|

시장보고서

상품코드

1998680

신장 결석 관리 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Kidney Stone Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

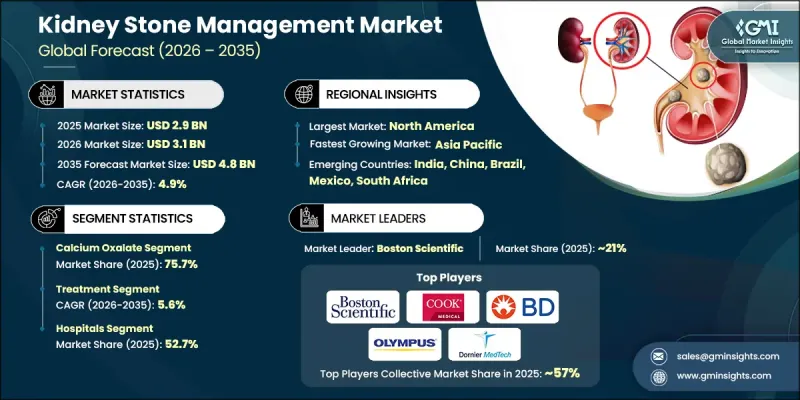

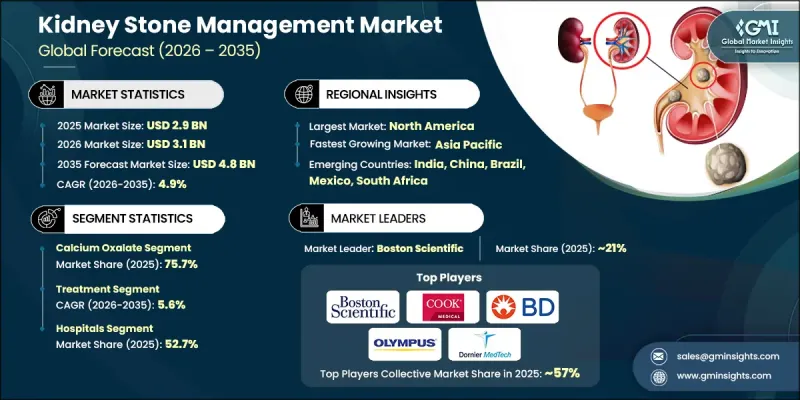

세계의 신장 결석 관리 시장은 2025년에 29억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.9%로 성장하여 48억 달러에 달할 것으로 예측됩니다.

신장 결석 관리 시장의 성장은 전 세계 신장 결석 질환의 유병률 증가, 치료 기술의 지속적인 발전, 그리고 고령화 인구의 꾸준한 증가에 의해 뒷받침되고 있습니다. 의료진은 요로 질환과 관련된 환자 수가 증가함에 따라 신뢰할 수 있는 진단 도구와 효과적인 치료 솔루션에 대한 수요가 증가하고 있습니다. 의료기술의 발전으로 결석 검출의 정확도가 향상되고, 치료 효율과 환자의 안전도도 높아지고 있습니다. 또한 저침습적 치료로의 전환으로 회복 기간 단축과 시술 위험 감소를 실현하여 치료의 방식을 변화시키고 있습니다. 병원과 전문 클리닉에서는 임상 결과의 향상과 환자 관리의 최적화를 위해 최신 의료기기와 첨단 시술 기술의 도입이 점점 더 많이 이루어지고 있습니다. 또한, 디지털 진단 기술과 영상 진단 기술의 통합을 통해 의료진은 신장 결석을 조기에 발견하고 보다 정밀한 치료 전략을 수립할 수 있게 되었습니다. 이러한 발전과 함께 신장 결석 관리 시장은 꾸준히 성장하고 있으며, 환자 치료의 전반적인 질도 향상되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 29억 달러 |

| 예측액 | 48억 달러 |

| CAGR | 4.9% |

신장결석의 관리에는 영상진단, 약물 치료, 최소침습적 또는 외과적 시술을 통한 신장결석의 확인, 치료 및 장기적인 관리가 포함됩니다. 이러한 중재의 주요 목적은 증상 완화, 결석 제거 또는 분쇄, 재발 방지 및 정상적인 요로 기능 회복에 있습니다. 요관경 검사, 레이저 결석파쇄술, 체외충격파쇄석술, 경피적 시술에 사용되는 기술의 발전으로 치료 효과가 크게 향상되었습니다. 이러한 개선을 통해 임상의는 합병증을 최소화하면서 보다 정밀한 시술을 할 수 있게 되었습니다. 또한, 의료시설에서 최소침습적 시술 및 외래 수술 솔루션의 도입을 확대함에 따라 이 산업은 빠르게 성장하고 있습니다.

