|

시장보고서

상품코드

1998667

비전기식 정맥 주입 펌프 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Non-electric Intravenous Infusion Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

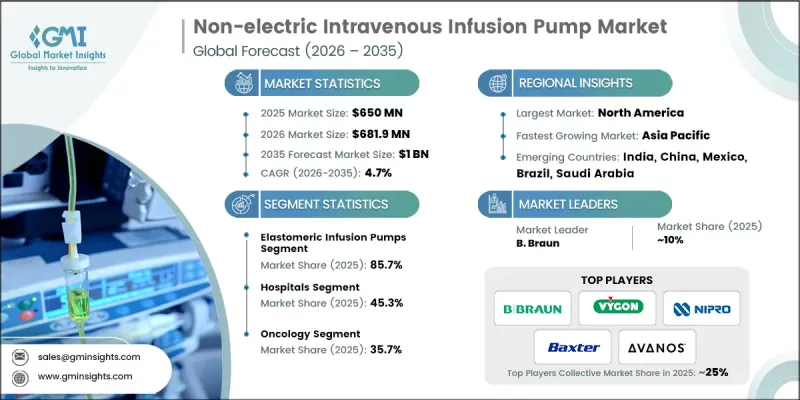

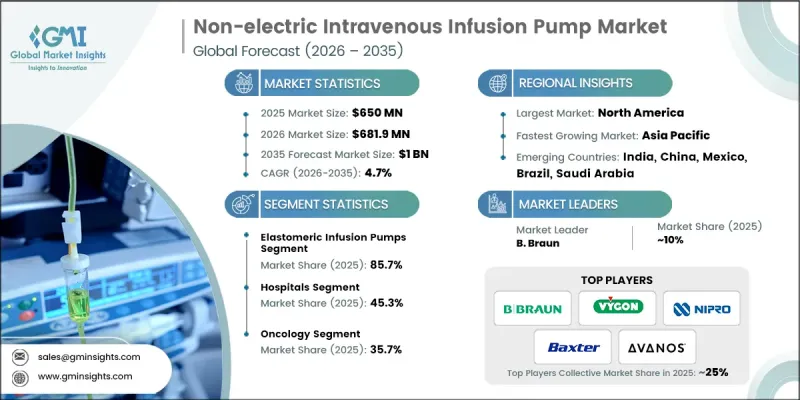

세계의 비전기식 정맥 주입 펌프 시장은 2025년에 6억 5,000만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.7%로 성장하여 10억 달러에 달할 것으로 예측됩니다.

비전기식 정맥 주입 펌프 시장의 성장은 전 세계 만성질환 유병률 증가와 수술 건수 증가에 힘입어 성장세를 보이고 있습니다. 또한, 의료 종사자들은 전동식 주입 장치에 대한 경제적 대안을 점점 더 많이 찾고 있으며, 이는 기계식 주입 기술에 대한 수요를 촉진하고 있습니다. 비 전동식 정맥주입 펌프는 배터리나 전원이 필요 없이 제어된 속도로 수액이나 약물을 투여할 수 있도록 설계된 소형 의료기기입니다. 이러한 설계로 조작의 편의성을 유지하면서 치료제를 일관성 있게 투여할 수 있습니다. 또한, 기존 병원 환경 외에서 지속적 또는 장기적인 약물 투여에 대한 니즈가 증가하고 있는 것도 수요 증가의 요인으로 작용하고 있습니다. 이 시스템은 휴대성, 조작의 용이성, 최소한의 유지보수 요구 사항으로 유명하며, 재택치료 프로그램이나 자원이 제한된 시설에 이상적입니다. 또한, 이러한 펌프가 환자의 이동성을 개선하고 조기 퇴원 프로토콜을 촉진하는 능력은 다양한 임상 환경에서의 도입을 가속화하고 있습니다. 재택치료로의 전환이 진행되고 있는 것도 비동력 수액 기술의 채택을 더욱 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 6억 5,000만 달러 |

| 예측액 | 10억 달러 |

| CAGR | 4.7% |

2025년 엘라스토머 주입 펌프 부문은 실용적인 디자인, 휴대성, 안정적인 약물 투여 능력에 힘입어 85.7%의 시장 점유율을 차지했습니다. 엘라스토머 주입 펌프는 복잡한 설정이나 전자 부품 없이도 지속적인 약물 투여가 가능하기 때문에 비전기식 정맥주입 펌프 업계에서 가장 널리 사용되는 카테고리입니다. 이 장치는 제어된 속도로 약물을 점진적으로 방출하는 탄성 저장소에 의존하여 일관된 치료 제공을 보장합니다. 컴팩트한 구조와 정숙성은 특히 이동성과 사용 편의성이 필수적인 의료 환경에서 환자와 의료진의 편의성을 높여줍니다.

종양학 분야는 2025년 35.7%로 가장 큰 매출 점유율을 차지했으며, 안정적이고 통제된 약물 투여가 필요한 장기 정맥주사 요법의 사용 증가로 인해 2035년까지 3억 8,890만 달러에 달할 것으로 예측됩니다. 비동력 수액 시스템은 휴대성이 뛰어나 기존 병원 환경을 넘어선 치료 시행이 가능해 종양학 치료 프로그램에서 널리 활용되고 있습니다. 전 세계적으로 증가하는 암 부담과 분산형 종양학 치료 서비스의 확대는 예측 기간 동안 이러한 수액 시스템에 대한 수요를 지속적으로 견인할 것으로 예측됩니다.

