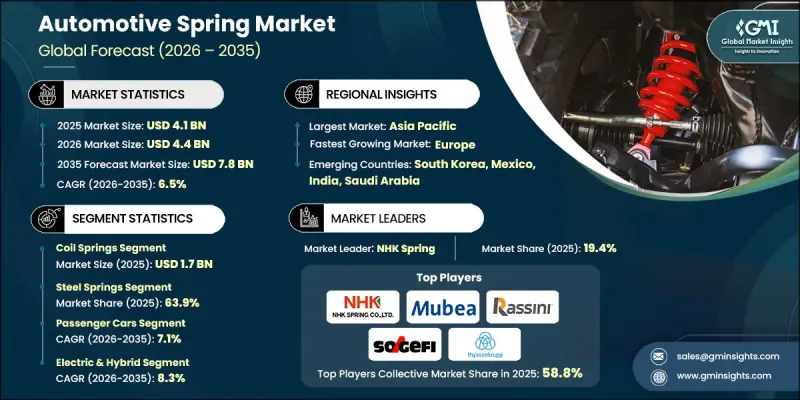

세계의 자동차 스프링 시장은 2025년 41억 달러로 평가되었고 CAGR은 6.5%를 나타낼 것으로 보이며, 2035년까지 78억 달러에 이를 것으로 추정됩니다.

자동차 스프링은 승용차와 상용차 전반에 걸쳐 하중 관리, 승차감, 안정성을 지원하는 핵심적인 구조 및 서스펜션 부품으로 자리 잡고 있습니다. 세계의 자동차 생산량의 꾸준한 증가는 스프링 시스템에 대한 장기적인 수요를 뒷받침하고 있습니다. 여러 경제권에서 가처분 소득이 증가함에 따라 차량 소유율이 상승하고 있으며, 이는 세계적으로 자동차 생산량 증가에 기여하고 있습니다. 자동차 제조사들이 소비자 수요를 충족하기 위해 생산 규모를 확대함에 따라, 신뢰성 높고 성능 중심의 스프링 솔루션에 대한 필요성도 계속 증가하고 있습니다. 이와 동시에, 전기 모빌리티로의 전환은 자동차 스프링 시장 내 제품 개발 전략을 재편하고 있습니다. 제조사들은 에너지 효율과 주행 거리를 향상시키기 위해 경량화 엔지니어링 솔루션을 최우선으로 고려하고 있습니다. 이러한 변화는 진화하는 자동차 아키텍처에 부합하는 첨단 재료와 최적화된 스프링 설계의 도입을 촉진하고 있습니다. 또한, 아시아, 라틴 아메리카, 일부 중동 및 아프리카 지역에 새로운 자동차 제조 허브가 등장함에 따라 공급업체들은 현지 생산 시설을 구축하고 OEM과의 장기적인 파트너십을 강화할 기회를 얻고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시점 시장 규모 | 41억 달러 |

| 예측 금액 | 78억 달러 |

| CAGR | 6.5% |

가스 스프링 부문은 2026년부터 2035년까지 연평균 성장률(CAGR) 8.1%로 성장할 것으로 예상됩니다. 이러한 부품은 제어된 움직임과 향상된 안전성을 제공하기 위해 현대식 차량 시스템에 점점 더 많이 통합되고 있습니다. 부드럽고 정밀한 움직임을 제공하는 능력은 사용자 편의성과 운영 신뢰성을 높여줍니다. 전기차 및 하이브리드 차량에서 가스 스프링은 정밀한 동작 제어가 필요한 특수한 구조 및 실내 부품에 사용됩니다. 규제 압력과 변화하는 소비자 선호도에 따라 세계적으로 전기차 보급이 가속화됨에 따라, 첨단 가스 스프링 솔루션의 중요성은 계속해서 높아지고 있습니다.

