|

시장보고서

상품코드

1998681

다리 및 발목용 의료기기 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Foot and Ankle Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

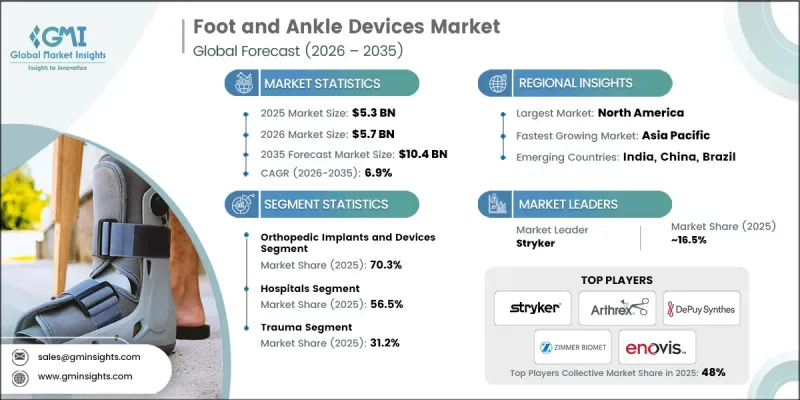

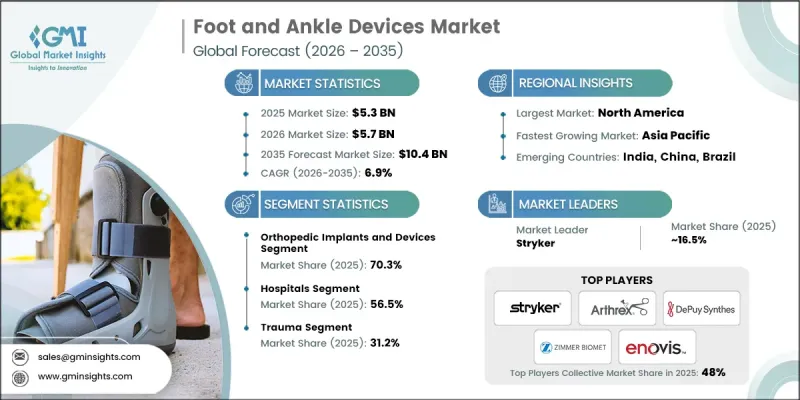

세계의 다리 및 발목용 의료기기 시장은 2025년에 53억 달러로 평가되었고, CAGR 6.9%로 성장하여 2035년까지 104억 달러에 달할 것으로 예측됩니다.

이 시장의 성장은 정형외과 질환의 유병률 증가, 외상 사례 증가, 발 및 발목용 의료기기 기술의 발전으로 인해 성장하고 있습니다. 당뇨병 환자 증가와 이에 따른 족부 합병증, 그리고 환자 맞춤형 임플란트 및 저침습 수술의 혁신적인 기술 개발이 결합되어 수요가 가속화되고 있습니다. 고령화 및 생활습관과 관련된 위험 요인도 발, 발목 질환 증가에 기여하고 있습니다. 또한, 전 세계적으로 교통사고와 고에너지 외상 사례가 증가함에 따라 골절, 인대 파열, 탈구 및 기타 하지 손상을 관리하는 의료기기에 대한 수요가 증가하고 있습니다. 재료 과학과 의료기기 공학의 발전을 포함한 기술 혁신은 환자의 치료 결과를 크게 개선하여 시장 확대를 더욱 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 53억 달러 |

| 예측액 | 104억 달러 |

| CAGR | 6.9% |

2025년에는 정형외과용 임플란트 및 의료기기 부문이 70.3%의 점유율을 차지했습니다. 이러한 성장은 3D 프린팅 정형외과용 임플란트의 채택과 외상, 변형 교정, 퇴행성 관절 질환에 대한 수술 건수 증가에 의해 주도되고 있습니다. 정형외과용 임플란트는 외상 고정, 관절 재건, 변형 교정을 포함한 발과 발목 질환의 외과적 치료에서 여전히 주요 치료 옵션으로 자리 잡고 있습니다. 하지 골절, 당뇨병 관련 족부 합병증, 노화에 따른 근골격계 퇴행, 스포츠 외상 발생률 증가가 세계 수요를 견인하고 있습니다.

