|

시장보고서

상품코드

1982356

원격 조종 잠수정 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Remote Operated Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

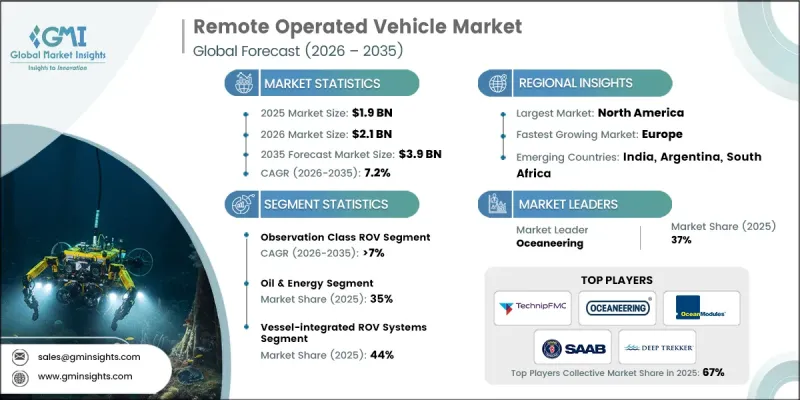

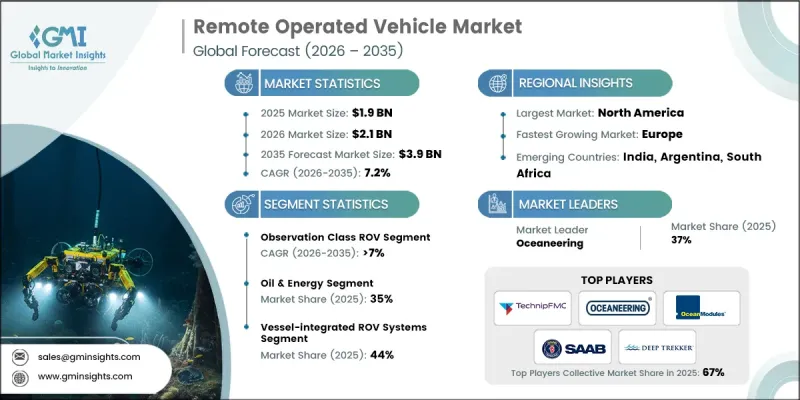

세계의 원격 조종 잠수정(ROV) 시장은 2025년 19억 달러로 평가되었으며 CAGR 7.2%로 성장해 2035년까지 39억 달러에 이를 것으로 추정됩니다.

첨단 해양기술에 대한 연구기관과 정부기관으로부터의 재정 지원의 확대가 시장의 성장을 대폭 가속화하고 있습니다. 원격 조종 잠수정(ROV)는 고해상도 이미지, 고급 센서, 인간의 도달범위를 넘은 극심해에서의 정밀한 조종성을 필요로 하는 복잡한 해저 임무에 점점 도입되고 있습니다. 이러한 시스템은 해양과학, 해양학 평가, 생물다양성 분석 및 기후 관련 연구를 지원하는 환경정보 수집에 매우 중요한 역할을 합니다. 지속가능한 해양관리와 지구 규모 환경 모니터링 프로그램에 대한 관심이 높아지면서 도입을 더욱 강화하고 있습니다. 이와 병행하여, 석유, 가스 및 재생에너지 분야에서 해양 인프라의 확대는 신뢰할 수 있는 수중 로봇의 지속적인 수요를 창출하고 있습니다. ROV는 작업의 안전성을 높이고 비용 효율성을 향상시키고 위험한 해저 환경에 대한 인간의 노출을 최소화합니다. 실시간 데이터 전송, 정확한 조작 능력 및 원격 조작을 통한 개입이 가능하므로 지속적인 수중 작업을 지원합니다. 방위 및 해상보안 분야에서의 이용 확대는 세계의 원격 조종 차량(ROV) 산업의 장기적인 성장 궤도를 더욱 견고하게 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 금액 | 19억 달러 |

| 예측 금액 | 39억 달러 |

| CAGR | 7.2% |

원격 조종 잠수정(ROV) 시장의 업계 관계자는 경쟁 우위를 유지하기 위해 신제품의 도입, 인수, 전략적 제휴 등 비유기적 성장책을 적극적으로 추진하고 있습니다. 해상 에너지에 대한 투자 확대로 해저 검사, 개입, 건설 서비스에 대한 수요가 크게 증가하고 있습니다. ROV 시스템은 가혹한 수중 환경에 안전한 액세스를 제공하는 동시에 작업의 정확성과 비용 관리를 보장합니다. 가동 중지 시간을 최소화하면서 기술적으로 어려운 작업을 수행할 수 있는 능력은 끊임없는 해저 작업에 의존하는 에너지 관련 산업 전반에서 ROV의 가치 제안을 강화하고 있습니다. 또한, 국방 분야에서 현대화 노력의 확대는 해상 작전에서 고급 원격 조작 시스템의 통합 촉진에 기여합니다.