강철 스프링 부문은 2025년에 63.9%의 점유율을 차지하며, 2035년까지 48억 달러에 이를 것으로 예측됩니다. 원자재 가격 변동에도 불구하고, 강철은 우수한 강중량비와 내구성을 바탕으로 여전히 선호되는 재료로 남아 있습니다. 예측 기간 동안 강철 스프링은 복합재나 폴리머 기반 제품과 같은 대체재에 비해 광범위한 채택을 유지할 것으로 예상됩니다. 비용 효율성, 대규모 제조 능력, 일관된 품질 기준 덕분에 강철 스프링은 OEM 생산과 애프터마켓 교체 수요 모두에 있어 신뢰할 수 있는 선택지입니다. 확립된 공급망과 경쟁력 있는 가격은 성숙한 자동차 시장과 신흥 자동차 시장 전반에서 강철 스프링의 우위를 더욱 공고히 합니다.

미국의 자동차 스프링 시장은 2025년 4억 6,080만 달러에 달했습니다. 미국은 방대한 자동차 제조 기반, 견고한 애프터마켓 생태계, 승용차 및 경트럭의 강력한 생산량을 바탕으로 중요한 시장을 형성하고 있습니다. 지속적인 차량 생산과 노후화된 차량 보유량 증가로 인한 교체 수요 증가는 시장의 꾸준한 확장을 뒷받침하고 있습니다. 2030년까지 무공해 모빌리티를 촉진하기 위한 규제 체계는 서스펜션 부품 설계 요건에 영향을 미치고 있으며, 제조사들은 전기차의 중량 분배 및 성능 특성을 수용할 수 있는 스프링 시스템을 개발하도록 유도하고 있습니다. 동시에 자동차 제조사들은 조달 전략에 영향을 미치는 변화하는 정책 환경과 공급망의 복잡성을 헤쳐 나가고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계 자동차 생산 대수 증가

- 상용차에 대한 수요 증가

- 전기자동차(EV) 시장 확대

- 자동차 애프터마켓 수요 증가

- 업계의 잠재적 위험 및 과제

- 원재료 가격 변동

- 격렬한 경쟁과 가격 압력

- 시장 기회

- 첨단 경량 스프링 재료 개발

- 신흥 자동차 시장의 성장

- 전기자동차 및 하이브리드 자동차의 확대

- 전략적 제휴 및 OEM 파트너십

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국 도로교통안전국(NHTSA)

- 캐나다 운수성

- 미국 환경보호청(EPA)

- 캘리포니아주 대기자원국(CARB)

- SAE International

- 유럽

- 유럽 위원회

- 유엔 유럽 경제위원회(UNECE)

- 유럽 자동차 공업회(ACEA)

- 유럽 표준화위원회(CEN)

- 독일 연방 자동차국(KBA)

- 아시아태평양

- 중국 공업 정보화부(MIIT)

- 중국 자동차 기술 연구센터(CATARC)

- 인도 자동차연구협회(ARAI)

- 한국 교통안전청(KOTSA)

- 라틴아메리카

- 국가교통사무국(SENATRAN)

- INMETRO

- 국토교통성

- 멕시코 국가규격(NOM)

- 중동 및 아프리카

- 걸프 협력 회의 표준화 기구(GSO)

- 아랍에미리트(UAE) 표준화 및 계량청(ESMA)

- 사우디아라비아 표준 계량 품질 기구(SASO)

