|

시장보고서

상품코드

1982338

기계 제어 시스템 시장의 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)Machine Control Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

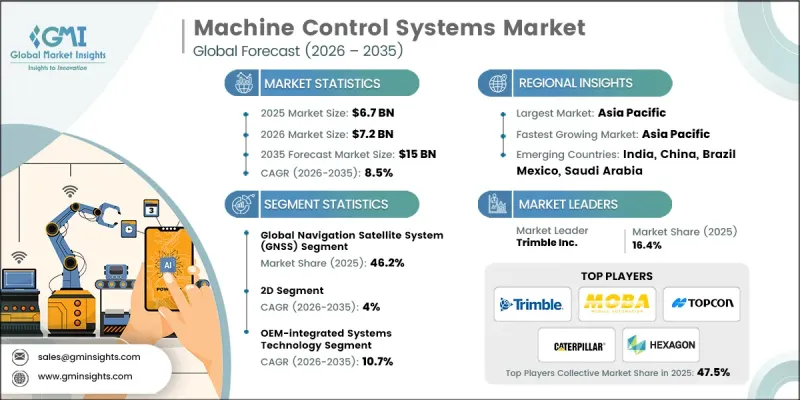

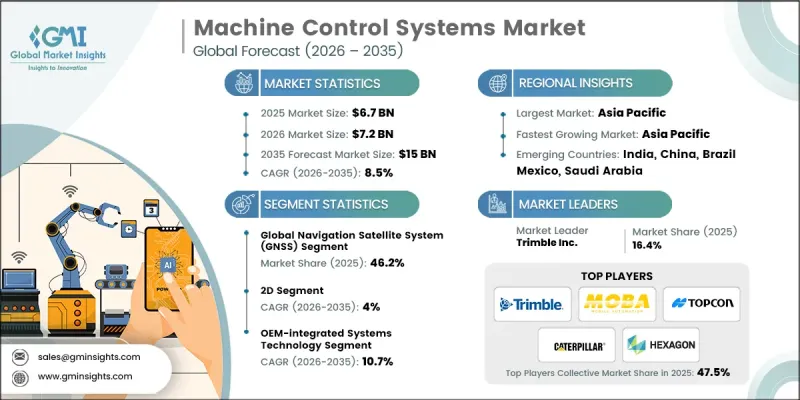

세계의 기계 제어 시스템 시장은 2025년 67억 달러로 평가되었고 CAGR은 8.5%를 나타낼 것으로 보이며, 2035년까지 150억 달러에 이를 것으로 추정됩니다.

시장 확대는 대규모 인프라 프로젝트, 운영 효율성에 대한 수요 증가, 그리고 자동화 및 정밀 기술의 도입 확대에 힘입고 있습니다. 원천 제조업체(OEM)들은 첨단 기계 제어 시스템을 신규 기계에 점진적으로 통합하고 있어, 공장 출고 시 사전 설치된 솔루션에 대한 수요를 촉진하고 있습니다. 시장 내 기업들은 이러한 추세를 활용하여 장비 제조업체와 파트너십을 구축함으로써 성능을 최적화하고 애프터마켓 판매에 대한 의존도를 낮추고 있습니다. 또한 이 분야는 건설, 광업 및 농업 분야 전반에서 정밀도와 효율성을 높이기 위해 3D 기계 제어 기술로 전환되는 추세를 보이고 있습니다. GNSS, 레이저 및 센서 기반 안내 시스템의 도입이 증가함에 따라 시공업체들은 자재 낭비를 최소화하고, 생산성을 향상시키며, 프로젝트 완료 일정을 효율화할 수 있게 되었으며, 이로 인해 기계 제어 시스템은 현대 운영에 없어서는 안 될 필수 요소가 되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시장 규모 | 67억 달러 |

| 예측 금액 | 150억 달러 |

| CAGR | 8.5% |

센서 부문은 실시간 모니터링, 자동 항법 및 예측 유지보수에 대한 수요 증가로 인해 2026년부터 2035년까지 연평균 성장률(CAGR) 10.1%로 성장할 것으로 예상됩니다. 관성 측정 장치(IMU), 레이저 센서 및 경사 센서를 포함한 첨단 센서는 정확도를 높이고, 사람의 개입을 줄이며, 성능을 최적화합니다. 특히 건설, 광업 및 정밀 농업 분야에서 기존 장비 개조 시스템과 신규 기계 모두에 걸쳐 도입이 증가하고 있습니다.

