|

시장보고서

상품코드

1982345

산업용 히트펌프 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Industrial Heat Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

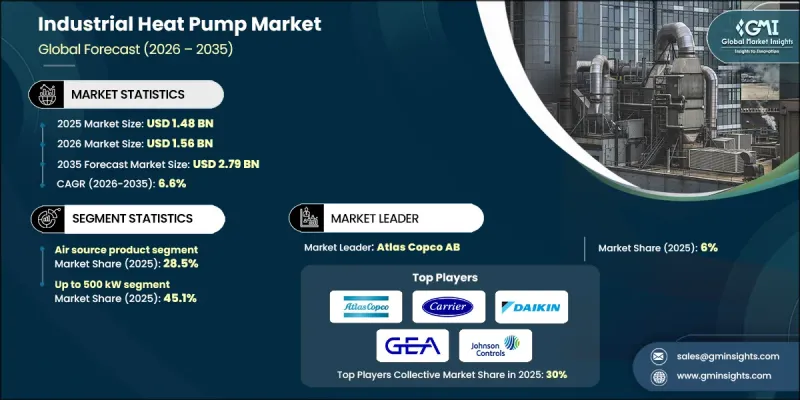

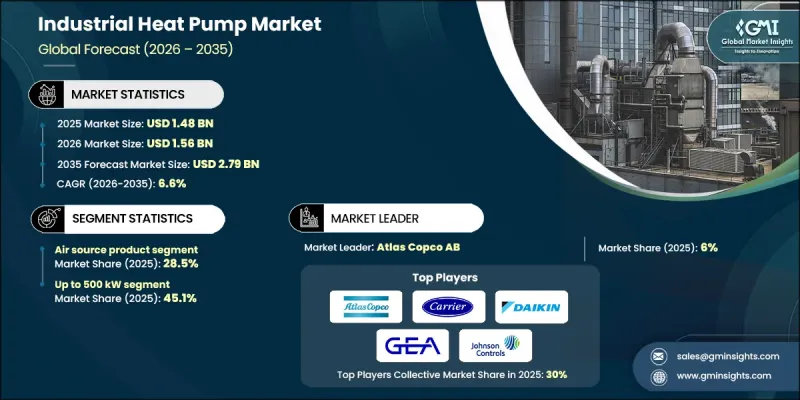

세계의 산업용 히트펌프 시장은 2025년 14억 8,000만 달러로 평가되었으며 CAGR 6.6%로 성장해 2035년까지 27억 9,000만 달러에 이를 것으로 추정됩니다.

환경문제에 대한 관심 증가와 산업활동에서 이산화탄소 배출 감축에 대한 대처의 강화가 에너지 효율이 높은 기술에 대한 수요를 뒷받침하고 있습니다. 산업용 히트펌프는 저온의 폐열을 회수 및 재이용하고 효율성과 지속가능성 모두를 높이기 위한 중요한 솔루션으로 등장해 왔습니다. 화석연료에 대한 의존도 감소를 선호하는 산업이 증가함에 따라 이러한 시스템의 도입은 가속화되고 있습니다. 지원 규제 정책 외에도 에너지 비용 상승과 지속가능성 목표에 대한 적합성을 추구하는 압력이 증가함에 따라 산업의 열 에너지 관리 방법에 변화가 있습니다. 산업 플랜트 전체의 효율적인 냉난방 요구에 더하여, 구식 시스템의 단계적 폐지에 대한 관심 증가가 시장의 기세를 뒷받침하고 있습니다. 산업 관계자는 운영 비용을 줄이면서 에너지 성능을 향상시키는 히트펌프의 가능성을 인식하고 있습니다. 특히 신흥국의 청정기술과 스마트 인프라에 대한 투자 증가와 함께 이 시장은 앞으로 수년간 강력한 확대를 이룰 것으로 전망되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 규모 | 14억 8,000만 달러 |

| 예측 금액 | 27억 9,000만 달러 |

| CAGR | 6.6% |

2025년 시점에서 공기 열원 히트펌프 부문은 28.5%의 점유율을 차지했습니다. 산업용 응용 분야에서 난방, 냉방 및 온수의 효율적인 솔루션에 대한 수요 증가와 더불어 탄소 배출량 감소에 대한 관심 증가는 업계 전망을 더욱 견고하게 만들 것으로 예측됩니다. 히트펌프 컴프레서나 냉매의 개량에 의한 종합 효율의 향상 등, 구성 부품의 기술이 끊임없이 진보하고 있는 것이 도입을 가속시키고 있습니다. 게다가 설치의 용이성, 운영상의 다양성, 비용 효율성 및 다양한 산업 공정에 대한 광범위한 적용성은 공기원 히트펌프 시장의 성장을 더욱 강화하고 있습니다.

