|

시장보고서

상품코드

1998692

자동차용 HMI 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Human Machine Interface (HMI) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

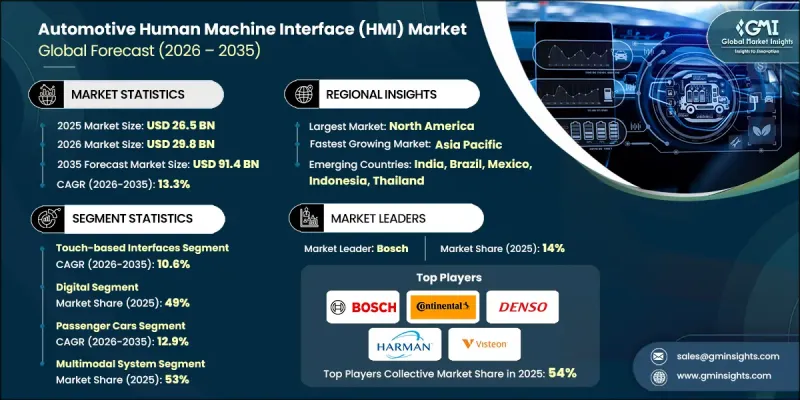

세계의 자동차용 HMI 시장은 2025년에 265억 달러로 평가되었고, CAGR 13.3%로 성장하여 2035년까지 914억 달러에 달할 것으로 예측됩니다.

시장 확대는 전기자동차 및 하이브리드 자동차의 보급이 확대되고 있는 것에 힘입은 바 큽니다. 이러한 차량에서는 차량 1대당 HMI 컨텐츠가 더 고급화되어야 합니다. 원활한 조작, 모바일 기기 같은 경험, 개인화된 인포테인먼트, 통합 음성 제어에 대한 소비자의 기대가 높아지면서 자동차 제조업체들은 첨단 디지털 콕핏 솔루션에 대한 투자를 늘리고 있습니다. 첨단운전자보조시스템(ADAS)와 증강현실(AR) 헤드업 디스플레이의 보급으로 HMI의 기능은 인포테인먼트의 틀을 넘어 안전에 중요한 통신 플랫폼으로 확대되고 있습니다. 무선 소프트웨어 업데이트, 클라우드 기반 서비스, 실시간 내비게이션을 지원하는 커넥티드카로 인해 HMI 시스템은 지속적인 수익을 창출하는 플랫폼으로 진화하고 있습니다. 대형 터치스크린 디스플레이, 에너지 관리 인터페이스, AI 기반 분석 기능에 대한 수요가 급증하면서 OEM과 공급업체 모두 프리미엄 차량부터 양산차까지 사용자 참여도를 높이고 차별화를 꾀할 수 있는 기회가 생기고 있습니다. 전반적으로 이 시장은 기술 혁신, 전기차 보급 확대, 직관적이고 커넥티드한 운전 경험을 원하는 소비자 수요가 결합되어 형성되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 265억 달러 |

| 예측액 | 914억 달러 |

| CAGR | 13.3% |

터치 인터페이스 부문은 38%의 점유율을 차지하고 있으며, 2035년까지 연평균 복합 성장률(CAGR) 10.6%를 나타낼 것으로 예측됩니다. 이러한 인터페이스는 물리적 버튼을 사용하지 않고 인포테인먼트, 공조, 차량 시스템을 제어하는 대형, 고해상도, 햅틱 기능을 갖춘 스크린으로 진화하여 직관적인 사용자 경험을 제공합니다.

디지털 부문은 2025년 49%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 14%로 성장할 것으로 전망됩니다. 디지털 HMI에는 터치스크린 패널, 소프트웨어 기반 디스플레이, 구성 가능한 계기판 클러스터가 포함되며, 운전자는 이를 통해 조종석을 개인화하고, 실시간 데이터에 액세스하고, IoT 용도를 통합하고, 무선 업데이트를 수신할 수 있습니다. 무선 업데이트를 받을 수 있습니다.

