|

시장보고서

상품코드

1982361

신호 정보(SIGINT) 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Signals Intelligence (SIGINT) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

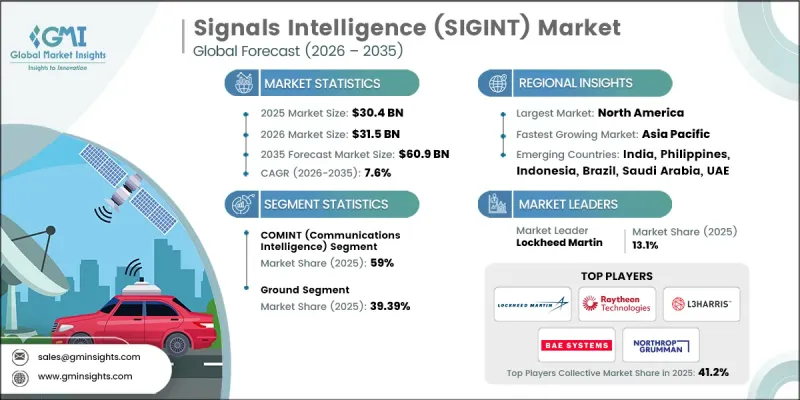

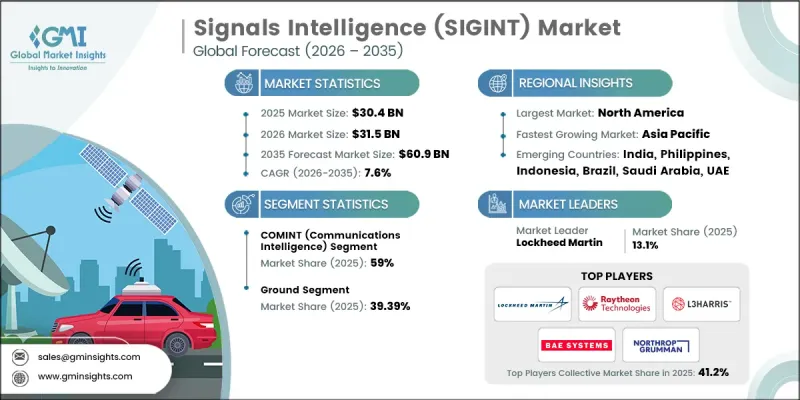

세계의 신호 정보(SIGINT) 시장은 2025년 304억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 7.6%로 확대되어 609억 달러에 이를 것으로 추정됩니다.

신호 정보(SIGINT) 산업은 현대 방어 및 국가 안보 전략에서 중요한 기둥으로 진화하고 있습니다. 지정학적 상황의 변화, 사이버 위협 증가, 주파수 대역의 혼잡, 그리고 전자전 활동의 확대에 의해 각국 정부는 SIGINT 능력을 단순한 지원 기능에서 핵심적인 전략 자산으로 격상시킬 것을 강요받고 있습니다. 정보기관은 복잡한 안보 환경에서 실시간 상황 인식을 얻고, 새로운 위협을 파악하고, 전략적 이점을 유지하기 위해 고급 SIGINT 시스템에 대한 의존도를 높이고 있습니다. 방어 예산 증가, 비대칭 분쟁 시나리오, 세계 통신 네트워크의 급속한 디지털화로 고급 SIGINT 플랫폼의 도입이 가속화되고 있습니다. 육상, 항공, 해군, 우주의 각 영역에 걸친 솔루션이 통합되어 다층적인 정보망이 구축되고 있습니다. 인공지능, 머신러닝, 클라우드 대응 분석, 소프트웨어 정의 아키텍처 등 기술의 진보가 데이터 처리 능력을 변화시키고 있습니다. 신호 검출의 고도화, 자동 분류, 전자기 데이터 스트림의 고속 분석을 통해 방어 에코시스템 전체의 운영 효율성과 정보 정밀도가 향상되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 규모 | 304억 달러 |

| 예측 금액 | 609억 달러 |

| CAGR | 7.6% |

통신 정보(COMINT) 부문은 2025년에 59%의 점유율을 차지했고 2035년까지 연평균 복합 성장률(CAGR) 7.8%를 나타낼 것으로 예측됩니다. COMINT는 다양한 네트워크를 가로질러 통신 신호를 가로채고 분석하는 필수적인 요건으로 지배적인 지위를 유지하고 있습니다. 적대세력의 연계와 의도에 대한 실용적인 지식을 제공하는 능력은 방위, 안보 및 전략적 작전을 지원합니다. 암호화 통신과 멀티채널 통신의 복잡화가 진행됨에 따라 방대한 데이터량을 처리하면서 정확하고 시기 적절한 정보 성과를 제공할 수 있는 고급 COMINT 시스템에 대한 수요가 높아지고 있습니다.