외래수술센터(ASC) 부문은 2025년 13억 달러 규모에 달헀으며, 2026년부터 2035년까지 연평균 6.7%의 성장률을 보일 것으로 예측됩니다. ASC는 정형외과 수술과 최소침습수술이 외래진료로 전환되는 세계적인 흐름의 수혜를 받고 있습니다. 마취, 통증 관리, 수술 기구의 기술 발전으로 ASC는 외래에서 외반 모지 교정, 인대 재건, 고정 수술 등의 시술을 외래 환경에서 안전하게 시행할 수 있게 되어 시장 성장을 견인하고 있습니다.

미국 발 및 발목용 의료기기 시장은 2025년 26억 달러로 평가되었습니다. 이러한 성장은 환자 맞춤형 임플란트 개발, 잘 구축된 의료 인프라, 높은 수술 건수, 종합적인 보상 제도, 활발한 연구개발 활동, 그리고 접근하기 쉬운 정형외과 전문의의 존재가 뒷받침하고 있습니다. 또한 미국은 혁신의 선두주자로 발목관절 전치환 시스템, 첨단 고정용 나사, 인공연골 임플란트, 외고정 프레임 등의 신기술은 전 세계 상용화에 앞서 국내에서도 자주 발표되고 임상적으로 검증되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품별, 2022-2035

제6장 시장 추산 및 예측 : 용도별, 2022-2035

제7장 시장 추산 및 예측 : 최종 용도별, 2022-2035

제8장 시장 추산 및 예측 : 지역별, 2022-2035

제9장 기업 개요

LSH 26.04.23The Global Foot and Ankle Devices Market was valued at USD 5.3 billion in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 10.4 billion by 2035.

The market's growth is driven by the rising prevalence of orthopedic disorders, an increasing number of trauma cases, and advancements in foot and ankle device technologies. A growing diabetic population with related foot complications, coupled with the development of patient-specific implants and minimally invasive surgical innovations, is accelerating demand. Aging populations and lifestyle-related risk factors are also contributing to the rise in foot and ankle disorders. Furthermore, the global increase in road traffic accidents and high-impact trauma cases is boosting the need for devices that manage fractures, ligament tears, dislocations, and other lower extremity injuries. Technological innovation, including improvements in material science and device engineering, has significantly enhanced patient outcomes, further supporting market expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.3 Billion |

| Forecast Value | $10.4 Billion |

| CAGR | 6.9% |

The orthopedic implants and devices segment held 70.3% share in 2025. Growth is being fueled by the adoption of 3D-printed orthopedic implants and the high procedural volume for trauma, deformity correction, and degenerative joint conditions. Orthopedic implants remain the primary treatment option for surgical management of foot and ankle conditions, including trauma fixation, joint reconstruction, and deformity correction. Rising incidences of lower extremity fractures, diabetes-related foot complications, age-related musculoskeletal degeneration, and sports injuries are driving demand globally.

The ambulatory surgical centers (ASCs) segment was valued at USD 1.3 billion in 2025 and is expected to grow at a CAGR of 6.7% during 2026-2035. ASCs are benefiting from the global shift toward outpatient orthopedic surgeries and minimally invasive procedures. Technological advancements in anesthesia, pain management, and surgical instrumentation have enabled ASCs to perform procedures such as bunion corrections, ligament reconstructions, and fixation surgeries safely in outpatient settings, supporting market growth.