미국의 자동차 휴먼 머신 인터페이스(HMI) 시장은 2025년 74억 달러에 달할 것으로 예측됩니다. 각 지역 거점들은 AI 기반 조종석 솔루션, AR 헤드업 디스플레이(HUD), 전기차, 차량 관리, 첨단 인포테인먼트에 최적화된 커넥티드 디지털 인터페이스의 보급을 주도하고 있습니다. 대형 차량에 대한 소비자의 강력한 수요는 멀티스크린 대시보드, 차량당 HMI 탑재량 증가, 차량 내 커넥티비티 확대, 특히 프리미엄 및 전기 SUV와 트럭에 대한 수요를 견인하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 기술별, 2022-2035

제6장 시장 추산 및 예측 : 인터페이스별, 2022-2035

제7장 시장 추산 및 예측 : 용도별, 2022-2035

제8장 시장 추산 및 예측 : 차종별, 2022-2035

제9장 시장 추산 및 예측 : 컴포넌트별, 2022-2035

제10장 시장 추산 및 예측 : 액세스별, 2022-2035

제11장 시장 추산 및 예측 : 지역별, 2022-2035

제12장 기업 개요

LSH 26.04.23The Global Automotive Human Machine Interface Market was valued at USD 26.5 billion in 2025 and is estimated to grow at a CAGR of 13.3% to reach USD 91.4 billion by 2035.

Market expansion is driven by the increasing adoption of electric and hybrid vehicles, which demand more sophisticated HMI content per vehicle. Rising consumer expectations for seamless interaction, mobile device-like experiences, personalized infotainment, and integrated voice controls are pushing automakers to invest heavily in advanced digital cockpit solutions. The growth of advanced driver assistance systems and augmented reality head-up displays has expanded HMI functions beyond infotainment to safety-critical communication platforms. Connected vehicles that support over-the-air software updates, cloud-based services, and real-time navigation are enabling HMI systems to evolve into recurring revenue platforms. The surge in demand for larger touchscreen displays, energy management interfaces, and AI-driven analytics has created opportunities for both OEMs and suppliers to enhance user engagement and differentiation across premium and mass-market vehicles. Overall, the market reflects a combination of technological innovation, rising EV adoption, and consumer demand for intuitive, connected driving experiences.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $26.5 Billion |

| Forecast Value | $91.4 Billion |

| CAGR | 13.3% |

The touch-based interfaces segment held 38% share and is expected to grow at a CAGR of 10.6% through 2035. These interfaces are evolving into large, high-resolution, haptic-enabled screens that control infotainment, climate, and vehicle systems without physical buttons, offering an intuitive user experience.

The digital segment held a 49% share in 2025 and is projected to grow at a CAGR of 14% from 2026 to 2035. Digital HMIs include touchscreen panels, software-driven displays, and configurable instrument clusters that allow drivers to personalize their cockpit, access real-time data, integrate IoT applications, and receive over-the-air updates.

U.S. Automotive Human Machine Interface Market reached USD 7.4 billion in 2025. Regional hubs drive adoption of AI-enabled cockpit solutions, AR HUDs, and connected digital interfaces tailored to EVs, fleet management, and advanced infotainment. Strong consumer preference for larger vehicles supports multi-screen dashboards, high HMI content per vehicle, and expanded in-cabin connectivity, particularly for premium and electric SUVs and trucks.

Key players in the Global Automotive Human Machine Interface Market include Alpine, Bosch, Continental, Denso, Harman, LG Display, Nippon Seiki, Panasonic, Valeo, and Visteon. Companies in the Automotive Human Machine Interface Market strengthen their market position by continuously innovating advanced cockpit solutions and investing in AI, augmented reality, and connected vehicle technologies. OEMs and suppliers form strategic partnerships to integrate HMI systems with cloud platforms, EV architectures, and telematics. Expanding R&D capabilities enables the development of high-resolution, customizable interfaces and multi-screen dashboards. Companies also focus on software updates and over-the-air services to create recurring revenue streams while enhancing user experience. Entering new regional markets, building alliances with fleet operators, and offering modular HMI solutions for multiple vehicle platforms further reinforce their presence and competitive advantage.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Interface

- 2.2.4 Application

- 2.2.5 Vehicle

- 2.2.6 Component

- 2.2.7 Access

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Vehicle electrification (EV / Hybrid Growth)

- 3.2.1.2 ADAS & autonomous integration

- 3.2.1.3 Consumer demand for premium UX

- 3.2.1.4 Connected vehicle ecosystem

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development & integration cost