3D 부문은 평탄화, 굴착 및 토목 작업에 대해 다축 실시간 안내 기능을 제공한다는 장점에 힘입어 2025년 시장 점유율 62.2%를 차지했습니다. GNSS, 레이저 및 센서 기술과의 통합은 정밀한 작업을 보장하고 자재 낭비를 줄이며 생산성을 향상시킵니다. OEM 업체들의 3D 솔루션 채택은 건설, 광업 및 농업 부문 전반에서 이 부문의 선도적 위치를 공고히 하고 있습니다.

2025년 북미의 기계 제어 시스템 시장은 29.8%의 점유율을 차지했습니다. 건설 및 광업 분야에서 자동화 및 정밀 기술의 높은 도입률이 지역 성장을 주도하고 있습니다. 건설업체들은 생산성을 높이고 운영 비용을 절감하기 위해 2D/3D 안내, GNSS 및 센서 시스템에 의존하고 있습니다. 도로, 고속도로 및 도시 프로젝트의 인프라 업그레이드는 첨단 기계 제어 솔루션에 대한 수요를 더욱 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 자동화 및 정밀 기술의 채택 확대

- 인프라 확충 및 대규모 건설 프로젝트

- 운영 비용 절감에 대한 관심 증가

- 숙련된 기계 조작 인력 부족

- 신규 기계에 대한 OEM의 기계 제어 시스템 통합 증가

- 업계의 잠재적 위험 및 과제

- 높은 초기 투자 및 설치 비용

- 소규모 프로젝트 및 개발도상국에서의 제한적인 도입

- 시장 기회

- 구형 기계용 개조/애프터마켓 솔루션 개발

- 예측 기계 제어를 위한 AI 및 머신러닝의 발전

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신의 동향

- 현재의 기술 동향

- 신흥 기술

- 신흥 비즈니스 모델

- 규정 준수 요건

- 지정학적 및 무역의 동향

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 시장 집중도 분석

- 주요 기업의 경쟁 벤치마킹

- 재무실적의 비교

- 매출액

- 이익률

- 연구개발

- 제품 포트폴리오 비교

- 제품 라인의 폭

- 기술

- 혁신

- 지역 입지 비교

- 세계의 입지 분석

- 서비스 네트워크 커버 범위

- 지역별 시장 침투율

- 경쟁 포지셔닝 매트릭스

- 선도 기업

- 도전 기업

- 팔로워

- 틈새 기업

- 재무실적의 비교

- 주요 발전

- 합병 및 인수

- 파트너십 및 제휴

- 기술적 진보

- 사업 확대 및 투자 전략

- 디지털 전환의 대처

- 신흥 및 스타트업 경쟁 기업의 동향

제5장 시장 추계 및 예측 : 컴포넌트 유형별(2022-2035년)

- 글로벌 항법 위성 시스템(GNSS)

- 총 스테이션

- 레이저 시스템

- 센서

- 제어 하드웨어

제6장 시장 추계 및 예측 : 시스템 치수별(2022-2035년)

- 2D

- 3D

제7장 시장 추계 및 예측 : 통합 형태별(2022-2035년)

- OEM 통합 시스템

- 개조/애프터마켓 시스템

제8장 시장 추계 및 예측 : 장비 유형별(2022-2035년)

- 굴삭기

- 그레이더

- 불도저

- 로더

- 포장 장비

- 체결 장비

- 기타

제9장 시장 추계 및 예측 : 최종 이용 산업별(2022-2035년)

- 건설

- 광업

- 농업

- 석유 및 가스

- 기타

제10장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계 주요 기업

- Trimble Inc.

- Topcon

- Hexagon AB

- MOBA Mobile Automation AG

- Caterpillar Inc.

- 지역별 주요 기업

- AB Volvo

- ANDRITZ

- CASE Construction Equipment

- Doosan Corporation

- Dynamic Measurement &Control Solutions

- Hemisphere GNSS, Inc.

- iDig System

- Komatsu

- Leica Geosystems AG

- Novatron

- SATEL USA

- Shanghai Huace Navigation Technology Ltd.

- Unicontrol ApS

The Global Machine Control Systems Market was valued at USD 6.7 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 15 billion by 2035.

