|

시장보고서

상품코드

1982368

폴리염화알루미늄 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Poly Aluminum Chloride Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

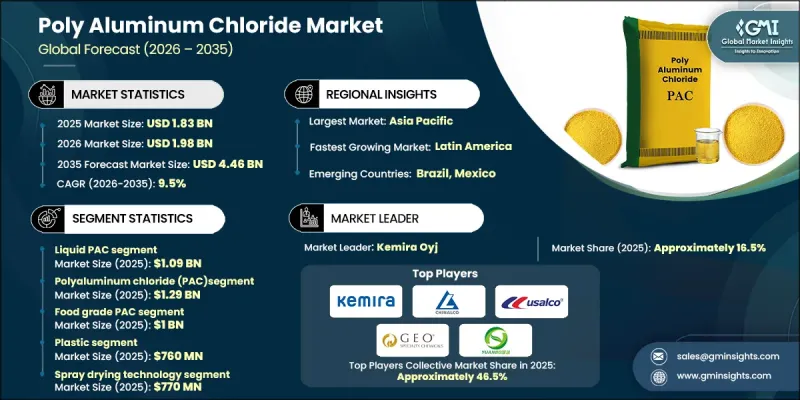

세계의 폴리염화알루미늄 시장은 2025년에 18억 3,000만 달러로 평가되었으며, CAGR 9.5%로 성장하여 2035년까지 44억 6,000만 달러에 이를 것으로 예측됩니다.

폴리염화알루미늄 산업은 지자체 및 산업용 수처리 응용 분야에서 수요가 증가함에 따라 강력한 확대를 이루고 있습니다. 신흥국의 급속한 도시화와 대규모 인프라 개발로 식수 및 폐수처리시설에 대한 공적 및 민간 투자가 대폭 증가하고 있습니다. 이러한 추세는 탁도, 부유 입자 및 기타 오염물질을 제거하는 높은 효율을 가진 폴리염화알루미늄의 소비를 증가시킵니다. 수질 규제의 강화와 배출 기준 엄격화로 인해 첨단 응집제로의 전환이 더욱 가속화되고 있습니다. 섬유, 펄프 및 제지, 화학, 식품 가공의 각 섹터에서 산업 활동의 확대에 수반해, 배출 전에 효과적인 처리를 필요로 하는 대량의 폐수가 발생하고 있습니다. 기존 응집제에 비해 폴리염화알루미늄은 응집이 빠르고, 발생하는 슬러지량도 적기 때문에 운용 효율의 향상과 처분 비용의 삭감으로 이어집니다. 따라서 지속적인 산업화와 지속적인 규제의 시행은 세계적으로 폴리염화알루미늄에 대한 꾸준하고 장기적인 수요의 성장으로 이어지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 금액 | 18억 3,000만 달러 |

| 예측 금액 | 44억 6,000만 달러 |

| CAGR | 9.5% |

액체 PAC 부문은 2025년에 10억 9,000만 달러를 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 9.2%를 나타낼 것으로 예측됩니다. 다양한 제품 형태에 대한 수요는 용도에 따라 취급, 보관 및 투여 요건과 밀접하게 관련되어 있습니다. 액체 폴리염화알루미늄은 펌프 이송이 용이하고, 안정된 투여 능력과 신속한 반응 성능을 갖추고 있기 때문에 대규모 지자체 및 산업용 처리 시설에서 점점 선호되고 있습니다. 한편, 분말, 과립, 플레이크 형태는 장기 보존성, 운송의 간소화 및 유연한 적용이 중요한 고려사항이 되는 분산형 또는 소규모 처리 시설에서 지지를 모으고 있습니다. 이러한 제품 형태의 다양화는 표준화된 솔루션에 의존하지 않고 운영상의 적응성을 강조하는 업계 전반의 큰 변화를 반영합니다.

폴리염화알루미늄(PAC) 부문 시장 규모는 2025년 12억 9,000만 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 9.2%로 성장할 것으로 추정됩니다. 각종 PAC 등급에 걸친 시장의 발전은 처리 효율과 수질 화학적 요건에 근거한 제품 차별화의 진전을 부각하고 있습니다. 전통적인 PAC는 지자체 및 산업 분야에서 비용 성능이 균형을 이루고 있기 때문에 계속 높은 채용률을 유지하고 있습니다. 동시에, 안정성과 응집 효율의 향상이 요구되는 보다 복잡한 폐수 조성에 대해서는 폴리염화알루미늄 황산염이나 복합 PAC 제제 등의 개량형 제품이 채용되고 있습니다. 이 진화는 획일적인 처리 접근법이 아니라 개별 요구에 맞는 화학 처리 솔루션으로의 전환을 돋보이게합니다.