지상 부문은 2025년에 39.39%의 점유율을 차지했으며, 2026년부터 2035년까지 CAGR 6.2%를 나타낼 것으로 예측됩니다. 지상형 SIGINT 플랫폼은 신뢰성과 다양한 운영 환경에 대한 적응성을 통해 정보 작전의 핵심 역할을 계속하고 있습니다. 이러한 시스템은 전략적으로 중요한 위치에서 지속적인 모니터링과 신호 차단을 지원합니다. 보다 광범위한 방위 네트워크와의 통합은 지휘 수준에서 의사 결정과 전략 조정을 강화합니다. 유연한 전개 능력과 다른 정보 프레임워크 간의 상호 운용성은 신호 정보 시장에서 이 부문의 주도적 지위를 더욱 견고하게 만듭니다.

미국의 신호 정보(SIGINT) 시장은 93%의 점유율을 차지했으며, 2025년에는 164억 달러 규모에 도달했습니다. 이 나라 시장 성장은 방위의 현대화와 정보 능력에 대한 연방 정부의 지속적인 투자에 의해 지원됩니다. 증가하는 지정학적 긴장과 확대되는 사이버 및 전자전 상의 과제는 첨단 SIGINT 기술에 대한 장기적인 수요를 강화하고 있습니다. 방위 및 정보기관은 복수의 작전 영역에 걸쳐 정보 우위성을 유지하기 위해 실시간 정보 솔루션을 우선하고 있습니다. AI 기반 분석, 클라우드 컴퓨팅 통합 및 모듈식 시스템 아키텍처의 지속적인 혁신은 기술 업그레이드를 가속화하고 SIGINT 플랫폼의 라이프사이클 성능을 확장합니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 방위 현대화 프로그램 증가

- 사이버 공격 및 네트워크 침입의 급증

- AI 및 머신러닝 도입 확대

- 우주 및 위성 기반의 SIGINT 플랫폼 배치 확대

- 무인 및 휴대형 SIGINT 시스템의 이용 확대

- 업계의 잠재적 위험 및 과제

- 고급 SIGINT 시스템의 고비용

- 규제 및 프라이버시에 대한 우려

- 시장 기회

- 상업 및 민간 부문 수요 증가

- 신흥 시장에서 SIGINT 도입 급증

- IoT 및 5G 네트워크와의 통합 진전

- 매니지드 SIGINT 서비스 모델 증가

- 멀티 도메인 정보 작전의 상승

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 외국 정보 감시법(FISA)

- 국방수권법(NDAA)

- 통신 보안청법(캐나다)

- 규제 품목 프로그램(CGP)

- 유럽

- 독일 : 전기통신법(TKG)

- 영국 : 네트워크 및 정보 시스템(NIS) 보안 규칙

- 이탈리아 : 사이버 보안에 관한 정령

- 프랑스 : 디지털 공화국법

- 아시아태평양

- 중국 : 국가정보법

- 인도 : 정보기술(IT)법

- 일본 : 부정 액세스 방지법

- 호주 : 중요 인프라 보안법

- 라틴아메리카

- 브라질 : 국가정보법

- 멕시코 : 정보 및 국가 안보에 관한 연방법

- 아르헨티나 : 사이버 방어 규제

- 중동 및 아프리카(MEA)

- UAE : 사이버 보안 관련 연방법령

- 사우디아라비아 : 사이버 보안 및 정보 보호 프레임워크(CIPF)

- 남아프리카 : 통신 차단 및 통신 관련 정보 제공에 관한 법률(RICA)

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 특허 분석

- 비용 내역 분석

- 지속가능성 및 환경영향 분석

- 지속가능한 대처

- 폐기물 감축 전략

- 생산의 에너지 효율

- 친환경 대처

- 탄소발자국에 관한 고찰

- 방위 조달 및 취득의 프레임워크

- 플랫폼 아키텍처와 도입 모델

- 소프트웨어 정의형 및 AI를 활용한 SIGINT의 진화

- 멀티 도메인 및 크로스 인텔리전스의 통합

- 전망과 기회

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 유형별(2022-2035년)

- COMINT(통신 정보)

- ELINT(전자 정보)