관측용 ROV 부문은 2025년에 35%의 점유율을 차지했고 2026년부터 2035년까지 CAGR 7%를 나타낼 것으로 예측됩니다. 이러한 컴팩트한 시스템은 합리적인 가격, 도입 용이성, 높은 기동성으로 인해 다양한 산업에서 일상적인 수중 평가에 널리 채택되었습니다. 특히 지속적인 모니터링이 필요한 수몰 인프라 및 중요 자산의 육안 검사에 적합합니다. 규제감독의 강화와 자산 보전요건 증가로 고화질의 시각 데이터 솔루션에 대한 수요가 가속화되고 있어 세계 관측용 ROV 카테고리의 지속적인 확대를 지원하고 있습니다.

석유 및 에너지 분야는 2025년에 35%의 점유율을 차지했고, 2026년부터 2035년까지 CAGR 6.5%를 나타낼 것으로 예측됩니다. 보다 깊고 기술적으로 복잡한 저류층에서 지속적인 해양 탄화수소 탐사 활동이 ROV 도입에 크게 기여하고 있습니다. 사업자는 드릴링 작업 지원, 장비 점검, 해저 구성요소 설치 및 파이프라인 인프라 유지관리를 위한 고급 시스템에 의존합니다. 이러한 차량은 가혹한 해저 환경에서 업무 연속성을 지원하고 안전 기준을 강화하며 탄화수소의 전체 회수 성능을 향상시키는 효율적이고 정밀한 개입 능력을 제공합니다.

미국의 원격 조종 잠수정(ROV) 시장은 71%의 점유율을 차지하고, 2025년에는 5억 2,800만 달러 시장 규모를 기록했습니다. 이 나라의 고급 작업 ROV 시스템에 대한 수요를 견인하는 주요 요인은 지속적인 해양 에너지 생산 활동입니다. 해양 자산의 지속적인 유지 보수, 심해 개발 및 해저 인프라 업그레이드에는 고성능 원격 운영 기술이 필수적입니다. 지속적인 모니터링과 시스템 업그레이드를 통해 노후화된 해양시설의 가동 수명을 연장하는 노력은 플릿의 안정적인 가동과 장기적인 시장의 안정을 더욱 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 해양 석유 및 가스 탐사 확대

- 해상풍력발전의 급속한 성장

- 확대하는 방위 및 해군 현대화 프로그램

- 해저 통신 및 전력 케이블 인프라의 성장

- 로봇 공학 및 AI 통합의 기술적 진보

- 업계의 잠재적 위험 및 과제

- 높은 자본 비용 및 운영 비용

- 숙련 오퍼레이터 부족

- 가혹한 해양 조업환경

- 해양 에너지 사이클에 대한 의존도

- 시장 기회

- 심해 광업 활동 확대

- 해양조사 및 환경 모니터링 확대

- 수산 양식 및 해양 양식 사업의 확대

- 자율형 수중 차량(AUV)과의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국 선박 부수적 배출법

- 미국 해안 경비대의 안전 규제

- 안전 및 환경 집행국(BSEE)의 해양 규칙

- 유럽

- EU 해양안전지령

- CE 마킹 및 기계 지령 준수

- 각국 해사당국의 차이점

- 해상 재생에너지 규제

- 다이버의 안전 및 해저 작업에 관한 규제

- 아시아태평양

- 중국의 해양 규제 프레임워크

- 인도의 해양 규제 환경

- ASEAN의 해사 조화를 위한 대처

- 일본의 해사 및 해양 프레임워크

- 호주 및 한국의 해상 컴플라이언스 기준

- 라틴아메리카

- 브라질의 해양 규제 프레임워크

- 멕시코의 해양 안전 및 환경 규제

- 지역별 해양 개발 규제 조화를 위한 노력

- 중동 및 아프리카

- GCC의 해양 규제 프레임워크

- 남아프리카 해사 안전 규제

- 서아프리카 및 홍해의 해양 개발 규제

- 북미

- 주요 시장 동향과 변화

- 미래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출입

- 비용 내역 분석

- 특허 분석

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국에 관한 고찰

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카(MEA)

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 유형별(2022-2035년)

- 작업용 ROV

- 경작업용 ROV

- 관측용 ROV

- 마이크로 및 미니 ROV

제6장 시장 추계 및 예측 : 용도별(2022-2035년)

