|

시장보고서

상품코드

1998687

배터리 열관리 시스템 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Battery Thermal Management System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

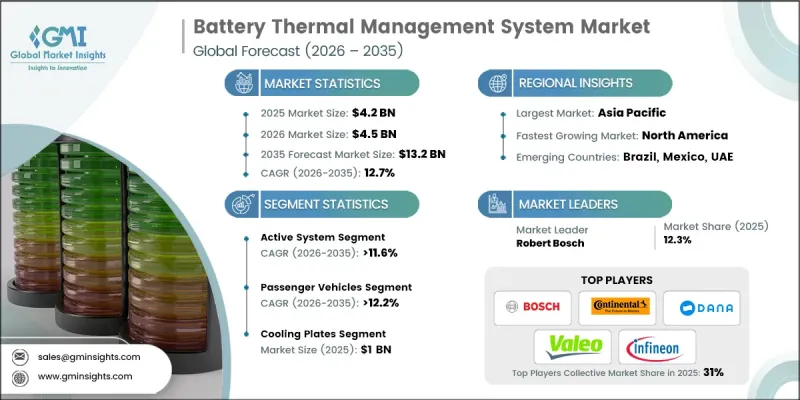

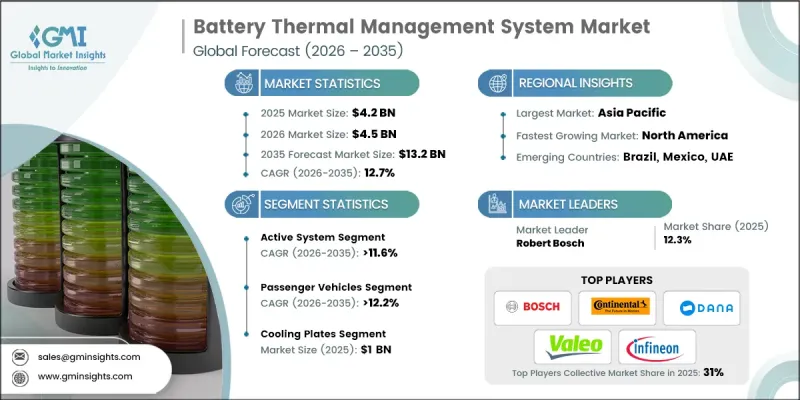

세계의 배터리 열관리 시스템 시장은 2025년에 42억 달러로 평가되었고, CAGR 12.7%로 성장하여 2035년까지 132억 달러에 달할 것으로 예측됩니다.

배터리 열관리 시스템 산업의 확대는 전기자동차의 보급 확대, 첨단 배터리 저장 기술에 대한 수요 증가, 배터리 작동에 대한 엄격한 안전 기준, 재생에너지 인프라의 급속한 발전으로 뒷받침되고 있습니다. 자동차 제조업체, 배터리 개발사, 에너지 저장 장치 공급업체들은 배터리 성능 향상, 수명 연장, 안전한 기능성을 보장하기 위해 첨단 열관리 솔루션에 많은 투자를 하고 있습니다. 전기 모빌리티의 급속한 확대, 대규모 배터리 저장 시설의 도입, 대용량 배터리 팩의 보급으로 효율적인 열관리 기술에 대한 수요가 더욱 증가하고 있습니다. 배터리 용량이 증가하고 전력 밀도가 높아짐에 따라 열화를 방지하고 안정적인 에너지 출력을 보장하기 위해서는 안정적인 작동 온도를 유지하는 것이 매우 중요합니다. 그 결과, 첨단 배터리 열관리 시스템은 현대의 에너지 저장 및 전기 이동성 생태계에서 필수적인 구성 요소로 자리 잡고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 42억 달러 |

| 예측액 | 132억 달러 |

| CAGR | 12.7% |

고성능 배터리 시스템의 온도 안정성 유지에 대한 요구가 증가함에 따라 다양한 산업 분야에서 보다 진보된 열관리 기술이 도입되고 있습니다. 제조업체와 시스템 통합사업자들은 효율적인 방열, 과열 위험 감소 및 에너지 효율을 향상시키는 솔루션에 점점 더 많은 관심을 기울이고 있습니다. 최신 배터리 열관리 시스템에는 실시간 온도 모니터링, 지능형 냉각 메커니즘, 열 환경 제어를 위해 설계된 고급 재료 등의 기능이 내장되어 있습니다. 냉각 아키텍처 개선, 지능형 모니터링 플랫폼, 통합 배터리 제어 기술 등의 최근 동향은 기존의 배터리 관리 방식을 혁신하고 운영 안전성과 신뢰성을 향상시키고 있습니다.