Market expansion is driven by large-scale infrastructure projects, rising demand for operational efficiency, and increasing adoption of automation and precision technologies. Original equipment manufacturers (OEMs) are progressively integrating advanced machine control systems into new machinery, fueling demand for factory-installed solutions. Companies in the market are leveraging this trend to establish partnerships with equipment manufacturers, ensuring optimized performance and reducing reliance on aftermarket sales. The sector is also witnessing a shift toward 3D machine control technologies to enhance precision and efficiency across construction, mining, and agricultural applications. Increased adoption of GNSS, laser, and sensor-enabled guidance systems is enabling contractors to minimize material waste, improve productivity, and streamline project completion timelines, making machine control systems an indispensable part of modern operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.7 Billion |

| Forecast Value | $15 Billion |

| CAGR | 8.5% |

The sensors segment is expected to grow at a CAGR of 10.1% during 2026-2035, owing to the rising demand for real-time monitoring, automated navigation, and predictive maintenance. Advanced sensors, including inertial measurement units, laser sensors, and tilt sensors, enhance accuracy, reduce human intervention, and optimize performance. Deployment is increasing across both retrofit systems and new machinery, particularly in construction, mining, and precision agriculture.

The 3D segment accounted for 62.2% share in 2025, driven by its ability to provide real-time guidance across multiple axes for grading, excavation, and earthmoving tasks. Integration with GNSS, laser, and sensor technologies ensures precise operations, reduces material waste, and enhances productivity. OEM adoption of 3D solutions reinforces its leading position across construction, mining, and agricultural sectors.

North America Machine Control Systems Market held 29.8% share in 2025. High adoption of automation and precision technologies in construction and mining is driving regional growth. Contractors rely on 2D/3D guidance, GNSS, and sensor systems to improve productivity and reduce operational costs. Infrastructure upgrades in roads, highways, and urban projects further support demand for advanced machine control solutions.

Prominent players operating in the Global Machine Control Systems Market include Trimble Inc., Caterpillar, Komatsu, Hexagon AB, Leica Geosystems AG, Topcon, AB Volvo, DOOSAN Corporation, ANDRITZ, iDig System, MOBA Mobile Automation AG, Dynamic Measurement & Control Solutions, Novatron, SATEL USA, and Shanghai Huace Navigation Technology Ltd. Companies in the Global Machine Control Systems Market are strengthening their position by focusing on technological innovation, strategic partnerships, and market expansion. Key strategies include integrating advanced GNSS, 3D guidance, and sensor technologies into OEM machinery to ensure seamless factory-installed solutions. Firms are investing in software and analytics capabilities to offer predictive maintenance, real-time monitoring, and automation solutions. Collaborations with construction, mining, and agricultural contractors allow companies to tailor solutions to operational needs and secure long-term contracts. Expanding into emerging regions and leveraging retrofit system offerings enables access to untapped markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Component type trends

- 2.2.2 System dimension trends

- 2.2.3 Integration trends

- 2.2.4 Equipment type trends

- 2.2.5 End-use industry trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of automation and precision technologies

- 3.2.1.2 Expansion of infrastructure and large-scale construction projects

- 3.2.1.3 Growing focus on reducing operational costs

- 3.2.1.4 Shortage of skilled machine operators

- 3.2.1.5 Increasing integration of machine control systems by OEMs in new equipment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment and installation costs

- 3.2.2.2 Limited adoption in small-scale projects and developing regions

- 3.2.3 Market opportunities

- 3.2.3.1 Development of retrofit/aftermarket solutions for older machinery

- 3.2.3.2 Advancements in AI and machine learning for predictive machine control

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Component Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Global Navigation Satellite System (GNSS)

- 5.3 Total stations

- 5.4 Laser systems

- 5.5 Sensors

- 5.6 Control hardware

Chapter 6 Market Estimates and Forecast, By System Dimension, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 2D

- 6.3 3D

Chapter 7 Market Estimates and Forecast, By Integration, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 OEM-integrated systems

- 7.3 Retrofit/aftermarket systems

Chapter 8 Market Estimates and Forecast, By Equipment Type, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Excavators

- 8.3 Graders

- 8.4 Dozers

- 8.5 Loaders

- 8.6 Paving equipment

- 8.7 Compaction equipment

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 Construction

- 9.3 Mining

- 9.4 Agriculture

- 9.5 Oil & gas

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Trimble Inc.

- 11.1.2 Topcon

- 11.1.3 Hexagon AB

- 11.1.4 MOBA Mobile Automation AG

- 11.1.5 Caterpillar Inc.

- 11.2 Regional key players

- 11.2.1 AB Volvo

- 11.2.2 ANDRITZ

- 11.2.3 CASE Construction Equipment

- 11.2.4 Doosan Corporation

- 11.2.5 Dynamic Measurement & Control Solutions

- 11.2.6 Hemisphere GNSS, Inc.

- 11.2.7 iDig System

- 11.2.8 Komatsu

- 11.2.9 Leica Geosystems AG

- 11.2.10 Novatron

- 11.2.11 SATEL USA

- 11.2.12 Shanghai Huace Navigation Technology Ltd.

- 11.2.13 Unicontrol ApS