- 수산 양식

- 상업 및 구조 다이빙

- 지자체 인프라

- 군사

- 석유 및 에너지

- 기타

제7장 시장 추계 및 예측 : 심도별(2022-2035년)

- 천해 ROV(1,000 msw 이하)

- 중층 ROV(1,000-3,000 msw)

- 심해 ROV(3,000-6,000 msw)

- 초심해 ROV(6,000 msw 이상)

제8장 시장 추계 및 예측 : 시스템 아키텍처별(2022-2035년)

- 선박 일체형 ROV 시스템

- 모듈식 컨테이너형 ROV 시스템

- 완전 컨테이너형 ROV 시스템

제9장 시장 추계 및 예측 : 지역별, 2021-2034

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 네덜란드

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 동남아시아

- 라틴아메리카

- 브라질

- 아르헨티나

- 멕시코

- 중동 및 아프리카(MEA)

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제10장 기업 프로파일

- 세계 기업

- DeepOcean

- DOF Subsea

- Forum Energy Technologies

- Fugro

- Kongsberg Maritime

- Oceaneering International

- Saab Seaeye

- Saipem

- SLB(Schlumberger)

- TechnipFMC

- 지역 기업

- ROVOP

- AC-CESS Co UK

- Anritsu Corp

- Deep Ocean Engineering

- Deep Ocean Search

- SEAMOR Marine

- Seatronics

- 신흥기업

- Deep Trekker

- Rovtech

- VideoRay

The Global Remote Operated Vehicle Market was valued at USD 1.9 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 3.9 billion by 2035.

Growing financial support from research institutions and government bodies for advanced marine technologies is significantly accelerating market growth. Remote operated vehicles are increasingly deployed for complex subsea missions that require high-resolution imaging, advanced sensors, and precise maneuverability at extreme depths beyond human reach. These systems play a critical role in collecting environmental intelligence that supports marine science, oceanographic assessments, biodiversity analysis, and climate-related studies. The rising emphasis on sustainable ocean management and global environmental monitoring programs continues to strengthen adoption. In parallel, expanding offshore infrastructure across oil, gas, and renewable energy sectors is creating sustained demand for dependable underwater robotics. ROVs enhance operational safety, improve cost efficiency, and minimize human exposure to hazardous subsea environments. Their ability to deliver real-time data transmission, accurate manipulation capabilities, and remote-controlled intervention supports continuous underwater operations. Increased utilization across defense and maritime security applications further reinforces the long-term expansion trajectory of the global remote operated vehicle industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.9 Billion |

| Forecast Value | $3.9 Billion |

| CAGR | 7.2% |

Industry participants in the remote operated vehicle market are actively implementing inorganic growth initiatives, including product introductions, acquisitions, and strategic collaborations, to maintain competitive positioning. Rising offshore energy investments are driving substantial demand for subsea inspection, intervention, and construction services. ROV systems provide safe access to challenging underwater environments while ensuring operational precision and cost control. Their capability to execute technically demanding tasks with minimal downtime has strengthened their value proposition across energy-driven industries that rely on uninterrupted subsea performance. Additionally, expanding defense modernization efforts are contributing to greater integration of advanced remotely operated systems within maritime operations.

The observation class ROV segment accounted for 35% share in 2025 and is anticipated to grow at a CAGR of 7% from 2026 to 2035. These compact systems are widely adopted for routine underwater assessments across multiple industries due to their affordability, ease of deployment, and high maneuverability. They are particularly suited for visual inspections of submerged infrastructure and critical assets requiring consistent monitoring. Increasing regulatory oversight and asset integrity requirements are accelerating demand for high-definition visual data solutions, supporting sustained expansion of the observation class category worldwide.

The oil & energy segment held a 35% share in 2025 and is forecast to grow at a CAGR of 6.5% between 2026 and 2035. Continued offshore hydrocarbon exploration activities in deeper and more technically complex reservoirs are significantly contributing to ROV deployment. Operators rely on advanced systems to assist drilling operations, perform equipment inspections, install subsea components, and maintain pipeline infrastructure. These vehicles provide efficient, high-precision intervention capabilities that support operational continuity, enhance safety standards, and improve overall hydrocarbon recovery performance in demanding subsea conditions.

United States Remote Operated Vehicle Market held 71% share, generating USD 528 million in 2025. Sustained offshore energy production activities are a major driver of demand for advanced work-class ROV systems in the country. Ongoing maintenance of offshore assets, deepwater developments, and subsea infrastructure upgrades requires highly capable remotely operated technologies. Efforts to extend the operational life of mature offshore facilities through continuous monitoring and system upgrades further support steady fleet utilization and long-term market stability.

