|

시장보고서

상품코드

1982364

하이퍼차저 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Hypercharger Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

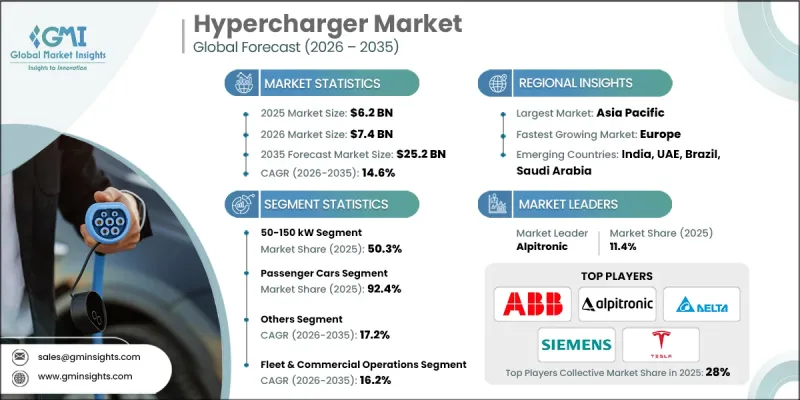

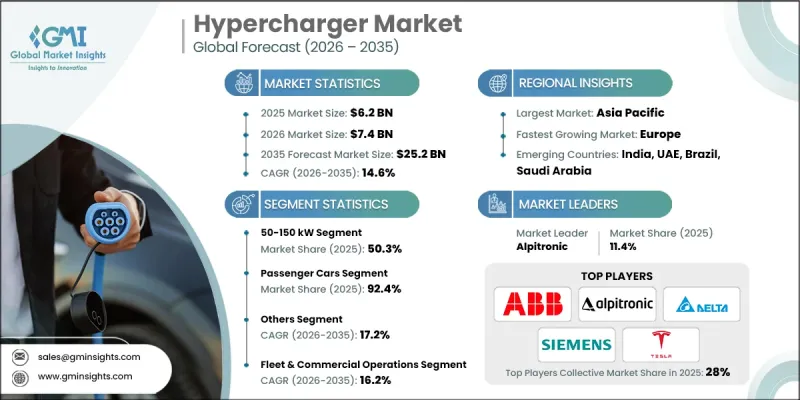

세계의 하이퍼차저 시장은 2025년 62억 달러로 평가되었으며 CAGR 14.6%로 성장해 2035년까지 252억 달러에 이를 것으로 추정됩니다.

세계의 지속가능성에 대한 노력의 가속화와 제로 배출 교통의 목표로 전기자동차(EV)의 보급이 현저하게 진행되고, 그 결과 고출력 충전 인프라에 대한 수요가 견인되고 있습니다. 자동차 제조업체가 라인업을 전동 모델로 계속 전환하는 동안, 보다 빠르고 효율적인 충전 솔루션의 필요성이 점점 중요해지고 있습니다. 충전 네트워크 사업자는 충전 시간을 단축하고 전반적인 편의성을 향상시키는 초고속 기술을 선호하여 EV 보급의 주요 장벽 중 하나를 다루고 있습니다. 선진국 및 신흥 시장에서 인프라를 확대해 장거리 전기 이동성에 대한 일반 시민의 신뢰가 높아지고 있습니다. 각국 정부는 정책 틀, 자금 지원 프로그램, 배출 감축 의무를 통해 도입을 지원하고 중심적인 역할을 하고 있습니다. 북미, 유럽, 아시아의 투자는 대용량 충전 회랑과 도시 허브의 설치를 가속화하고 있으며, 첨단 충전 시스템에 대한 액세스를 더욱 광범위하게 확보하고 있습니다. 공공기관과 민간기업 참가자와의 이러한 협조적인 노력으로 하이퍼차저는 진화하는 세계의 전기차 생태계의 필수적인 구성 요소로서의 지위를 확립하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 금액 | 62억 달러 |