2025년에는 500kW 이하 부문이 45.1%의 점유율을 차지했고 2035년까지 연평균 복합 성장률(CAGR) 6.5% 이상으로 성장할 것으로 예측되고 있습니다. 산업분야에서는 운용 비용 절감과 탄소 실적 저감을 목적으로 에너지 효율이 높은 냉난방 시스템의 도입이 확대되고 있으며, 제조업, 화학처리업, 식품 및 음료업, 펄프 및 제지업에 대한 수요를 견인하고 있습니다. 특정 산업 요건에 맞는 첨단 히트펌프 기술의 채택이 시장을 재구성하고 있으며, 다양한 분야에서의 급속한 도입이 성장 궤도를 더욱 강화하고 있습니다.

2025년 시점에서 미국 산업용 히트펌프 시장은 75.6%의 점유율을 차지하여 3억 3,960만 달러 시장 규모를 형성했습니다. 북미 시장은 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 7.2%라는 견조한 성장이 예상됩니다. '인플레이션 억제법(IRA)'과 미국 에너지부(DOE)에 의한 대상을 좁힌 조성금 등의 정책에 의해 산업 전기화를 위한 설비투자 장벽이 대폭 줄어들고 있습니다. 에너지 집약형 산업, 특히 식품, 음료 및 펄프 및 제지 산업에서는 노후화된 가스 보일러의 대안과 기업의 ESG 목표 달성을 위한 히트펌프의 도입이 점점 더 진행되고 있습니다. 2026년 기술진보로 캐나다나 미국 북부와 같은 혹독한 환경에서도 가동 가능한 고효율 유닛이 등장해 대상 시장이 확대되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 산업 배출량 억제를 위한 밝은 전망

- 대형 산업용도에 신규 투자 유입

- 각 당국에 의해 뒷받침 되는 규제 프레임워크

- 업계의 잠재적 위험 및 과제

- 고액의 초기 도입 비용

- 특수 합금 공급망의 변동성

- 기회

- 산업 공정의 탈탄소화

- 정부에 의한 인센티브 및 지원 정책

- 성장 촉진요인

- 성장 가능성 분석

- 미래 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품 유형별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 제품별(2022-2035년)

- 공기 열원

- 지중열

- 수원

- 폐쇄 루프 기계식 히트펌프

- 개방 사이클 기계식 증기 압축 히트펌프

- 개방 사이클 기계식 열 압축 히트펌프

- 폐쇄 루프 흡수식 히트펌프

제6장 시장 추계 및 예측 : 용량별(2022-2035년)

- 500 kW 이하

- 500 kW-2 MW

- 2-5 MW

- 5 MW 이상

제7장 시장 추계 및 예측 : 온도별(2022-2035년)

- 80-100°C

- 100-150°C

- 150-200°C

- 200°C 이상

제8장 시장 추계 및 예측 : 용도별(2022-2035년)

- 산업용

- 제지

- 식품 및 음료

- 화학

- 철강

- 기계

- 비금속광물

- 기타 산업

- 지역난방

제9장 시장 추계 및 예측 : 국가별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Armstrong International Inc.

- Atlas Copco AB

- Baker Hughes Company

- Carrier

- Daikin Applied Europe SpA

- Dalrada Climate Technology

- Ecop

- Emerson Electric Co.

- Enerin AS

- GEA Group Aktiengesellschaft

- Hien New Energy Equipment Co., Ltd.

- Johnson Controls

- MAN Energy Solutions

- OCHSNER

- Oilon Group Oy

- Piller Blowers &Compressors GmbH

- Qvantum Energi AB

- Swegon Ltd

- Trane Technologies International Limited

- Turboden SpA

The Global Industrial Heat Pump Market was valued at USD 1.48 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 2.79 billion by 2035.

Rising environmental concerns and increased efforts to cut carbon emissions in industrial operations are pushing the demand for energy-efficient technologies. Industrial heat pumps have emerged as a key solution for capturing and repurposing low-temperature waste heat, enhancing both efficiency and sustainability. As more industries prioritize reducing reliance on fossil fuels, the adoption of these systems is accelerating. Supportive regulatory policies, combined with increasing energy costs and growing pressure to align with sustainability targets, are reshaping how industries manage thermal energy. The need for efficient heating and cooling across industrial plants, along with growing interest in phasing out outdated systems, continues to boost market momentum. Industrial players are recognizing the potential of heat pumps to improve energy performance while cutting operational expenditures. Coupled with rising investments in clean technologies and smart infrastructure, especially across emerging economies, the market is set to witness robust expansion in the years ahead.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.48 Billion |

| Forecast Value | $2.79 Billion |

| CAGR | 6.6% |

The air source heat pump segment held 28.5% share in 2025. Rising demand for efficient solutions in space heating, cooling, and hot water across industrial applications, coupled with the increasing focus on reducing carbon emissions, is expected to strengthen the industry outlook. Continuous advancements in component technologies, including improvements in heat pump compressors and refrigerants to enhance overall efficiency, are accelerating adoption. Additionally, the ease of installation, operational versatility, cost-effectiveness, and wide applicability across various industrial processes are further supporting the growth of the air source heat pump market.