U.S. Foot and Ankle Devices Market was valued at USD 2.6 billion in 2025. Growth is supported by the development of patient-specific implants, well-established healthcare infrastructure, high procedure volumes, comprehensive reimbursement frameworks, robust R&D activities, and accessible orthopedic specialists. The U.S. is also a leader in innovation, with new technologies such as total ankle replacement systems, advanced fixation screws, synthetic cartilage implants, and external fixation frames often launched and clinically validated domestically before global commercialization.

Prominent companies in the Global Foot and Ankle Devices Market include Acumed LLC, Embla Medical Corporation, Enovis Corporation, Arthrex, Inc., Medartis, Smith & Nephew plc, Stryker Corporation, VILEX, LLC, Zimmer Biomet Holdings, Inc., DePuy Synthes (Johnson & Johnson), CONMED Corporation, Ottobock SE & Co KGaA, Fillauer LLC, and aap implantate AG. Companies in the Global Foot and Ankle Devices Market strengthen their position by investing heavily in R&D for patient-specific implants, advanced fixation systems, and minimally invasive solutions. They pursue strategic partnerships with hospitals, surgical centers, and orthopedic clinics to integrate their devices into standard care pathways. Expanding geographically into emerging markets helps tap into growing patient populations. Firms also focus on product differentiation through innovative materials, 3D printing, and smart implant technologies. Comprehensive after-sales support, physician training programs, and collaborations with research institutions further solidify their market presence and enhance brand credibility.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of orthopedic disorders

- 3.2.1.2 Rising incidence of trauma and road accidents

- 3.2.1.3 Technological advancements in foot and ankle devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of foot and ankle devices

- 3.2.2.2 Dearth of skilled healthcare professionals

- 3.2.3 Opportunities

- 3.2.3.1 Integration of digital health and smart orthotics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Reimbursement scenario

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.8 Consumer behavior analysis

- 3.9 Ring fixator competitive mapping, by company

- 3.10 Hexapod categories and technology differentiation

- 3.11 Price trends, by products

- 3.12 Gap analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.1.1 Stryker Corporation

- 4.1.2 DePuy Synthes (Johnson & Johnson)

- 4.1.3 Arthrex Inc.

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Orthopedic implants and devices

- 5.2.1 Joint implants

- 5.2.1.1 Ankle implants

- 5.2.1.2 Other joint implants

- 5.2.2 Fixation devices

- 5.2.2.1 Internal fixation devices

- 5.2.2.1.1 Plates

- 5.2.2.1.2 Screws

- 5.2.2.1.3 Fusion nails

- 5.2.2.1.4 Other internal fixation devices

- 5.2.2.2 External fixation devices

- 5.2.2.2.1 Ring fixation systems

- 5.2.2.2.2 Pin-to-bar systems

- 5.2.2.2.3 Hexapod systems

- 5.2.2.2.4 Other external fixators

- 5.2.2.1 Internal fixation devices

- 5.2.3 Soft tissue orthopedic devices

- 5.2.1 Joint implants

- 5.3 Bracing and support devices

- 5.3.1 Soft bracing & support devices

- 5.3.2 Hard braces & support devices

- 5.3.3 Hinged braces & support devices

- 5.4 Prostheses

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Trauma

- 6.3 Hammertoe

- 6.4 Osteoarthritis

- 6.5 Rheumatoid Arthritis

- 6.6 Neurological Disorders

- 6.7 Osteoporosis

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Orthopedic clinics

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 aap implantate AG

- 9.2 Acumed LLC

- 9.3 Arthrex, Inc.

- 9.4 CONMED Corporation

- 9.5 DePuy Synthes (Johnson & Johnson)

- 9.6 Embla Medical Corporation

- 9.7 Enovis Corporation

- 9.8 Fillauer LLC

- 9.9 Medartis

- 9.10 Orthofix Medical Inc.

- 9.11 Ottobock SE & Co KGaA

- 9.12 Smith & Nephew plc

- 9.13 Stryker Corporation

- 9.14 VILEX, LLC

- 9.15 Zimmer Biomet Holdings, Inc.