액티브 시스템 부문은 2025년 47%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 11.6%를 나타낼 것으로 예측됩니다. 이 부문은 배터리의 안전성, 효율성 및 작동 수명에 직접적인 영향을 미치는 최적의 배터리 온도를 능동적으로 유지하는 데 있어 매우 중요한 역할을 합니다. 전기자동차 및 에너지 저장 시스템에서 대용량 리튬 이온 배터리 및 차세대 배터리 기술의 채택이 확대됨에 따라, 안정적인 성능을 유지하기 위해 능동적 냉각 접근 방식이 필수적입니다. 이 시스템은 지속적인 온도 제어를 제공하고 에너지 효율을 향상시킵니다. 이는 전 세계 다양한 용도에서 배터리의 안정적인 작동을 보장하기 위해 매우 중요합니다.

승용차 부문은 2025년 76%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 12.2%로 성장할 것으로 추정됩니다. 이 부문의 견조한 실적은 주로 세계 전기차 및 하이브리드 승용차 생산 및 보급 확대에 기인합니다. 소비자와 제조업체는 배터리 효율 향상, 배터리 수명 연장, 열 안정성 강화, 일관된 차량 성능의 향상을 우선순위로 삼고 있습니다. 그 결과, 최적의 배터리 작동 조건을 유지하고 안정적인 차량 운행을 지원하기 위해 첨단 배터리 열관리 기술이 승용차에 광범위하게 적용되고 있습니다. 다양한 차량 카테고리에서 통합 배터리 열관리 시스템의 표준화가 진행됨에 따라 세계 시장에서의 선도적인 입지를 더욱 공고히 하고 있습니다.

중국의 배터리 열관리 시스템 시장은 55%의 점유율을 차지하며, 2025년에는 11억 8,800만 달러 규모에 도달할 것으로 예측됩니다. 강력한 전기자동차 제조 생태계와 잘 구축된 배터리 공급망 인프라를 바탕으로 배터리 열관리 시스템 산업에서 중요한 역할을 하고 있습니다. 주요 자동차 제조업체와 배터리 공급업체들이 이 지역에 첨단 열관리 솔루션의 개발 및 도입을 가속화하고 있습니다. 자동차 제조업체 및 기술 제공업체와의 긴밀한 협력을 통해 엄격한 에너지 효율 및 안전 규정을 준수하면서 배터리의 안전성, 운영 효율성 및 장기적인 성능을 지속적으로 개선하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 냉각 방식별, 2022-2035

제6장 시장 추산 및 예측 : 컴포넌트별, 2022-2035

제7장 시장 추산 및 예측 : 차량별, 2022-2035

제8장 시장 추산 및 예측 : 배터리별, 2022-2035

제9장 시장 추산 및 예측 : 추진력별, 2022-2035

제10장 시장 추산 및 예측 : 배터리 용량별, 2022-2035

제11장 시장 추산 및 예측 : 지역별, 2022-2035

제12장 기업 개요

LSH 26.04.23The Global Battery Thermal Management System Market was valued at USD 4.2 billion in 2025 and is estimated to grow at a CAGR of 12.7% to reach USD 13.2 billion by 2035.