| 예측 금액 | 252억 달러 |

| CAGR | 14.6% |

고출력 DC 충전 시스템은 기존의 충전 방식에 비해 차량 가동 정지 시간을 대폭 단축합니다. 일부 EV 플랫폼에서는 350kW 충전기에 연결하여 약 15분에서 30분 이내에 배터리 용량을 80%까지 복구할 수 있습니다. 대조적으로, 저출력 충전 솔루션은 유사한 충전 레벨에 도달하는 데 상당히 오랜 시간이 걸립니다. ABB, Tesla, IONITY 등의 업계 선두주자는 도시의 통근과 장거리 고속도로 주행을 모두 지원하도록 설계된 고급 급속 충전 기술을 도입하고 있습니다. 공공 부문의 지원으로 대용량 충전 네트워크에 중점을 둔 협력적인 자금 조달 메커니즘과 규제 측면의 지원을 통해 인프라 개발이 가속화되고 있습니다.

50-150kW 부문은 50.3%의 점유율을 차지했으며 2025년에는 31억 달러 시장 규모를 창출했습니다. 이 출력 범위는 광범위한 차종과의 호환성과 초고출력 시스템에 비해 상대적으로 낮은 설치 비용으로 여전히 널리 채택되고 있습니다. 이 카테고리의 충전기는 보통 1시간 내에 실용적인 항속거리를 충전할 수 있으며 차량이 중간 시간 주차되는 장소에 적합합니다. 비용 퍼포먼스의 밸런스에 의해 하이퍼차저 시장 전체에서 기초가 되는 층으로서 역할이 확고해지고 되고 있습니다.

승용차 부문은 2025년에 92.4%의 점유율을 차지했며, 2035년까지 226억 달러에 이를 것으로 예측됩니다. 이 압도적인 점유율은 충전 세션과 수익의 대부분을 자가용 차량이 차지하고 있다는 현실을 반영합니다. 대부분의 충전 활동은 주택이나 직장 환경에서 이루어지고 있지만, 장거리 이동이나 자가용 충전 인프라를 이용할 수 없는 운전자에게는 공공 급속 충전 네트워크가 필수적입니다. 수요 증가에 대응하기 위해 회랑 기반 인프라 계획과 도시 지역의 충전 허브는 계속 확대되고 있습니다.

미국의 하이퍼차저 시장은 충전 편의성 향상과 운송 부문 배출량 감소를 목적으로 연방 및 주 수준의 종합적인 노력에 힘입어 2025년에는 9억 8,790만 달러에 달했습니다. 정부 주도 인프라 정비 프로그램은 전국적인 연결성을 촉진하기 위해 전략적 교통 경로를 따라 고출력 충전소을 확장하는 데 기금을 제공합니다. 이러한 노력은 상호 운용성, 표준화된 도입 및 급속 충전 솔루션에 대한 광범위한 액세스를 선호하며, 항속 거리에 대한 불안을 줄이고 EV의 보급을 촉진하는 데 도움이 됩니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계 전기자동차(EV)의 보급 가속

- 충전 시간 단축과 고출력 인프라에 대한 수요 증가

- 정부 인센티브 및 국가 EV 인프라 정비 프로그램

- 고속도로 및 회랑 기반 급속 충전 네트워크의 확대

- 업계의 잠재적 위험 및 과제

- 송전망의 용량 제약 및 전력 배전의 제한

- 설치 및 송전망의 업그레이드에 수반하는 고액의 설비 투자

- 시장 기회

- 재생에너지 및 에너지 저장 시스템과의 통합

- 신흥 EV 시장 확대

- 인프라 확장을 위한 관민 파트너십

- 상용차 및 플릿 차량의 전기화 진전

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- SAE J3400

- J1772

- NEVI 프로그램 요건

- 유럽

- EU TEN-T 규제

- CCS 의무화

- 아시아태평양

- CHAdeMO 3.0

- GB/T

- 지역별 인센티브

- 라틴아메리카

- 브라질 ANEEL EV 충전 규제 프레임워크

- 멕시코의 EVSE 도입 이니셔티브

- 중동 및 아프리카

- UAE 국가 전기자동차 정책

- 두바이 및 아부다비의 EV 충전 네트워크 규제

- 북미

- 투자·자금 조달 분석

- 공공 인프라 투자(NEVI, EU 자금 지원 프로그램)

- 민간 자금 및 벤처 자본의 동향

- OEM 및 에너지 기업의 전략적 투자

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 고출력 DC 충전(350kW 이상의 도입)