The up to 500 kW segment accounted for 45.1% share in 2025 and is projected to grow at over 6.5% CAGR through 2035. Industrial sectors are increasingly deploying energy-efficient heating and cooling systems to lower operational costs and reduce carbon footprints, driving demand in manufacturing, chemical processing, food & beverage, and pulp & paper industries. The adoption of advanced heat pump technologies tailored to specific industrial requirements is reshaping the market, with rapid implementation across diverse sectors further enhancing the growth trajectory.

U.S. Industrial Heat Pump Market held 75.6% share in 2025, generating USD 339.6 million. North America is expected to grow at a strong CAGR of 7.2% from 2026 to 2035. Policies such as the Inflation Reduction Act (IRA) and targeted Department of Energy (DOE) grants are significantly reducing capital expenditure barriers for industrial electrification. Energy-intensive industries, particularly food & beverage and pulp & paper, are increasingly adopting heat pumps to replace aging gas-fired boilers and meet corporate ESG targets. Technological advances in 2026 have introduced high-efficiency units capable of operating under extreme conditions in Canada and northern U.S., broadening the addressable market.

Key players shaping the competitive landscape of the Global Industrial Heat Pump Market include Turboden S.p.A., Ecop, MAN Energy Solutions, Carrier, Qvantum Energi AB, Oilon Group Oy, Dalrada Climate Technology, Armstrong International Inc., Johnson Controls, Atlas Copco AB, GEA Group Aktiengesellschaft, Hien New Energy Equipment Co., Ltd., Daikin Applied Europe S.p.A., Trane Technologies International Limited, Swegon Ltd, Enerin AS, OCHSNER, Emerson Electric Co., Baker Hughes Company, and Piller Blowers & Compressors GmbH. To strengthen their positioning, companies in the industrial heat pump space are prioritizing strategic investments in product innovation and R&D to offer higher efficiency systems compatible with modern industrial demands. Several players are expanding global manufacturing capabilities and establishing local partnerships to cater to region-specific requirements. Firms are also aligning their portfolios with low-carbon and renewable energy trends, introducing systems capable of integrating with waste heat recovery and hybrid setups.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Countrywise

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 By Power Range

- 2.2.4 Material/Construction

- 2.2.5 End-User

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Positive outlook to curb industrial emission levels

- 3.2.1.2 Influx of new investments across heavy-duty industrial applications

- 3.2.1.3 Encouraging regulatory framework by respective authorities

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Significant initial deployment cost

- 3.2.2.2 Supply Chain Volatility for Specialized Alloys

- 3.2.3 Opportunities

- 3.2.3.1 Decarbonization of industrial processes

- 3.2.3.2 Government incentives and supportive policies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Product Type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Air source

- 5.3 Ground source

- 5.4 Water source

- 5.5 Closed cycle mechanical heat pump

- 5.6 Open cycle mechanical vapor compression heat pump

- 5.7 Open cycle mechanical thermocompression heat pump

- 5.8 Closed cycle absorption heat pump

Chapter 6 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Up to 500 kW

- 6.3 > 500 kW to 2 MW

- 6.4 2 MW - 5 MW

- 6.5 > 5 MW

Chapter 7 Market Estimates and Forecast, By Temperature, 2022 - 2035 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 80 - 100 °C

- 7.3 100 - 150 °C

- 7.4 150 - 200 °C

- 7.5 > 200 °C

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Industrial

- 8.2.1 Paper

- 8.2.2 Food & beverages

- 8.2.3 Chemical

- 8.2.4 Iron & Steel

- 8.2.5 Machinery

- 8.2.6 Non-Metallic minerals

- 8.2.7 Other industries

- 8.3 District heating

Chapter 9 Market Estimates and Forecast, By Country, 2022 - 2035 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Key trends

- 9.3 North America

- 9.3.1 U.S.

- 9.3.2 Canada

- 9.4 Europe

- 9.4.1 Germany

- 9.4.2 UK

- 9.4.3 France

- 9.4.4 Italy

- 9.4.5 Spain

- 9.5 Asia Pacific

- 9.5.1 China

- 9.5.2 Japan

- 9.5.3 India

- 9.5.4 Australia

- 9.5.5 South Korea

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Mexico

- 9.6.3 Argentina

- 9.7 Middle East and Africa

- 9.7.1 South Africa

- 9.7.2 Saudi Arabia

- 9.7.3 UAE

Chapter 10 Company Profiles

- 10.1 Armstrong International Inc.

- 10.2 Atlas Copco AB

- 10.3 Baker Hughes Company

- 10.4 Carrier

- 10.5 Daikin Applied Europe S.p.A.

- 10.6 Dalrada Climate Technology

- 10.7 Ecop

- 10.8 Emerson Electric Co.

- 10.9 Enerin AS

- 10.10 GEA Group Aktiengesellschaft

- 10.11 Hien New Energy Equipment Co., Ltd.

- 10.12 Johnson Controls

- 10.13 MAN Energy Solutions

- 10.14 OCHSNER

- 10.15 Oilon Group Oy

- 10.16 Piller Blowers & Compressors GmbH

- 10.17 Qvantum Energi AB

- 10.18 Swegon Ltd

- 10.19 Trane Technologies International Limited

- 10.20 Turboden S.p.A.