Expansion within the battery thermal management system industry is supported by the growing adoption of electric vehicles, increasing demand for advanced battery storage technologies, strict safety standards for battery operation, and the rapid development of renewable energy infrastructure. Automotive manufacturers, battery developers, and energy storage providers are investing heavily in advanced thermal management solutions to improve battery performance, extend operational lifespan, and ensure safe functionality. The rapid expansion of electric mobility, large-scale battery storage installations, and high-capacity battery packs is further strengthening demand for efficient thermal management technologies. As battery capacity increases and power density rises, maintaining stable operating temperatures becomes critical for preventing degradation and ensuring reliable energy output. Consequently, advanced battery thermal management systems are becoming essential components in modern energy storage and electric mobility ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.2 Billion |

| Forecast Value | $13.2 Billion |

| CAGR | 12.7% |

The growing need to maintain temperature stability in high-performance battery systems is encouraging the deployment of more advanced thermal management technologies across multiple industries. Manufacturers and system integrators are increasingly focusing on solutions that enable efficient heat dissipation, reduce overheating risks, and enhance energy efficiency. Modern battery thermal management systems incorporate features such as real-time temperature monitoring, intelligent cooling mechanisms, and advanced materials designed to regulate thermal conditions. Recent technological developments, including improved cooling architectures, intelligent monitoring platforms, and integrated battery control technologies, are reshaping conventional battery management approaches while enhancing operational safety and reliability.

The active system segment held a 47% share in 2025, and it is expected to grow at a CAGR of 11.6% between 2026 and 2035. This segment plays a vital role in actively maintaining optimal battery temperatures, which directly influences battery safety, efficiency, and operational lifespan. With the increasing use of high-capacity lithium-ion and next-generation battery technologies in electric mobility and energy storage systems, active cooling approaches have become essential for maintaining consistent performance. These systems provide continuous temperature regulation and improve energy efficiency, which is critical for ensuring stable battery operation across various applications worldwide.

The passenger vehicles segment held 76% share in 2025, and it is estimated to grow at a CAGR of 12.2% during 2026-2035. The strong performance of this segment is largely attributed to the increasing production and adoption of electric and hybrid passenger vehicles globally. Consumers and manufacturers are prioritizing improved battery efficiency, longer battery lifespan, enhanced thermal stability, and consistent vehicle performance. As a result, advanced battery thermal management technologies are being widely integrated into passenger vehicles to maintain optimal battery operating conditions and support reliable vehicle operation. Increasing standardization of integrated battery thermal management systems across different vehicle categories is further strengthening the leadership of this segment across global markets.

China Battery Thermal Management System Market held a 55% share, generating USD 1,108.8 million in 2025. The country plays a significant role in the battery thermal management system industry due to its strong electric vehicle manufacturing ecosystem and well-established battery supply chain infrastructure. The presence of major automotive manufacturers and battery suppliers has accelerated the development and deployment of advanced thermal management solutions within the region. Close collaboration between automotive companies and technology providers continues to support improvements in battery safety, operational efficiency, and long-term performance while ensuring compliance with strict energy efficiency and safety regulations.

Major companies operating in the Global Battery Thermal Management System Market include Robert Bosch, Continental, BorgWarner, Denso, Valeo, Dana, MAHLE, Hanon Systems, Infineon Technologies, and Hitachi Astemo. Companies participating in the Global Battery Thermal Management System Market are implementing a range of strategic initiatives to strengthen their competitive position and expand their market presence. Leading manufacturers are investing significantly in research and development to introduce advanced thermal management technologies that improve energy efficiency and battery performance. Many companies are also forming strategic partnerships with automotive manufacturers and energy storage providers to accelerate the development of integrated battery solutions. Expanding production capacity and strengthening global supply chains are key priorities to meet growing demand from the electric mobility sector. Additionally, organizations are focusing on integrating intelligent monitoring systems and advanced cooling technologies into their product portfolios. Continuous innovation, strategic collaborations, and the development of next-generation battery management technologies are helping companies reinforce their foothold in the global battery thermal management system market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Cooling method

- 2.2.3 Component

- 2.2.4 Vehicle

- 2.2.5 Battery

- 2.2.6 Propulsion

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising EV Adoption

- 3.2.1.2 High-Capacity Battery Packs

- 3.2.1.3 Regulatory & Safety Standards

- 3.2.1.4 Technological Advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Cost

- 3.2.2.2 Integration Complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Commercial EV & Fleet Electrification

- 3.2.3.2 Energy Storage & Renewable Integration

- 3.2.3.3 Next-Generation Battery Technologies

- 3.2.3.4 Integration with AI and IoT

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: EPA, CARB, NHTSA Standards