- 모듈형 전력 아키텍처

- 수냉식 충전 케이블

- 동적 부하 관리

- 신흥기술

- 메가와트급 충전(대형 차량용 MCS)

- Vehicle-to-Grid(V2G)의 통합

- AI를 활용한 충전 최적화

- 신재생에너지 통합형 충전 거점

- 현재의 기술 동향

- 가격 분석(1차 조사에 기초)

- 과거 가격 동향 분석

- 사업자 유형별 가격 전략(프리미엄, 밸류, 코스트 플러스)

- 무역 데이터 분석(1차 조사에 기초)

- 수출입량 및 수출입액의 동향

- 주요 무역 회랑과 관세의 영향

- 특허 동향(1차 조사에 기초)

- 지속가능성과 환경에 미치는 영향

- 환경 영향 평가

- 사회적 영향과 지역사회에 대한 이익

- 거버넌스 및 기업의 사회적 책임

- 지속 가능한 금융 및 투자 동향

- AI가 가져오는 영향 하이퍼차저 시장

- AI에 의한 기존 비즈니스 모델의 변화

- 부문별 GenAI 이용 사례 및 도입 로드맵

- 위험, 제약 및 규제 고려 사항

- 신재생에너지 통합

- 하이퍼차저와 조합한 온사이트 태양광 발전(PV)

- 충전 인프라를 갖춘 에너지 저장 시스템(ESS)

- 원격 충전 허브용 마이크로그리드 아키텍처

- 재생에너지 통합을 수반하는 Vehicle-to-Grid(V2G)

- 다목적 시설용 공유 태양광 충전 허브

- 초급속 충전 네트워크의 급속한 확대

- 고속도로 회랑에서의 전개 전략

- 상용 및 플릿용 초고속 허브

- 관민 파트너십(PPP) 및 투자 모델

- 기술의 표준화와 상호 운용성

- 사례 연구

- 향후 전망과 기회

- 예측의 전제조건 및 시나리오 분석(1차 조사에 기초)

- 베이스 케이스 - CAGR을 견인하는 주요 거시 경제 및 업계 변수

- 상승 시나리오 - 거시 경제 및 업계의 순풍

- 하락 시나리오 - 거시 경제의 감속 또는 업계의 역풍

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카(MEA)

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 출력별(2022-2035년)

- 50-150 kW

- 150-350 kW

- 350kW 초과

제6장 시장 추계 및 예측 : 차량별(2022-2035년)

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- LCV

- MCV

- HCV

제7장 시장 추계 및 예측 : 커넥터별(2022-2035년)

- CCS(Combined Charging System)

- CHAdeMO

- GB/T

- 기타

제8장 시장 추계 및 예측 : 용도별(2022-2035년)

- 공공 충전소

- 간선도로

- 도시 충전소

- 플릿 및 상용 운영

- 소매 및 편의점

- 쇼핑센터 및 아울렛

- 서비스 스테이션

제9장 시장 추계 및 예측 : 충전 장소별(2022-2035년)

- 도시

- 교외 및 고속도로 연선

제10장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 러시아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 싱가포르

- 말레이시아

- 인도네시아

- 베트남

- 태국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 중동 및 아프리카(MEA)

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계 기업

- ABB

- Tesla

- Siemens

- ChargePoint

- Tritium

- Schneider Electric

- Eaton

- Blink Charging

- Delta Electronics

- Kempower

- 지역 기업

- EVgo Services

- Electrify America

- Alpitronic

- StarCharge

- Enel X Way

- EVBox

- 신흥기업

- Wallbox

- ADS-TEC Energy

- Compleo Charging

- Allego

The Global Hypercharger Market was valued at USD 6.2 billion in 2025 and is estimated to grow at a CAGR of 14.6% to reach USD 25.2 billion by 2035.

