|

시장보고서

상품코드

1982355

우주 로봇 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Space Robotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

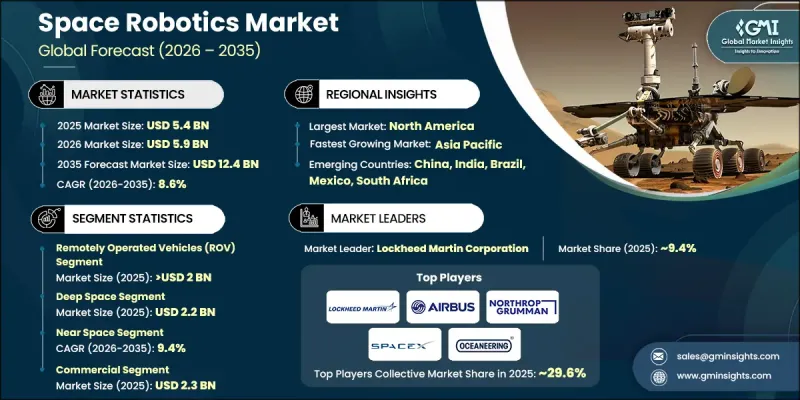

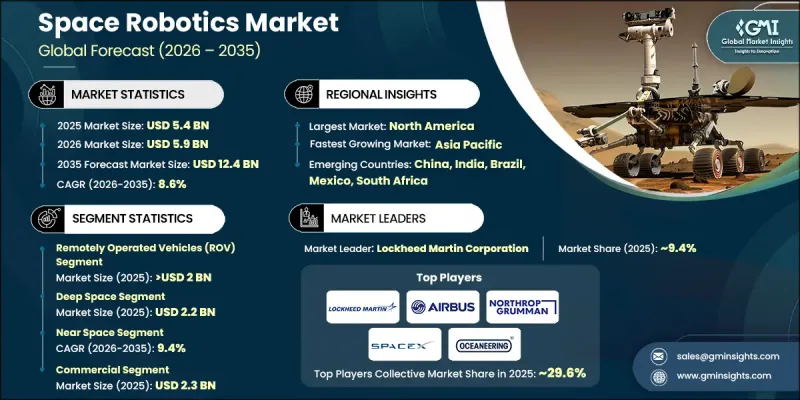

세계의 우주 로봇 시장은 2025년 54억 달러로 평가되었으며 CAGR 8.6%로 성장해 2035년까지 124억 달러에 이를 것으로 추정됩니다.

우주 임무의 복잡성과 규모가 확대됨에 따라 이 분야는 확대되고 있으며, 다양한 지구외 환경에서 작동할 수 있는 첨단 로봇 기술과 자동화 기술에 대한 수요가 탄생하고 있습니다. 우주기관과 민간기업은 심우주에서의 장기 임무를 지원하고, 우주비행사에 대한 의존도를 줄이고 운영 효율성을 향상시키는 로봇 시스템을 개발하고 있습니다. 이러한 시스템은 우주 공간에서의 정비, 조립, 행성 탐사 등 다양한 용도로 설계되어 보다 빈번하고 복잡하고 비용 효율적인 임무를 가능하게 합니다. 우주 프로그램에 로봇 기술을 통합하면 실시간 모니터링, 작업 자동 실행, 인적 자원에 과도한 부담을 주는 임무 지원이 가능합니다. 정부, 연구기관, 민간기업이 일체가 되어 혁신을 추진하고 있으며, 로봇기술이 미래의 우주운용에 있어 매우 중요한 역할을 하는 것을 확실히 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 금액 | 54억 달러 |

| 예측 금액 | 124억 달러 |

| CAGR | 8.6% |

원격조작 차량(ROV) 부문은 우주 탐사, 궤도 점검, 행성 탐사 로버 및 우주 정거장 운영에 중요한 역할을 했기 때문에 2025년에는 20억 달러에 달했습니다. ROV는 위험한 환경과 접근하기 어려운 환경에서 원격 근무을 수행할 수 있는 다목적 플랫폼으로 기능하며, 실시간 제어와 자율 기능을 모두 활용하여 지표 탐사, 샘플 채취 및 궤도 유지보수를 지원합니다.

상업 부문은 위성 전개, 우주 여행, 궤도 제조 및 상업 스테이션에 종사하는 민간 우주 기업의 급속한 확대에 견인되어 2025년에는 23억 달러에 이르렀습니다. 상업 우주 로봇 공학은 위성 관리, 발사 운영, 점검 및 유지보수에 널리 적용되어 확장성이 높고 비용 효율적인 운영을 가능하게 합니다. 강력한 민간 투자, 발사 빈도 증가 및 기술 혁신으로 상업 임무 전반의 채용이 더욱 가속화되고 있습니다.