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 고강도 합금강 스프링

- 경량 복합재 리프 스프링

- 차량 에어 스프링 통합

- 신흥 기술

- 탄소섬유 강화 복합재 스프링

- 내피로성 및 내식성 향상을 위한 나노 코팅

- 현재의 기술 동향

- 생산 통계

- 생산 허브

- 소비 허브

- 수출과 수입

- 가격 동향

- 지역별

- 제품별

- 원가 내역 분석

- 지속가능성과 환경에 미치는 영향

- 환경 영향 평가

- 사회적 영향과 지역사회에의 공헌

- 거버넌스와 기업의 사회적 책임

- 지속 가능한 금융 및 투자 동향

- 제품의 라이프 사이클 및 교환 사이클의 분석

- 스프링의 유형 및 차종 부문별 평균 수명

- 고장 모드와 일반적인 마모 패턴

- 차량 연령 분포와 애프터마켓 수요의 상관관계

- 차량의 전동화가 교환 사이클에 미치는 영향

- 계절적인 수요 변동과 재고 관리 패턴

- 차량의 전동화가 미치는 영향 분석

- EV의 중량 배분 변화와 스프링 설계에 대한 영향

- 배터리 팩의 중량 보상 요건

- 회생 브레이크가 서스펜션 스프링의 사양에 미치는 영향

- EV 특유의 스프링 내구성 및 피로에 관한 고려 사항

- 향후 전망과 비즈니스 기회

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카(MEA)

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 제품별(2022-2035년)

- 코일 스프링

- 리프 스프링

- 토션 스프링

- 가스 스프링

- 기타

제6장 시장 추계 및 예측 : 재료별(2022-2035년)

- 강철 스프링

- 복합재 스프링

- 플라스틱 스프링

- 기타

제7장 시장 추계 및 예측 : 적재 용량별(2022-2035년)

- 소형 스프링

- 중형 스프링

- 대형 스프링

제8장 시장 추계 및 예측 : 차량별(2022-2035년)

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- LCV

- MCV

- 대형차(HCV)

- 이륜차

제9장 시장 추계 및 예측 : 파워트레인별(2022-2035년)

- 내연기관(ICE)

- 전기자동차 및 하이브리드 자동차

- BEV

- HEV

- PHEV

- FCEV

제10장 시장 추계 및 예측 : 최종 용도별(2022-2035년)

- 서스펜션 시스템

- 엔진 밸브

- 클러치 어셈블리

- 송전 시스템

- 기타

제11장 시장 추계 및 예측 : 판매 채널별(2022-2035년)

- OEM

- 애프터마켓

제12장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 체코 공화국

- 벨기에

- 러시아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 싱가포르

- 말레이시아

- 인도네시아

- 베트남

- 태국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 중동 및 아프리카(MEA)

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제13장 기업 프로파일

- 세계 기업

- NHK Spring

- Mubea

- Sogefi

- Rassini

- GKN Automotive

- Mitsubishi Steel

- ZF Friedrichshafen

- Thyssenkrupp

- Lesjofors

- 지역 기업

- UNI AUTO

- Kilen Springs

- Olgun Celik

- Clifford Springs

- Soni Auto &Allied Industries

- Emco Industries

- Stanley Spring

- 신흥 기업

- Hendrickson

- Auto Steels

- Vikrant Auto

- Protopower Springs

The Global Automotive Spring Market was valued at USD 4.1 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 7.8 billion by 2035.

Automotive springs remain a fundamental structural and suspension component across passenger and commercial vehicles, supporting load management, ride comfort, and stability. Steady growth in global vehicle production is sustaining long-term demand for spring systems. Rising vehicle ownership levels, supported by improving disposable incomes in multiple economies, are contributing to higher automobile manufacturing volumes worldwide. As automakers scale production to meet consumer demand, the need for reliable and performance-driven spring solutions continues to increase. In parallel, the transition toward electric mobility is reshaping product development strategies within the automotive spring market. Manufacturers are prioritizing lightweight engineering solutions to enhance energy efficiency and vehicle range. This shift is encouraging the adoption of advanced materials and optimized spring designs that align with evolving automotive architectures. Additionally, the emergence of new vehicle manufacturing hubs across Asia, Latin America, and select Middle Eastern and African regions is creating opportunities for suppliers to establish localized production facilities and strengthen long-term partnerships with original equipment manufacturers.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.1 Billion |

| Forecast Value | $7.8 Billion |

| CAGR | 6.5% |

The gas springs segment is anticipated to grow at a CAGR of 8.1% from 2026 to 2035. These components are increasingly integrated into modern vehicle systems to enable controlled motion and improved safety. Their ability to deliver smooth and precise movement enhances user convenience and operational reliability. In electric and hybrid vehicles, gas springs support specialized structural and interior applications that require accurate motion management. As global electric vehicle adoption accelerates in response to regulatory pressures and evolving consumer preferences, the importance of advanced gas spring solutions continues to rise.