Accelerating sustainability initiatives and zero-emission transportation targets worldwide are significantly increasing electric vehicle adoption, which in turn is driving demand for high-power charging infrastructure. As automotive manufacturers continue shifting their portfolios toward electrified models, the need for faster and more efficient charging solutions has become increasingly critical. Charging network operators are prioritizing ultra-fast technologies that reduce charging times and improve overall convenience, thereby addressing one of the primary barriers to EV adoption. Infrastructure expansion across developed and emerging markets is strengthening public confidence in long-distance electric mobility. Governments are playing a central role by supporting deployment through policy frameworks, funding programs, and emission-reduction mandates. Investments across North America, Europe, and Asia are accelerating the installation of high-capacity charging corridors and urban hubs, ensuring broader accessibility to advanced charging systems. These coordinated efforts between public authorities and private industry participants are positioning hyperchargers as essential components of the evolving global electric mobility ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.2 Billion |

| Forecast Value | $25.2 Billion |

| CAGR | 14.6% |

High-power DC charging systems significantly reduce vehicle downtime compared to conventional alternatives. Certain EV platforms can replenish battery capacity to 80% within approximately 15 to 30 minutes when connected to 350 kW chargers. By contrast, lower-tier charging solutions require substantially longer durations to achieve similar levels. Industry leaders such as ABB, Tesla, and IONITY have introduced advanced fast-charging technologies designed to support both urban commuting and extended highway travel. Public-sector backing continues to accelerate infrastructure deployment through coordinated funding mechanisms and regulatory support focused on high-capacity charging networks.

The 50-150 kW segment held 50.3% share, generating USD 3.1 billion in 2025. This power range remains widely adopted due to its broad vehicle compatibility and comparatively lower installation costs than ultra-high-capacity systems. Chargers within this category typically deliver a meaningful driving range within a single hour, making them well-suited for locations where vehicles remain parked for moderate durations. Their cost-performance balance has solidified their role as a foundational tier within the overall hypercharger landscape.

The passenger vehicles segment accounted for 92.4% share in 2025 and is expected to reach USD 22.6 billion by 2035. This dominance reflects the reality that private vehicles represent the majority of charging sessions and revenue generation. While a substantial portion of charging activity occurs in residential and workplace environments, public fast-charging networks are essential for long-distance travel and for drivers without access to private charging infrastructure. Corridor-based infrastructure planning and urban charging hubs continue to expand to meet rising demand.

U.S. Hypercharger Market reached USD 987.9 million in 2025, supported by comprehensive federal and state-level initiatives aimed at improving charging accessibility and reducing transportation emissions. Government-backed infrastructure programs are funding the expansion of high-power charging stations along strategic transportation routes to facilitate nationwide connectivity. These efforts prioritize interoperability, standardized deployment, and widespread access to fast-charging solutions, helping to alleviate range anxiety and encourage broader EV adoption.

Major companies operating in the Global Hypercharger Market include Siemens, Schneider Electric, Delta Electronics, Alpitronic, Eaton, EVgo Services, Tritium, and Kempower. These companies compete through technological innovation, network expansion, and strategic collaborations with automakers and infrastructure developers. Companies in the Hypercharger Market are strengthening their competitive position by investing in next-generation high-power charging systems, expanding modular and scalable infrastructure solutions, and forming partnerships with automotive OEMs and utility providers. Many firms are focusing on improving charger uptime, enhancing software integration, and enabling smart-grid compatibility to optimize energy management. Geographic expansion into high-growth EV markets, combined with participation in government-funded infrastructure programs, is accelerating deployment. Businesses are also prioritizing interoperability standards and user-friendly digital platforms to improve customer experience.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Power Output

- 2.2.3 Vehicle

- 2.2.4 Connector

- 2.2.5 Application

- 2.2.6 Charging Location

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Accelerating global electric vehicle (EV) adoption

- 3.2.1.2 Growing demand for reduced charging time and high-power infrastructure

- 3.2.1.3 Government incentives and national EV infrastructure programs

- 3.2.1.4 Expansion of highway and corridor-based fast charging networks

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Grid capacity constraints and power distribution limitations

- 3.2.2.2 High capital expenditure for installation and grid upgrades

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with renewable energy and energy storage systems

- 3.2.3.2 Expansion in emerging EV markets

- 3.2.3.3 Public-private partnerships for infrastructure expansion

- 3.2.3.4 Increasing electrification of commercial and fleet vehicles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 SAE J3400