- FISINT(외국 계측 신호 정보)

제6장 시장 추계 및 예측 : 용도별(2022-2035년)

- 사이버 네트워크

- 지상형

- 항공기 탑재형

- 전투기

- 수송용 항공기

- 무인 항공기(UAV)

- 해군

- 선박

- 잠수함

- 무인 해양 차량(UMV)

- 우주

제7장 시장 추계 및 예측 : 이동 수단별(2022-2035년)

- 고정식

- 휴대용

제8장 시장 추계 및 예측 : 최종 용도별(2022-2035년)

- 군 및 방위

- 정부 및 법 집행 기관

- 상업 및 민간 부문

제9장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 벨기에

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 필리핀

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카(MEA)

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계기업

- BAE Systems

- Boeing Defense

- General Dynamics Mission Systems

- L3Harris Technologies

- Leonardo

- Lockheed Martin

- Northrop Grumman

- Raytheon Technologies

- Thales

- Mitsubishi Electric

- 지역 기업

- Babcock International

- CACI International

- HENSOLDT

- Leidos

- QinetiQ

- Ultra Electronics

- 신흥기업

- Kawasaki Heavy Industries

- Mercury Systems

- NEC Corporation

- Palantir Technologies

The Global Signals Intelligence (SIGINT) Market was valued at USD 30.4 billion in 2025 and is estimated to grow 7.6% to reach USD 60.9 billion by 2035.

The signals intelligence (SIGINT) industry is evolving into a critical pillar of modern defense and national security strategies. Shifting geopolitical dynamics, rising cyber threats, spectrum congestion, and expanding electronic warfare activities are driving governments to elevate SIGINT capabilities from supporting functions to central strategic assets. Intelligence agencies are increasingly relying on advanced SIGINT systems to obtain real-time situational awareness, identify emerging threats, and maintain operational superiority across complex security environments. Growing defense allocations, asymmetric conflict scenarios, and rapid digitalization of global communications networks are accelerating the deployment of sophisticated SIGINT platforms. Solutions across land, air, naval, and space domains are being integrated to provide multi-layered intelligence coverage. Technological advancements such as artificial intelligence, machine learning, cloud-enabled analytics, and software-defined architectures are transforming data processing capabilities. Enhanced signal detection, automated classification, and faster analysis of electromagnetic data streams are strengthening operational efficiency and intelligence accuracy across defense ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $30.4 Billion |

| Forecast Value | $60.9 Billion |

| CAGR | 7.6% |

The communications intelligence (COMINT) segment held 59% share in 2025 and is projected to grow at a CAGR of 7.8% through 2035. COMINT maintains a dominant position due to the essential requirement to intercept and analyze communication signals across diverse networks. Its capability to provide actionable insights into adversarial coordination and intent supports defense, security, and strategic operations. The growing complexity of encrypted and multi-channel communications is increasing the need for advanced COMINT systems capable of managing high data volumes while delivering precise and timely intelligence outputs.

The ground segment held 39.39% share in 2025 and is anticipated to grow at a CAGR of 6.2% between 2026 and 2035. Ground-based SIGINT platforms remain central to intelligence operations due to their reliability and adaptability in various operational environments. These systems support continuous monitoring and signal interception in strategically sensitive locations. Their integration with broader defense networks enhances command-level decision-making and operational coordination. Flexible deployment capabilities and interoperability with other intelligence frameworks further reinforce the segment's leadership within the signals intelligence market.

United States Signals Intelligence (SIGINT) Market held 93% share, generating USD 16.4 billion in 2025. Market growth in the country is supported by sustained federal investment in defense modernization and intelligence capabilities. Rising geopolitical tensions and expanding cyber and electronic warfare challenges are strengthening long-term demand for advanced SIGINT technologies. Defense and intelligence agencies are prioritizing real-time intelligence solutions to maintain information superiority across multiple operational domains. Continuous innovation in AI-driven analytics, cloud computing integration, and modular system architectures is accelerating technology upgrades and extending the lifecycle performance of SIGINT platforms.