The steel springs segment accounted for 63.9% share in 2025 and is expected to reach USD 4.8 billion by 2035. Despite fluctuations in raw material pricing, steel remains a preferred material due to its favorable strength-to-weight ratio and durability. Over the forecast period, steel springs are expected to maintain widespread adoption compared to alternatives such as composite or polymer-based variants. Their cost efficiency, large-scale manufacturing capability, and consistent quality standards make them a reliable option for both OEM production and aftermarket replacement demand. Established supply networks and competitive pricing further reinforce their dominance across mature and emerging automotive markets.

U.S. Automotive Spring Market reached USD 460.8 million in 2025. The country represents a significant market due to its extensive vehicle manufacturing base, robust aftermarket ecosystem, and strong production of passenger vehicles and light trucks. Continuous vehicle output and rising replacement demand driven by an aging fleet are supporting steady market expansion. Regulatory frameworks aimed at promoting zero-emission mobility by 2030 are influencing suspension component design requirements, prompting manufacturers to engineer spring systems that accommodate the weight distribution and performance characteristics of electric vehicles. At the same time, automakers are navigating evolving policy environments and supply chain complexities that impact procurement strategies.

Leading companies operating in the Global Automotive Spring Market include ZF Friedrichshafen, Thyssenkrupp, NHK Spring, Mubea, Mitsubishi Steel, GKN Automotive, Sogefi, Rassini, Lesjofors, and UNI AUTO. Companies in the Global Automotive Spring Market are reinforcing their competitive positioning through material innovation, geographic expansion, and strategic collaborations. Manufacturers are investing in lightweight spring technologies, including high-strength alloys and composite materials, to support electric vehicle performance requirements. Partnerships with OEMs are enabling co-development of customized spring solutions tailored to evolving vehicle platforms. Many firms are expanding production footprints in emerging automotive hubs to strengthen supply chain resilience and reduce logistics costs.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Load Capacity

- 2.2.5 Vehicle

- 2.2.6 Powertrain

- 2.2.7 End-Use

- 2.2.8 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle production

- 3.2.1.2 Growing demand for commercial vehicles

- 3.2.1.3 Expansion of electric vehicle (EV) market

- 3.2.1.4 Increasing automotive aftermarket demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in raw material prices

- 3.2.2.2 High competition and price pressure

- 3.2.3 Market opportunities

- 3.2.3.1 Development of advanced lightweight spring materials

- 3.2.3.2 Growth in emerging automotive markets

- 3.2.3.3 Expansion of electric and hybrid vehicles

- 3.2.3.4 Strategic collaborations and OEM partnerships

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Transport Canada

- 3.4.1.3 U.S. Environmental Protection Agency (EPA)

- 3.4.1.4 California Air Resources Board (CARB)

- 3.4.1.5 SAE International

- 3.4.2 Europe

- 3.4.2.1 European Commission

- 3.4.2.2 United Nations Economic Commission for Europe (UNECE)

- 3.4.2.3 European Automobile Manufacturers’ Association (ACEA)

- 3.4.2.4 European Committee for Standardization (CEN)

- 3.4.2.5 Kraftfahrt-Bundesamt (KBA)

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Industry and Information Technology (MIIT), China

- 3.4.3.2 China Automotive Technology and Research Center (CATARC)

- 3.4.3.3 Automotive Research Association of India (ARAI)

- 3.4.3.4 Korea Transportation Safety Authority (KOTSA)

- 3.4.4 Latin America

- 3.4.4.1 National Traffic Secretariat (SENATRAN)