- 3.2.2.2 Driver distraction & regulatory restrictions

- 3.2.3 Market opportunities

- 3.2.3.1 Software-defined vehicle (SDV) architecture

- 3.2.3.2 Augmented reality (AR) head-up displays

- 3.2.3.3 AI & generative voice assistants

- 3.2.3.4 Emerging market digitalization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 NHTSA - National Highway Traffic Safety Administration

- 3.4.1.2 Transport Canada

- 3.4.2 Europe

- 3.4.2.1 UNECE - United Nations Economic Commission for Europe (WP.29)

- 3.4.2.2 Euro NCAP - European New Car Assessment Programme

- 3.4.3 Asia Pacific

- 3.4.3.1 AIS - Automotive Industry Standards Committee (India)

- 3.4.3.2 KAMA - Korea Automobile Manufacturers Association

- 3.4.4 Latin America

- 3.4.4.1 ANFAVEA - Associacao Nacional dos Fabricantes de Veiculos Automotores

- 3.4.4.2 IMT - Instituto Mexicano del Transporte

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Standardization Organization (GSO)

- 3.4.5.2 NRF - National Roads Fund (South Africa)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Pricing analysis (Driven by primary research)

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use cases

- 3.13 AI & generative AI future impact assessment

- 3.13.1 AI Disruption in Automotive HMI

- 3.13.2 Generative AI Use Cases

- 3.13.3 Strategic Market Implications

- 3.14 Strategic recommendations

- 3.14.1 OEM adoption roadmap for next-gen HMI

- 3.14.2 Tier-1/Tier-2 supplier investment strategies

- 3.14.3 Regulatory compliance & global alignment

- 3.14.4 AI & GenAI adoption plan for competitive advantage

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Touch-based interfaces

- 5.3 Voice control systems

- 5.4 Gesture recognition

- 5.5 Augmented reality displays

- 5.6 Haptic feedback systems

Chapter 6 Market Estimates & Forecast, By Interface, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Physical

- 6.3 Digital

- 6.4 Multimodal

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Infotainment

- 7.3 Navigation

- 7.4 Driver assistance

- 7.5 Climate control

- 7.6 Vehicle diagnostics

- 7.7 Connectivity services

- 7.8 Driver monitoring

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Passenger car

- 8.2.1 Hatchback

- 8.2.2 SUV

- 8.2.3 Sedan

- 8.3 Commercial vehicle

- 8.3.1 LCV

- 8.3.2 MCV

- 8.3.3 HCV

Chapter 9 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Hardware

- 9.2.1 Display & control supporting hardware

- 9.2.2 Sensors & actuators

- 9.2.3 Integration devices

- 9.3 Software

- 9.3.1 HMI Operating Systems & Middleware

- 9.3.2 Interaction Processing Software

- 9.3.3 UI & Graphics Software

- 9.3.4 Diagnostics & Monitoring Software

- 9.4 Services

- 9.4.1 Design & integration services

- 9.4.2 Maintenance & support

- 9.4.3 Customization & deployment

Chapter 10 Market Estimates & Forecast, By Access, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 Single-modal systems

- 10.3 Multimodal systems

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Nordics

- 11.3.7 Russia

- 11.3.8 Poland

- 11.3.9 Romania

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Vietnam

- 11.4.7 Indonesia

- 11.4.8 Philippines

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 Bosch

- 12.1.2 Continental

- 12.1.3 Denso

- 12.1.4 Harman International (Samsung)

- 12.1.5 Hyundai Mobis

- 12.1.6 LG Display

- 12.1.7 Marelli

- 12.1.8 Panasonic Automotive

- 12.1.9 Valeo

- 12.1.10 Visteon

- 12.2 Regional players

- 12.2.1 Alps Alpine

- 12.2.2 BlackBerry QNX

- 12.2.3 Cerence

- 12.2.4 Ficosa

- 12.2.5 Japan Display

- 12.2.6 Nippon Seiki

- 12.2.7 Sharp

- 12.2.8 Yazaki

- 12.3 Emerging players

- 12.3.1 AU Optronics (AUO)

- 12.3.2 Elektrobit

- 12.3.3 Preh

- 12.3.4 Rightware