Key companies operating in the Global Signals Intelligence (SIGINT) Market include Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation (RTX), L3Harris Technologies, Inc., Thales, BAE Systems plc, Leidos Holdings, Mitsubishi Electric Corporation, QinetiQ Limited, and Ultra Electronics. Companies in the Signals Intelligence (SIGINT) Market are reinforcing their competitive position through sustained investment in research and development and strategic defense partnerships. Leading firms are integrating artificial intelligence, advanced analytics, and secure cloud architectures into next-generation SIGINT systems to enhance data processing speed and accuracy. Collaboration with government defense agencies and military organizations supports long-term contracts and modernization initiatives. Companies are also focusing on modular, software-defined platforms that allow scalable upgrades and lifecycle extensions. Expanding global presence through joint ventures and regional alliances strengthens market penetration.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.2.4 Mobility

- 2.2.5 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in defense modernization programs

- 3.2.1.2 Surge in cyberattacks and network intrusions

- 3.2.1.3 Rise in adoption of AI and machine learning

- 3.2.1.4 Increase in deployment of space- and satellite-based SIGINT platforms

- 3.2.1.5 Rise in use of unmanned and portable SIGINT systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Costs of Advanced SIGINT Systems

- 3.2.2.2 Regulatory and Privacy Concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Increase in demand from commercial and private sectors

- 3.2.3.2 Surge in SIGINT adoption in emerging markets

- 3.2.3.3 Rise in integration with IoT and 5G networks

- 3.2.3.4 Increase in managed SIGINT service models

- 3.2.3.5 Rise in multi-domain intelligence operations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Foreign Intelligence Surveillance Act (FISA)

- 3.4.1.2 National Defense Authorization Act (NDAA)

- 3.4.1.3 Communications Security Establishment Act (Canada)

- 3.4.1.4 Controlled Goods Program (CGP)

- 3.4.2 Europe

- 3.4.2.1 Germany: Telecommunications Act (TKG)

- 3.4.2.2 UK: Security of Network and Information Systems (NIS) Regulations

- 3.4.2.3 Italy: Legislative Decree on Cybersecurity

- 3.4.2.4 France: Digital Republic Act

- 3.4.3 Asia Pacific

- 3.4.3.1 China: National Intelligence Law

- 3.4.3.2 India: Information Technology (IT) Act

- 3.4.3.3 Japan: Act on Prohibition of Unauthorized Computer Access

- 3.4.3.4 Australia: Security of Critical Infrastructure Act

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Intelligence Law

- 3.4.4.2 Mexico: Federal Law on Intelligence and National Security

- 3.4.4.3 Argentina: Cyber Defense Regulations

- 3.4.5 MEA

- 3.4.5.1 UAE: Federal Decree Law on Cybersecurity

- 3.4.5.2 Saudi Arabia: Cybersecurity & Information Protection Framework (CIPF)

- 3.4.5.3 South Africa: Regulation of Interception of Communications and Provision of Communication-Related Information Act (RICA)

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental impact analysis

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Defense Procurement & Acquisition Framework

- 3.12 Platform Architecture & Deployment Models

- 3.13 Software-Defined & AI-Enabled SIGINT Evolution

- 3.14 Multi-Domain & Cross-Intelligence Integration

- 3.15 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 COMINT (Communications Intelligence)

- 5.3 ELINT (Electronic Intelligence)

- 5.4 FISINT (Foreign Instrumentation Signals Intelligence)

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Cyber & Network

- 6.3 Ground

- 6.4 Airborne

- 6.4.1 Fighter Jets

- 6.4.2 Transport Aircrafts

- 6.4.3 Unmanned Aerial Vehicles (UAVs)

- 6.5 Naval

- 6.5.1 Ships

- 6.5.2 Submarines

- 6.5.3 Unmanned Marine Vehicles (UMVs)

- 6.6 Space

Chapter 7 Market Estimates & Forecast, By Mobility, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Fixed

- 7.3 Portable

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Military & Defense

- 8.3 Government & Law Enforcement

- 8.4 Commercial & Private Sector

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Belgium

- 9.3.8 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Philippines

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 BAE Systems

- 10.1.2 Boeing Defense

- 10.1.3 General Dynamics Mission Systems

- 10.1.4 L3Harris Technologies

- 10.1.5 Leonardo

- 10.1.6 Lockheed Martin

- 10.1.7 Northrop Grumman

- 10.1.8 Raytheon Technologies

- 10.1.9 Thales

- 10.1.10 Mitsubishi Electric

- 10.2 Regional Players

- 10.2.1 Babcock International

- 10.2.2 CACI International

- 10.2.3 HENSOLDT

- 10.2.4 Leidos

- 10.2.5 QinetiQ

- 10.2.6 Ultra Electronics

- 10.3 Emerging Players

- 10.3.1 Kawasaki Heavy Industries

- 10.3.2 Mercury Systems

- 10.3.3 NEC Corporation

- 10.3.4 Palantir Technologies