미국의 비동력 정맥주입 펌프 시장은 2025년 2억 5,320만 달러 규모에 달할 것으로 예측됩니다. 이는 많은 의료 시술 건수, 외래 수액요법의 보급, 그리고 잘 정비된 재택의료 생태계가 뒷받침하고 있습니다. 유리한 상환 제도와 외래 진료 모델에 대한 의존도가 높아짐에 따라 이러한 장비의 도입이 계속 증가하고 있습니다. 또한, 기존 제조업체의 존재와 의료진의 엘라스토머 수액 기술에 대한 이해도가 높아짐에 따라 병원, 외래 환자 및 재택 치료 제공업체의 지속적인 수요에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별, 2022-2035

제6장 시장 추산 및 예측 : 용도별, 2022-2035

제7장 시장 추산 및 예측 : 최종 용도별, 2022-2035

제8장 시장 추산 및 예측 : 지역별, 2022-2035

제9장 기업 개요

LSH 26.04.23The Global Non-electric Intravenous Infusion Pump Market was valued at USD 650 million in 2025 and is estimated to grow at a CAGR of 4.7% to reach USD 1 billion by 2035.

Growth across the non-electric intravenous infusion pump market for non-electric systems is supported by the increasing prevalence of long-term medical conditions and the rising number of surgical interventions worldwide. Healthcare providers are also increasingly looking for economical alternatives to electrically powered infusion devices, which is strengthening the demand for mechanical infusion technologies. Non-electric intravenous infusion pumps are compact medical devices designed to administer fluids and medications at controlled rates without the need for batteries or electrical power. Their design allows consistent delivery of therapeutic agents while maintaining operational simplicity. Demand is also rising due to the increasing need for continuous or extended drug administration outside conventional hospital settings. These systems are recognized for their portability, straightforward operation, and minimal maintenance requirements, making them well-suited for home healthcare programs and facilities with limited resources. Additionally, the ability of these pumps to support improved patient mobility and facilitate early discharge protocols has accelerated their acceptance in various clinical environments. The growing shift toward home-centered medical care is further strengthening the adoption of non-electric infusion technologies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $650 Million |

| Forecast Value | $1 Billion |

| CAGR | 4.7% |

The elastomeric infusion pumps segment accounted for a substantial 85.7% share in 2025, driven by their practical design, portability, and dependable medication delivery capabilities. Elastomeric infusion pumps represent the most widely utilized category within the non-electric intravenous infusion pump industry because they provide continuous drug administration without requiring complex setup or electronic components. These devices rely on an elastic reservoir that gradually releases medication at a controlled rate, ensuring consistent therapy delivery. Their compact structure and silent functioning enhance convenience for patients and healthcare professionals, particularly in care environments where mobility and ease of use are essential.

The oncology application segment held a leading revenue share of 35.7% in 2025 and is projected to reach USD 388.9 million by 2035, owing to the increasing use of prolonged infusion therapies that require stable and controlled medication delivery. Non-electric infusion systems are widely utilized in oncology treatment programs because their portable design supports therapy administration beyond traditional hospital environments. The increasing global burden of cancer and the expansion of decentralized oncology care services are expected to continue driving demand for these infusion systems throughout the forecast period.

U.S. Non-electric Intravenous Infusion Pump Market generated USD 253.2 million in 2025, supported by high volumes of medical procedures, widespread use of ambulatory infusion therapies, and a well-developed home healthcare ecosystem. Favorable reimbursement frameworks and increasing reliance on outpatient care models continue to strengthen the adoption of these devices. Additionally, the presence of established manufacturers and growing familiarity among healthcare professionals with elastomeric infusion technologies are contributing to sustained demand across hospitals, outpatient facilities, and home-based treatment providers.

Key companies operating in the Global Non-electric Intravenous Infusion Pump Market include Baxter, B. Braun, AVANOS, Ambu, NIPRO, VYGON, Go Medical Industries, Technoline, Multimedical, and Epic. Companies participating in the Non-electric Intravenous Infusion Pump Market are implementing several strategic initiatives to strengthen their market position and expand global reach. Leading manufacturers are focusing heavily on research and development to improve device reliability, safety, and user convenience while maintaining cost efficiency. Many companies are also expanding their product portfolios with advanced infusion systems designed for broader therapeutic applications. Strategic partnerships with healthcare providers and distribution networks are helping organizations increase product accessibility in both developed and emerging healthcare markets. In addition, firms are prioritizing regulatory approvals and compliance with international healthcare standards to accelerate global market entry.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic conditions

- 3.2.1.2 Increasing number of people undergoing surgical procedures

- 3.2.1.3 Shift toward home-based care

- 3.2.1.4 Surging demand for a low-cost alternative to electronic pumps

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited usage in high-acuity clinical settings

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of home-care and ambulatory infusion services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape (Driven by primary research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by primary research)

- 3.7 Patent analysis

- 3.8 Pricing analysis (Driven by primary research)

- 3.9 Customer insights (Driven by primary research)

- 3.10 Impact of AI and generative AI on the market

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Elastomeric infusion pumps

- 5.3 Mechanical pumps

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Oncology

- 6.3 Pediatrics/Neonatology

- 6.4 Pain Management

- 6.5 Diabetes

- 6.6 Gastroenterology

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Home care settings

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Ambu

- 9.2 AVANOS

- 9.3 B. Braun

- 9.4 Baxter

- 9.5 epic

- 9.6 Go Medical Industries

- 9.7 Multimedical

- 9.8 NIPRO

- 9.9 Technoline

- 9.10 VYGON