2025년에는 옥살산 칼슘 결석 부문이 75.7%의 점유율을 차지했습니다. 이 부문이 선두를 달리고 있는 이유는 주로 신장 결석의 발생률이 높고, 대사 및 식습관 관련 위험 요인과 밀접한 관련이 있기 때문입니다. 이 질환으로 진단된 환자들은 종종 반복적인 경과 관찰과 의료적 개입이 필요하기 때문에 진단 및 치료 솔루션에 대한 수요가 지속되고 있습니다. 이런 유형의 신장결석은 재발하는 경우가 많기 때문에 의료진은 식이요법, 약물 치료, 정기적인 경과 관찰을 포함한 장기적인 관리 전략을 중시합니다. 따라서 이러한 결석의 높은 유병률과 재발하기 쉬운 특성은 신장 결석 관리 시장에서 옥살산칼슘 부문의 성장을 지속적으로 뒷받침하고 있습니다.

치료 부문은 2025년 17억 달러 시장 규모를 기록했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 5.6%를 나타낼 것으로 예측됩니다. 전 세계적으로 신결석증 발병률이 증가하고 있으며, 특히 재발이 동반되는 사례가 증가하면서 치료 중재에 대한 수요 증가를 견인하고 있습니다. 이 질환의 재발성 특성으로 인해 즉각적인 치료와 지속적인 환자 관리가 모두 필요하며, 이로 인해 전 세계적으로 시행되는 의료 시술의 수가 크게 증가하고 있습니다. 또한, 진단 기술의 발전으로 의료진은 결석을 조기에 발견하고 결석의 정확한 위치를 보다 정확하게 파악할 수 있게 되었습니다. 영상 진단 능력의 향상은 보다 정밀한 치료 계획 수립을 가능하게 하여 임상 결과 개선에 기여하고 있습니다. 이러한 발전은 의사의 현대적 치료법에 대한 신뢰를 높이는 동시에 의료시설 전반의 시술 효율을 향상시키는 데 기여하고 있습니다.

미국의 신장 결석 관리 시장은 2025년 12억 달러에 달했습니다. 미국 내 신장 결석 질환의 높은 발병률은 수술적 치료와 예방적 치료 솔루션에 대한 안정적인 수요를 지속적으로 창출하고 있습니다. 환자의 상당수가 결석 재발을 경험하고 있으며, 지속적인 모니터링과 여러 가지 치료 중재가 필요합니다. 이러한 추세는 시장의 지속적인 호황과 첨단 의료 기술에 대한 수요 증가에 기여하고 있습니다. 미국은 또한 첨단 체외충격파쇄석기, 요관경 장비, 레이저 치료 기술을 갖춘 병원과 외래수술센터(ASC) 등 잘 정비된 의료 인프라의 혜택을 누리고 있습니다. 첨단 영상 진단 시스템에 대한 접근은 질병의 조기 발견과 치료 계획의 개선을 돕고 있습니다. 의료 서비스 제공업체들이 저침습적 기술에 대한 선호도가 높아지면서 의료 시스템 전반의 치료 효율성과 환자 처리 능력은 꾸준히 향상되고 있습니다.