- 3.4.1.2 J1772

- 3.4.1.3 NEVI Program Requirements

- 3.4.2 Europe

- 3.4.2.1 EU TEN-T Regulations

- 3.4.2.2 CCS Mandates

- 3.4.3 Asia Pacific

- 3.4.3.1 CHAdeMO 3.0

- 3.4.3.2 GB/T

- 3.4.3.3 Regional Incentives

- 3.4.4 Latin America

- 3.4.4.1 Brazil ANEEL EV Charging Regulatory Framework

- 3.4.4.2 Mexico EVSE Deployment Initiatives

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE National Electric Vehicle Policy

- 3.4.5.2 Dubai/Abu Dhabi EV Charging Network Regulations

- 3.4.1 North America

- 3.5 Investment & Funding Analysis

- 3.5.1 Public infrastructure investments (NEVI, EU Funding Programs)

- 3.5.2 Private equity & venture capital trends

- 3.5.3 OEM & energy company strategic investments

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.1.1 High Power DC Charging (350 kW+ Deployments)

- 3.8.1.2 Modular Power Architecture

- 3.8.1.3 Liquid-Cooled Charging Cables

- 3.8.1.4 Dynamic Load Management

- 3.8.2 Emerging technologies

- 3.8.2.1 Megawatt-Class Charging (MCS for Heavy Duty)

- 3.8.2.2 Vehicle-to-Grid (V2G) Integration

- 3.8.2.3 AI-Enabled Charging Optimization

- 3.8.2.4 Renewable-Integrated Charging Sites

- 3.8.1 Current technological trends

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.9.1 Historical price trend analysis

- 3.9.2 Pricing strategy by player type (Premium / Value / Cost-plus)

- 3.10 Trade data analysis (Driven by Primary Research)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Patent landscape (Driven by Primary Research)

- 3.12 Sustainability and environmental impact

- 3.12.1 Environmental impact assessment

- 3.12.2 Social impact & community benefits

- 3.12.3 Governance & corporate responsibility

- 3.12.4 Sustainable finance & investment trends

- 3.13 Impact of AI on the hypercharger market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Integration of Renewable Energy

- 3.14.1 On site solar photovoltaic (PV) coupled with hyperchargers

- 3.14.2 Energy storage systems (ESS) with charging infrastructure

- 3.14.3 Microgrid architectures for remote charging hubs

- 3.14.4 Vehicle-to-grid (V2G) with renewable integration

- 3.14.5 Shared solar charging hubs for multi-use sites

- 3.15 Rapid expansion of ultra-fast charging networks

- 3.15.1 Highway corridor deployment strategies

- 3.15.2 Commercial and fleet-oriented ultra-fast hubs

- 3.15.3 Public-private partnerships (PPPs) and investment models

- 3.15.4 Technological standardization and interoperability

- 3.16 Case studies

- 3.17 Future outlook & opportunities

- 3.18 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.18.1 Base Case - key macro & industry variables driving CAGR

- 3.18.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.18.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Power Output, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 50-150 kW

- 5.3 150-350 kW

- 5.4 Above 350kW

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 LCV

- 6.3.2 MCV

- 6.3.3 HCV

Chapter 7 Market Estimates & Forecast, By Connector, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 CCS (Combined Charging System)

- 7.3 CHAdeMO

- 7.4 GB/T

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 Public charging hubs

- 8.2.1 Highway corridors

- 8.2.2 Urban charging plazas

- 8.3 Fleet & commercial operations

- 8.4 Retail & convenience

- 8.4.1 Shopping centers & outlets

- 8.4.2 Service stations

Chapter 9 Market Estimates & Forecast, By Charging Location, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 Urban

- 9.3 Sub-Urban / highway corridors

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Russia

- 10.3.8 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.4.10 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 ABB

- 11.1.2 Tesla

- 11.1.3 Siemens

- 11.1.4 ChargePoint

- 11.1.5 Tritium

- 11.1.6 Schneider Electric

- 11.1.7 Eaton

- 11.1.8 Blink Charging

- 11.1.9 Delta Electronics

- 11.1.10 Kempower

- 11.2 Regional players

- 11.2.1 EVgo Services

- 11.2.2 Electrify America

- 11.2.3 Alpitronic

- 11.2.4 StarCharge

- 11.2.5 Enel X Way

- 11.2.6 EVBox

- 11.3 Emerging players

- 11.3.1 Wallbox

- 11.3.2 ADS-TEC Energy

- 11.3.3 Compleo Charging

- 11.3.4 Allego