2025년 북미 우주 로봇 시장은 38.5%의 점유율을 차지했습니다. 이 지역의 성장은 많은 양의 정부 자금, 견조한 우주 탐사 프로그램, 방어 관련 노력 및 우주 인프라에 대한 투자에 의해 지원됩니다. 북미의 정부기관과 기업은 장기적인 프로그램을 활용하여 선진적인 로봇 플랫폼을 개발하고 있으며, 우주 로봇 기술에서 동지역의 리더십을 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 위성 컨스텔레이션 및 심우주 미션 확대

- 자율형 및 AI를 활용한 우주 운용에 대한 수요 증가

- 우주 관광 및 상업 우주 활동의 성장

- 우주 프로그램에서 관민 제휴의 확대

- 궤도 서비스, 우주 쓰레기 제거 및 위성 유지보수의 필요성

- 업계의 잠재적 위험 및 과제

- 높은 개발 비용과 기술적 복잡성

- 가혹하고 예측 불가능한 우주 환경에서의 운영 위험

- 시장 기회

- 우주 미션에 자율형 로봇 시스템 도입 확대

- 궤도상 서비스, 조립 및 제조(ISAM)에 대한 수요 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 가격 전략

- 신흥 비즈니스 모델

- 컴플라이언스 요건

- 지정학적 및 무역 동향

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 주요 기업의 경쟁 벤치마킹

- 재무실적의 비교

- 매출액

- 이익률

- 연구개발

- 제품 포트폴리오 비교

- 제품 라인의 폭

- 기술

- 혁신

- 지역별 전개의 비교

- 세계 전개의 분석

- 서비스 네트워크의 커버율

- 지역별 시장 침투율

- 경쟁 포지셔닝 매트릭스

- 리더

- 챌린저

- 팔로워

- 틈새 기업

- 재무실적의 비교

- 주요 발전, 2022-2025년

- 합병 및 인수

- 파트너십 및 제휴

- 기술적 진보

- 사업 확대 및 투자 전략

- 디지털 전환의 대처

- 신흥/스타트업 경쟁기업의 동향

제5장 시장 추계 및 예측 : 솔루션별(2022-2035년)

- 원격조작 차량(ROV)

- 로버 및 우주선 착륙기

- 우주탐사기

- 기타

- 원격 조작 시스템(RMS)

- 로봇 암 및 매니퓰레이터 시스템

- 그리핑 및 도킹 시스템

- 기타

- 소프트웨어

- 서비스

제6장 시장 추계 및 예측 : 기술별(2022-2035년)

- 원격 탐사

- 자율 시스템

- 원격조작

- 로봇 소프트웨어

- 인공지능(AI) 및 머신러닝(ML)

- 인간-로봇 간 상호작용

제7장 시장 추계 및 예측 : 용도별(2022-2035년)

- 심우주

- 행성 탐사

- 소행성 채굴

- 우주 조사

- 근우주

- 위성운영

- 우주정거장 유지보수

- 궤도 수송

- 기타

- 지상

- 발사 운용

- 지상관제 운용

- 우주 조사시설

제8장 시장 추계 및 예측 : 최종 사용자별(2022-2035년)

- 상업용

- 정부

- 방위

제9장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계기업

- Airbus SE

- ITT Corporation

- Lockheed Martin Corporation

- MAXAR TECHNOLOGIES

- MDA Space

- Northrop Grumman

- SpaceX

- 지역 기업

- Altius Space Machine

- Astrobotic Technology

- Astroscale Holdings Inc.

- Honeybee Robotics

- Intuitive Machines, LLC.

- Ispace

- Made In Space Inc.(Redwire LLC)

- Metecs, LLC.

- Oceaneering International, Inc.

- 지역/틈새 기업

- BluHaptics, Inc.

- Motiv Space Systems, Inc.

- Olis Robotics

The Global Space Robotics Market was valued at USD 5.4 billion in 2025 and is estimated to grow at a CAGR of 8.6% to reach USD 12.4 billion by 2035.

The sector is expanding as the complexity and scope of space missions grow, creating demand for advanced robotic and automation technologies that can operate across diverse extraterrestrial environments. Space agencies and commercial enterprises are developing robotic systems to support long-duration missions in deep space, reduce reliance on astronauts, and enhance operational efficiency. These systems are being designed for multiple applications, including in-space servicing, assembly, and planetary exploration, enabling more frequent, complex, and cost-effective missions. Integration of robotics into space programs allows for real-time monitoring, automated task execution, and mission support that would otherwise strain human resources. Governments, research institutions, and private players are collectively driving innovation, ensuring that robotics plays a pivotal role in the future of space operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.4 Billion |

| Forecast Value | $12.4 Billion |

| CAGR | 8.6% |

The remotely operated vehicles (ROV) segment reached USD 2 billion in 2025, owing to their critical role in space exploration, orbital inspections, planetary rovers, and space station operations. ROVs act as versatile platforms capable of performing remote tasks in hazardous or inaccessible environments, supporting surface exploration, sample collection, and in-orbit maintenance with both real-time control and autonomous capabilities.