Allengers,Becton, Dickinson and Company,Boston Scientific,Coloplast,COOK MEDICAL,DirexGroup,Dornier MedTech,ELMED Medical Systems,EMS ELECTRO MEDICAL SYSTEMS, KARL STORZ, MEDISPEC, OLYMPUS, PolyDiagnost, Richard Wolf, SIEMENS Healthineers 등 수많은 주요 기업들이 세계 신장결석 관리 시장에 진출해 있습니다. 세계 신장결석 치료 시장에서 사업을 전개하는 기업들은 시장에서의 입지를 강화하고 세계 사업 기반을 확대하기 위해 다양한 전략적 노력을 기울이고 있습니다. 주요 기업들은 시술의 정확성과 환자의 치료 결과를 향상시키는 기술적으로 진보된 치료 시스템을 도입하기 위해 연구개발에 많은 투자를 하고 있습니다. 또한, 많은 기업들이 향상된 영상 진단 기능, 디지털 연결성 및 첨단 레이저 기술을 의료기기에 통합하여 제품 혁신에 주력하고 있습니다. 의료 기관 및 기술 제공업체와의 전략적 제휴는 기업이 제품 개발을 가속화하고 임상 현장에서의 채택을 확대하는 데 도움이 되고 있습니다. 또한, 파트너십 및 판매 계약을 통해 신흥 의료 시장에 진출함으로써 기업들은 첨단 치료 솔루션에 대한 접근성을 확대할 수 있게 되었습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 결석 유형별, 2022-2035

제6장 시장 추산 및 예측 : 카테고리별, 2022-2035

제7장 시장 추산 및 예측 : 최종 용도별, 2022-2035

제8장 시장 추산 및 예측 : 지역별, 2022-2035

제9장 기업 개요

LSH 26.04.23The Global Kidney Stone Management Market was valued at USD 2.9 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 4.8 billion by 2035.

Growth in the kidney stone management market is supported by the increasing global incidence of kidney stone disorders, continuous advancements in treatment technologies, and the steady rise in the aging population. Healthcare providers are witnessing higher patient volumes associated with urinary tract disorders, which is intensifying the demand for reliable diagnostic tools and effective treatment solutions. Medical technology advancements are improving the accuracy of stone detection while also enhancing treatment efficiency and patient safety. Additionally, the shift toward minimally invasive therapeutic approaches is transforming the treatment landscape by offering shorter recovery times and reduced procedural risks. Hospitals and specialty clinics are increasingly adopting modern devices and advanced procedural techniques designed to improve clinical outcomes and optimize patient management. Furthermore, the integration of digital diagnostics and imaging technologies is enabling healthcare professionals to identify kidney stones earlier and plan more precise treatment strategies. Collectively, these developments are driving steady expansion of the kidney stone management market while improving the overall quality of patient care.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.9 Billion |

| Forecast Value | $4.8 Billion |

| CAGR | 4.9% |

Kidney stone management involves the identification, treatment, and long-term control of renal calculi through diagnostic imaging, medical therapy, and minimally invasive or surgical procedures. The primary objective of these interventions is to relieve symptoms, eliminate or break down stones, prevent recurrence, and restore normal urinary system function. Advancements in technologies used for ureteroscopy, laser-based stone fragmentation, extracorporeal shock wave lithotripsy, and percutaneous procedures have significantly enhanced treatment effectiveness. These improvements allow clinicians to perform procedures with greater precision while minimizing complications. The industry is also experiencing rapid growth as healthcare facilities expand their adoption of minimally invasive procedures and ambulatory surgical solutions.

The calcium oxalate segment held 75.7% share in 2025. The segment's leadership is largely attributed to the widespread occurrence of this type of kidney stone and its strong association with metabolic and dietary risk factors. Patients diagnosed with this condition often require repeated monitoring and medical intervention, which contributes to sustained demand for diagnostic and treatment solutions. Because this type of kidney stone frequently recurs, healthcare providers emphasize long-term management strategies that include dietary guidance, medical therapy, and routine monitoring. The high prevalence and recurrent nature of these stones, therefore, continue to support the growth of the calcium oxalate segment within the kidney stone management market.

The treatment segment generated USD 1.7 billion in 2025 and is expected to grow at a CAGR of 5.6% during 2026-2035. The increasing global incidence of kidney stone disease, particularly cases involving recurrence, is driving greater demand for therapeutic interventions. The recurring nature of the condition requires both immediate treatment procedures and continuous patient management, which significantly increases the volume of medical procedures performed worldwide. In addition, improvements in diagnostic technologies are enabling healthcare providers to detect stones at earlier stages and determine their exact location more accurately. Enhanced imaging capabilities support more precise treatment planning and improve clinical outcomes. These developments are increasing physician confidence in modern treatment methods while also contributing to higher procedural efficiency across healthcare facilities.