Key companies operating in the Global Remote Operated Vehicle Market include Forum Energy Technologies, Halma Deep Trekker, Ocean Modules, Oceaneering, Saab Seaeye, Saipem, Seamor, SLB, TechnipFMC, and VideoRay. Companies within the Global Remote Operated Vehicle Market are strengthening their competitive position by investing in research and development to introduce technologically advanced and energy-efficient systems. Strategic mergers, acquisitions, and partnerships enable broader product portfolios and expanded geographic reach. Many firms are focusing on modular system designs, enhanced data analytics integration, and improved sensor capabilities to increase operational flexibility. Establishing regional service hubs and long-term maintenance agreements with offshore operators helps secure recurring revenue streams.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Class

- 2.2.3 Application

- 2.2.4 Depth rating

- 2.2.5 System architecture

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of offshore oil & gas exploration

- 3.2.1.2 Rapid growth of offshore wind energy

- 3.2.1.3 Rising defense and naval modernization programs

- 3.2.1.4 Growth in subsea telecom and power cable infrastructure

- 3.2.1.5 Technological advancements in robotics and AI integration

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital and operational costs

- 3.2.2.2 Skilled operator shortage

- 3.2.2.3 Harsh offshore operating environments

- 3.2.2.4 Dependency on offshore energy cycles

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of deep-sea mining activities

- 3.2.3.2 Growth in marine research and environmental monitoring

- 3.2.3.3 Rising aquaculture and offshore farming operations

- 3.2.3.4 Integration with autonomous underwater vehicles (AUVs)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US Vessel Incidental Discharge Act

- 3.4.1.2 US coast guard safety regulations

- 3.4.1.3 Bureau of Safety and Environmental Enforcement (BSEE) Offshore Rules

- 3.4.2 Europe

- 3.4.2.1 EU Offshore Safety Directive

- 3.4.2.2 CE Marking & Machinery Directive Compliance

- 3.4.2.3 National Maritime Authority Variations

- 3.4.2.4 Offshore Renewable Energy Regulations

- 3.4.2.5 Diver Safety & Subsea Intervention Regulations

- 3.4.3 Asia Pacific

- 3.4.3.1 Chinese Offshore Regulatory Framework

- 3.4.3.2 Indian Offshore Regulatory Environment

- 3.4.3.3 ASEAN Maritime Harmonization Efforts

- 3.4.3.4 Japanese Maritime & Offshore Framework

- 3.4.3.5 Australia & South Korea Offshore Compliance Standards

- 3.4.4 Latin America

- 3.4.4.1 Brazilian Offshore Regulatory Framework

- 3.4.4.2 Mexican Offshore Safety & Environmental Regulations

- 3.4.4.3 Regional Offshore Harmonization Initiatives

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Offshore Regulatory Framework

- 3.4.5.2 South African Maritime Safety Regulations

- 3.4.5.3 West Africa & Red Sea Offshore Development Regulations

- 3.4.1 North America

- 3.5 Major market trends and disruptions

- 3.6 Future market trends

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By product

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Cost breakdown analysis

- 3.13 Patent analysis

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Class, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Work class ROV

- 5.3 Light work class ROV

- 5.4 Observation class ROV

- 5.5 Micro/mini ROV

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Aquaculture

- 6.3 Commercial & salvage diving

- 6.4 Municipal INFRASTRUCTURE

- 6.5 Military

- 6.6 Oil & Energy

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Depth Rating, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Shallow water ROVs (≤1,000 msw)

- 7.3 Mid-water ROVs (1,000-3,000 msw)

- 7.4 Deepwater ROVs (3,000-6,000 msw)

- 7.5 Ultra-deepwater ROVs (more than 6,000 msw)

Chapter 8 Market Estimates & Forecast, By System Architecture, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Vessel-integrated ROV systems

- 8.3 Modular containerized ROV systems

- 8.4 Fully containerized ROV systems

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Netherlands

- 9.3.8 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 DeepOcean

- 10.1.2 DOF Subsea

- 10.1.3 Forum Energy Technologies

- 10.1.4 Fugro

- 10.1.5 Kongsberg Maritime

- 10.1.6 Oceaneering International

- 10.1.7 Saab Seaeye

- 10.1.8 Saipem

- 10.1.9 SLB (Schlumberger)

- 10.1.10 TechnipFMC

- 10.2 Regional Players

- 10.2.1 ROVOP

- 10.2.2 AC-CESS Co UK

- 10.2.3 Anritsu Corp

- 10.2.4 Deep Ocean Engineering

- 10.2.5 Deep Ocean Search

- 10.2.6 SEAMOR Marine

- 10.2.7 Seatronics

- 10.3 Emerging Players

- 10.3.1 Deep Trekker

- 10.3.2 Rovtech

- 10.3.3 VideoRay