북미의 폴리염화알루미늄 시장은 2025년 4억 6,000만 달러 규모에 이르렀습니다. 지역적 확대는 노후화된 수도 인프라에 대한 투자 증가와 식수 및 배수에 관한 규제 체제의 엄격화에 의해 지원되고 있습니다. 지자체 수도 유틸리티나 산업 사업자는 처리 성능을 향상시키면서 슬러지 관리 비용을 삭감하는 첨단 응집 기술에 보다 많은 예산을 할당하고 있습니다. 이 지역 내에서는 미국에서 처리 시설의 현대화와 장기적인 시스템의 신뢰성 향상을 목적으로 하는 공적 자금에 의한 대처에 지지되어 고성능 PAC 등급의 채용이 가속화되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 미래 시장 동향

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 특허 동향

- 무역 통계(주: 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산의 에너지 효율

- 친환경 이니셔티브

- 탄소발자국에 관한 고찰

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 형태별(2022-2035년)

- 액체 PAC

- 분말 PAC(분무 건조)

- 입상 PAC

- 플레이크상 PAC(드럼 건조)

제6장 시장 추계 및 예측 : 제품 유형별(2022-2035년)

- 폴리염화알루미늄(PAC)

- 폴리염화알루미늄 클로로설파이드(PACS)

- 알루미늄 클로로하이드레이트(ACH)

- 복합 PAC

- 나노 PAC

제7장 시장 추계 및 예측 : 등급별(2022-2035년)

- 식품용 PAC

- 식수용 PAC

- 산업 등급 PAC

- 필터 등급 PAC

제8장 시장 추계 및 예측 : 염기성별(2022-2035년)

- 저염기성

- 중간 염기성

- 고염기성

- 초고염기성

제9장 시장 추계 및 예측 : 제조 공정별(2022-2035년)

- 분무 건조 기술

- 드럼 건조 기술

- 전기투석법

- 산 가용성 알루미늄 재법

제10장 시장 추계 및 예측 : 최종 사용 산업별(2022-2035년)

- 수처리

- 펄프 및 제지

- 섬유 산업 산업

- 석유 및 가스 산업

- 의약품 및 화장품

- 기타

제11장 시장 추계 및 예측 : 용도별(2022-2035년)

- 응집 및 응집

- 슬러지 탈수

- 막 전처리

- 인 제거

- 중금속 제거

- 유기물 및 NOM 제거

- 기타

제12장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제13장 기업 프로파일

- Alumichem A/S

- Biosynth

- CHALCO Advanced Material Co., Ltd.

- EMCO Dyestuff

- Fengchen Group Co.,Ltd

- GEO Specialty Chemicals

- Henan Chemger Group Corporation

- Henan Yuanbo Environmental Technology Co., Ltd.

- Kavya Pharma

- Kemira Oyj

- NR CHEMICALS

- Taki Chemical

- USALCO

- Venator Materials

The Global Poly Aluminum Chloride Market was valued at USD 1.83 billion in 2025 and is estimated to grow at a CAGR of 9.5% to reach USD 4.46 billion by 2035.

The poly aluminum chloride industry is experiencing strong expansion driven by rising demand across municipal and industrial water treatment applications. Rapid urban growth and large-scale infrastructure development in emerging economies are prompting significant public and private investments in drinking water and wastewater treatment facilities. This trend is increasing the consumption of poly aluminum chloride due to its high efficiency in removing turbidity, suspended particles, and other contaminants. Tightening water quality regulations and stricter discharge standards are further accelerating the shift toward advanced coagulants. Expanding industrial operations across textiles, pulp and paper, chemicals, and food processing sectors are generating substantial wastewater volumes that require effective treatment before discharge. Compared to conventional coagulants, poly aluminum chloride delivers faster coagulation and produces lower sludge volumes, enhancing operational efficiency and reducing disposal costs. Sustained industrialization and continuous regulatory enforcement are therefore translating into consistent and long-term demand growth for poly aluminum chloride worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.83 Billion |

| Forecast Value | $4.46 Billion |

| CAGR | 9.5% |

The liquid PAC segment accounted for USD 1.09 billion in 2025 and is expected to grow at a CAGR of 9.2% from 2026 to 2035. Demand for different product forms is closely linked to application-specific handling, storage, and dosing requirements. Liquid poly aluminum chloride is increasingly preferred in large municipal and industrial treatment plants due to its ease of pumping, consistent dosing capability, and rapid reaction performance. Meanwhile, powdered, granular, and flake forms are gaining traction in decentralized or smaller-scale treatment facilities where extended shelf life, simplified transportation, and flexible application are critical considerations. This diversification in product formats reflects a broader industry shift toward operational adaptability rather than reliance on standardized solutions.