- 3.4.4.2 INMETRO

- 3.4.4.3 Ministry of Infrastructure and Transport

- 3.4.4.4 Mexican Official Standards (NOM)

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Cooperation Council Standardization Organization (GSO)

- 3.4.5.2 Emirates Authority for Standardization & Metrology (ESMA)

- 3.4.5.3 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 High-strength alloy steel springs

- 3.7.1.2 Lightweight composite leaf springs

- 3.7.1.3 Air spring integration in vehicles

- 3.7.2 Emerging technologies

- 3.7.2.1 Carbon fiber reinforced composite springs

- 3.7.2.2 Nano-coating for enhanced fatigue and corrosion resistance

- 3.7.1 Current technological trends

- 3.8 Production statistics

- 3.8.1 Production hubs

- 3.8.2 Consumption hubs

- 3.8.3 Export and import

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact

- 3.11.1 Environmental impact assessment

- 3.11.2 Social impact & community benefits

- 3.11.3 Governance & corporate responsibility

- 3.11.4 Sustainable finance & investment trends

- 3.12 Product Lifecycle & Replacement Cycle Analysis

- 3.12.1 Average lifespan by spring type and vehicle segment

- 3.12.2 Failure modes and common wear patterns

- 3.12.3 Vehicle age distribution and aftermarket demand correlation

- 3.12.4 Impact of vehicle electrification on replacement cycles

- 3.12.5 Seasonal demand variations and stocking patterns

- 3.13 Vehicle electrification impact analysis

- 3.13.1 Weight distribution changes in EVs and spring design implications

- 3.13.2 Battery pack weight compensation requirements

- 3.13.3 Regenerative braking impact on suspension spring specifications

- 3.13.4 EV-specific spring durability and fatigue considerations

- 3.14 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 Coil springs

- 5.3 Leaf springs

- 5.4 Torsion springs

- 5.5 Gas springs

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Steel springs

- 6.3 Composite springs

- 6.4 Plastic springs

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Load Capacity, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 Light-duty springs

- 7.3 Medium-duty springs

- 7.4 Heavy-duty springs

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 LCV

- 8.3.2 MCV

- 8.3.3 HCV

- 8.4 Two wheelers

Chapter 9 Market Estimates & Forecast, By Powertrain, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 ICE

- 9.3 Electric & hybrid

- 9.3.1 BEV

- 9.3.2 HEV

- 9.3.3 PHEV

- 9.3.4 FCEV

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 Suspension system

- 10.3 Engine valves

- 10.4 Clutch assemblies

- 10.5 Transmission system

- 10.6 Others

Chapter 11 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Thousand Units)

- 11.1 Key trends

- 11.2 OEM

- 11.3 Aftermarket

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Czech Republic

- 12.3.7 Belgium

- 12.3.8 Russia

- 12.3.9 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Singapore

- 12.4.7 Malaysia

- 12.4.8 Indonesia

- 12.4.9 Vietnam

- 12.4.10 Thailand

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Colombia

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global players

- 13.1.1 NHK Spring

- 13.1.2 Mubea

- 13.1.3 Sogefi

- 13.1.4 Rassini

- 13.1.5 GKN Automotive

- 13.1.6 Mitsubishi Steel

- 13.1.7 ZF Friedrichshafen

- 13.1.8 Thyssenkrupp

- 13.1.9 Lesjofors

- 13.2 Regional players

- 13.2.1 UNI AUTO

- 13.2.2 Kilen Springs

- 13.2.3 Olgun Celik

- 13.2.4 Clifford Springs

- 13.2.5 Soni Auto & Allied Industries

- 13.2.6 Emco Industries

- 13.2.7 Stanley Spring

- 13.3 Emerging players

- 13.3.1 Hendrickson

- 13.3.2 Auto Steels

- 13.3.3 Vikrant Auto

- 13.3.4 Protopower Springs