The commercial segment reached USD 2.3 billion in 2025, driven by the rapid expansion of private space companies engaged in satellite deployment, space tourism, in-orbit manufacturing, and commercial stations. Commercial space robotics is extensively applied for satellite management, launch operations, inspection, and maintenance, allowing scalable and cost-efficient operations. Strong private investments, increasing launch cadence, and technological innovation further accelerate adoption across commercial missions.

North America Space Robotics Market held a 38.5% share in 2025. The region's growth is fueled by substantial government funding, robust space exploration programs, defense initiatives, and investment in space infrastructure. Agencies and enterprises in North America are leveraging long-term programs to develop advanced robotic platforms, strengthening the region's leadership in space robotics technologies.

Key players operating in the Global Space Robotics Market include Lockheed Martin Corporation, Honeybee Robotics, Astroscale Holdings Inc., Northrop Grumman, Astrobotic Technology, Intuitive Machines LLC, Made In Space Inc. (Redwire LLC), SpaceX, MAXAR TECHNOLOGIES, Airbus SE, Oceaneering International Inc., MDA Space, Altius Space Machine, ITT Corporation, Motiv Space Systems Inc., Olis Robotics, BluHaptics Inc., Ispace, and Metecs LLC. Companies in the Global Space Robotics Market are adopting several strategies to solidify their market presence and expand their global footprint. Leading players are investing in research and development to design autonomous and semi-autonomous robotic systems for deep-space exploration, orbital servicing, and planetary operations. Strategic collaborations with space agencies, commercial launch providers, and satellite operators enable deployment at scale. Firms are also focusing on modular, reconfigurable robotic platforms to support multiple mission profiles and reduce operational costs. Technological innovation in AI, machine learning, sensors, and teleoperation is a priority to enhance precision, reliability, and safety.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.8 Mathematical impact of growth parameters on forecast

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Solution trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 End User trends

- 2.3 TAM analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of Satellite Constellations and Deep-Space Missions

- 3.2.1.2 Rising Demand for Autonomous and AI-Enabled Space Operations

- 3.2.1.3 Growth in Space Tourism and Commercial Space Activities

- 3.2.1.4 Increasing Public-Private Sector Collaboration in Space Programs

- 3.2.1.5 Need for In-Orbit Servicing, Debris Removal, and Satellite Maintenance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Development Costs and Technical Complexity

- 3.2.2.2 Operational Risks in Harsh and Unpredictable Space Environments

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of autonomous robotic systems for space missions

- 3.2.3.2 Growing demand for in-orbit servicing, assembly, and manufacturing (ISAM)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Solution, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Remotely Operated Vehicles (ROV)

- 5.2.1 Rovers/Spacecraft Landers

- 5.2.2 Space Probes

- 5.2.3 Others

- 5.3 Remote Manipulator System (RMS)

- 5.3.1 Robotic Arms/Manipulator Systems

- 5.3.2 Gripping & Docking Systems

- 5.3.3 Others

- 5.4 Software

- 5.5 Services

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Remote Sensing

- 6.3 Autonomous Systems

- 6.4 Teleoperation

- 6.5 Robotic Software

- 6.6 Artificial Intelligence (AI) and Machine Learning (ML)

- 6.7 Human-Robot Interaction

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Deep Space

- 7.2.1 Planetary Exploration

- 7.2.2 Asteroid Mining

- 7.2.3 Space Research

- 7.3 Near Space

- 7.3.1 Satellite Operations

- 7.3.2 Space Station Maintenance

- 7.3.3 Orbital Transportation

- 7.3.4 Others

- 7.4 Ground

- 7.4.1 Launch Operations

- 7.4.2 Ground Control Operations

- 7.4.3 Space Research Labs

Chapter 8 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Government

- 8.4 Defence

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Airbus SE

- 10.1.2 ITT Corporation

- 10.1.3 Lockheed Martin Corporation

- 10.1.4 MAXAR TECHNOLOGIES

- 10.1.5 MDA Space

- 10.1.6 Northrop Grumman

- 10.1.7 SpaceX

- 10.2 Regional Players

- 10.2.1 Altius Space Machine

- 10.2.2 Astrobotic Technology

- 10.2.3 Astroscale Holdings Inc.

- 10.2.4 Honeybee Robotics

- 10.2.5 Intuitive Machines, LLC.

- 10.2.6 Ispace

- 10.2.7 Made In Space Inc. (Redwire LLC)

- 10.2.8 Metecs, LLC.

- 10.2.9 Oceaneering International, Inc.

- 10.3 Local / Niche Players

- 10.3.1 BluHaptics, Inc.

- 10.3.2 Motiv Space Systems, Inc.

- 10.3.3 Olis Robotics