U.S. Kidney Stone Management Market reached USD 1.2 billion in 2025. The high occurrence of kidney stone disorders across the country continues to create consistent demand for both surgical procedures and preventive care solutions. A considerable portion of patients experience recurrent stone formation, which requires ongoing monitoring and multiple treatment interventions. This pattern contributes to sustained market activity and increased demand for advanced medical technologies. The United States also benefits from a well-developed healthcare infrastructure that includes hospitals and ambulatory surgical centers equipped with advanced lithotripsy systems, ureteroscopy devices, and laser-based treatment technologies. Access to sophisticated diagnostic imaging systems supports earlier disease detection and improved treatment planning. As healthcare providers continue to prioritize minimally invasive techniques, treatment efficiency and patient throughput are steadily improving across the healthcare system.

Several leading companies participate in the Global Kidney Stone Management Market, including Allengers, Becton, Dickinson and Company, Boston Scientific, Coloplast, COOK MEDICAL, DirexGroup, Dornier MedTech, ELMED Medical Systems, EMS ELECTRO MEDICAL SYSTEMS, KARL STORZ, MEDISPEC, OLYMPUS, PolyDiagnost, Richard Wolf, and SIEMENS Healthineers. Companies operating in the Global Kidney Stone Management Market are implementing a range of strategic initiatives to strengthen their market presence and expand their global footprint. Leading manufacturers are heavily investing in research and development to introduce technologically advanced treatment systems that enhance procedural precision and patient outcomes. Many firms are also focusing on product innovation by integrating improved imaging capabilities, digital connectivity, and advanced laser technologies into their medical devices. Strategic collaborations with healthcare institutions and technology providers are helping companies accelerate product development and broaden clinical adoption. Additionally, expansion into emerging healthcare markets through partnerships and distribution agreements is allowing companies to increase accessibility to advanced treatment solutions.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Stone type trends

- 2.2.3 Category trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence and recurrence rate of kidney stones

- 3.2.1.2 Technological advancements in minimally invasive treatments

- 3.2.1.3 Favourable reimbursement for lithotripsy procedures

- 3.2.1.4 Rising awareness regarding overall kidney health

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced treatment devices

- 3.2.2.2 Potential long-term adverse effects of lithotripsy

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Growth of telemedicine and remote patient monitoring

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Value chain analysis

- 3.11 Customer insights

- 3.12 Start-up scenarios

- 3.13 Gap analysis

- 3.14 Impact of AI and generative AI on the market

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Stone Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Calcium oxalate

- 5.3 Struvite

- 5.4 Uric acid

- 5.5 Calcium phosphate

- 5.6 Cysteine

Chapter 6 Market Estimates and Forecast, By Category, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Treatment

- 6.2.1 Extracorporeal shock wave lithotripsy (ESWL)

- 6.2.2 Ureteroscopy

- 6.2.3 Percutaneous nephrolithotomy (PCNL)

- 6.2.4 Other treatments

- 6.3 Diagnostics

- 6.3.1 Computed tomography

- 6.3.2 Ultrasound

- 6.3.3 Abdominal x-ray

- 6.3.4 Intravenous pyelography

- 6.3.5 Abdominal MRI

- 6.3.6 Other diagnostics

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Specialty clinics

- 7.4 Ambulatory surgical centers

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Allengers

- 9.2 Becton, Dickinson and Company

- 9.3 Boston Scientific

- 9.4 Coloplast

- 9.5 COOK MEDICAL

- 9.6 DirexGroup

- 9.7 Dornier MedTech

- 9.8 ELMED Medical Systems

- 9.9 EMS ELECTRO MEDICAL SYSTEMS

- 9.10 KARL STORZ

- 9.11 MEDISPEC

- 9.12 OLYMPUS

- 9.13 PolyDiagnost

- 9.14 Richard Wolf

- 9.15 SIEMENS Healthineers