The poly aluminum chloride (PAC) segment was valued at USD 1.29 billion in 2025 and is estimated to grow at a CAGR of 9.2% through 2035. Market development across various PAC grades highlights growing product differentiation based on treatment efficiency and water chemistry requirements. Conventional PAC continues to maintain strong adoption due to its balanced cost-to-performance ratio across municipal and industrial uses. At the same time, enhanced variants such as poly aluminum chlorosulfate and composite PAC formulations are being adopted for more complex wastewater compositions requiring improved stability and coagulation efficiency. This evolution underscores a transition toward tailored chemical treatment solutions instead of a uniform treatment approach.

North America Poly Aluminum Chloride Market generated USD 0.46 billion in 2025. Regional expansion is supported by increased investments in aging water infrastructure and stricter regulatory frameworks governing potable water and wastewater discharge. Municipal utilities and industrial operators are allocating greater budgets to advanced coagulation technologies that improve treatment performance while lowering sludge management expenses. Within the region, the United States is witnessing accelerated adoption of high-performance PAC grades, supported by public funding initiatives aimed at modernizing treatment facilities and improving long-term system reliability.

Key companies operating in the Global Poly Aluminum Chloride Market include Kemira Oyj, USALCO, CHALCO Advanced Material Co., Ltd., GEO Specialty Chemicals, Henan Yuanbo Environmental Technology Co., Ltd., and other regional participants. Companies in the Global Poly Aluminum Chloride Market are reinforcing their competitive position through investments in research and development focused on high-efficiency and low-sludge formulations. Strategic partnerships with municipal authorities and industrial operators are expanding long-term supply agreements and strengthening distribution networks. Many manufacturers are enhancing production capacities and optimizing supply chains to ensure consistent quality and cost competitiveness. Product portfolio diversification, including specialized PAC grades tailored to complex wastewater conditions, is improving market differentiation.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Form

- 2.2.3 Product Type

- 2.2.4 Grade

- 2.2.5 Basicity

- 2.2.6 Manufacturing Process

- 2.2.7 End-User Industry

- 2.2.8 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Form, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Liquid PAC

- 5.3 Powder PAC (spray-dried)

- 5.4 Granular PAC

- 5.5 Flaky PAC (drum-dried)

Chapter 6 Market Estimates and Forecast, By Product Type, 2022- 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Poly aluminum chloride (PAC)

- 6.3 Polyaluminum chlorosulfate (PACS)

- 6.4 Aluminum chlorohydrate (ACH)

- 6.5 Composite PAC

- 6.6 Nano-PAC

Chapter 7 Market Estimates and Forecast, By Grade, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Food grade PAC

- 7.3 Drinking water grade PAC

- 7.4 Industrial grade PAC

- 7.5 Filter grade PAC

Chapter 8 Market Estimates and Forecast, By Basicity, 2022 - 2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Low basicity

- 8.3 Medium basicity

- 8.4 High basicity

- 8.5 Ultra-high basicity

Chapter 9 Market Estimates and Forecast, By Manufacturing Process, 2022 - 2035 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 Spray drying technology

- 9.3 Drum drying technology

- 9.4 Electrodialysis process

- 9.5 Acid-soluble aluminum ash method

Chapter 10 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Billion, Kilo Tons)

- 10.1 Key trends

- 10.2 Water treatment

- 10.3 Pulp & paper industry

- 10.4 Textiles industry

- 10.5 Oil & gas industry

- 10.6 Pharmaceutical & cosmetics

- 10.7 Others

Chapter 11 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion, Kilo Tons)

- 11.1 Key trends

- 11.2 Coagulation & flocculation

- 11.3 Sludge dewatering

- 11.4 Membrane pre-treatment

- 11.5 Phosphorus removal

- 11.6 Heavy metal removal

- 11.7 Organic matter & NOM removal

- 11.8 Others

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Rest of Europe

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Rest of Asia Pacific

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Rest of Latin America

- 12.6 Middle East & Africa

- 12.6.1 Saudi Arabia

- 12.6.2 South Africa

- 12.6.3 UAE

- 12.6.4 Rest of Middle East & Africa

Chapter 13 Company Profiles

- 13.1 Alumichem A/S

- 13.2 Biosynth

- 13.3 CHALCO Advanced Material Co., Ltd.

- 13.4 EMCO Dyestuff

- 13.5 Fengchen Group Co.,Ltd

- 13.6 GEO Specialty Chemicals

- 13.7 Henan Chemger Group Corporation

- 13.8 Henan Yuanbo Environmental Technology Co., Ltd.

- 13.9 Kavya Pharma

- 13.10 Kemira Oyj

- 13.11 N. R. CHEMICALS

- 13.12 Taki Chemical

- 13.13 USALCO

- 13.14 Venator Materials