- 3.4.1.2 Canada: Transport Canada, CMVSS 305

- 3.4.2 Europe

- 3.4.2.1 Germany: BMDV, Euro 6/7

- 3.4.2.2 France: Ministry of Transport, Euro 6/7

- 3.4.2.3 UK: Department for Transport, Euro 6/7

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport, EV Battery Compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China: MIIT, China 6/7 Standards

- 3.4.3.2 Japan: MLIT, JIS Regulations

- 3.4.3.3 South Korea: MOLIT, KS Emission Standards

- 3.4.3.4 India: MoRTH, BS6 Norms

- 3.4.4 Latin America

- 3.4.4.1 Brazil: DENATRAN, CONAMA Standards

- 3.4.4.2 Mexico: Ministry of Communications & Transport

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: RTA, ESMA Regulations

- 3.4.5.2 Saudi Arabia: Ministry of Transport, SASO

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-Plus)

- 3.8.3 Regional Price Variation Analysis

- 3.9 Cost breakdown analysis

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Impact of Artificial Intelligence (AI)

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 Predictive maintenance & fleet battery management AI

- 3.11.3 Automated BTMS design optimization

- 3.11.4 Supply chain AI for component demand forecasting

- 3.11.5 GenAI use cases & adoption roadmap by segment

- 3.11.5.1 Thermal module design generation

- 3.11.5.2 Battery performance optimization

- 3.11.5.3 Customer service chatbots & technical support

- 3.11.5.4 Marketing content creation

- 3.11.6 Risks, limitations & regulatory considerations

- 3.11.6.1 Data privacy in IoT-enabled BTMS

- 3.11.6.2 AI algorithm transparency requirements

- 3.11.6.3 Liability in AI-driven product failures

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Use case scenarios

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Cooling Method, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Active system

- 5.2.1 Liquid Cooling Systems

- 5.2.2 Refrigerant-Based Cooling Systems

- 5.2.3 Thermoelectric Cooling Systems

- 5.3 Passive system

- 5.3.1 Air Cooling Systems

- 5.3.2 Heat Sink-Based Systems

- 5.3.3 Natural Convection Systems

- 5.4 Hybrid system

- 5.4.1 Active Liquid + Passive PCM Integration

- 5.4.2 Air + Liquid Hybrid Systems

- 5.4.3 Multi-Mode Adaptive Systems

Chapter 6 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Cooling Plates

- 6.3 Heat Exchangers

- 6.4 Pumps & Compressors

- 6.5 Fans & Blowers

- 6.6 Thermal Sensors

- 6.7 Thermal Interface Materials

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchbacks

- 7.2.2 Sedans

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Medium commercial vehicles (MCV)

- 7.3.3 Heavy commercial vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Battery, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Lithium-ion battery

- 8.3 Nickel-Metal Hydride (NiMH) battery

- 8.4 Lead-acid battery

- 8.5 Solid-state battery

Chapter 9 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Battery Electric Vehicles (BEVs)

- 9.3 Plug-in Hybrid Electric Vehicles (PHEVs)

- 9.4 Hybrid Electric Vehicles (HEVs)

Chapter 10 Market Estimates & Forecast, By Battery Capacity, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 <100 KWH

- 10.3 100-200 KWH

- 10.4 200-500 KWH

- 10.5 >500 KWH

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Belgium

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 Singapore

- 11.4.6 South Korea

- 11.4.7 Vietnam

- 11.4.8 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Global Player

- 12.1.1 BorgWarner

- 12.1.2 Continental

- 12.1.3 Dana

- 12.1.4 Denso

- 12.1.5 Hanon Systems

- 12.1.6 Hitachi Astemo

- 12.1.7 Infineon Technologies

- 12.1.8 MAHLE

- 12.1.9 Robert Bosch

- 12.1.10 Valeo

- 12.2 Regional Player

- 12.2.1 Aisin Seiki

- 12.2.2 Borgers

- 12.2.3 Calsonic Kansei (KKC)

- 12.2.4 GKN Automotive

- 12.2.5 Inalfa Roof Systems

- 12.2.6 Magna International

- 12.2.7 Modine Manufacturing

- 12.2.8 Nidec

- 12.2.9 Thermo King

- 12.2.10 Webasto