|

시장보고서

상품코드

1998693

리소 라미네이트 포장 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Litho Laminated Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

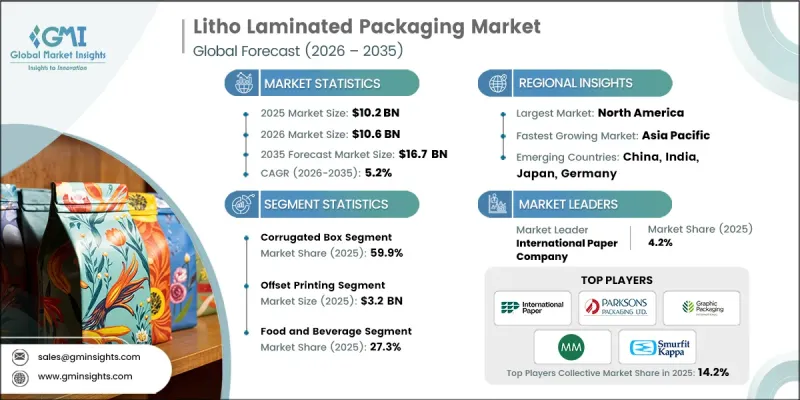

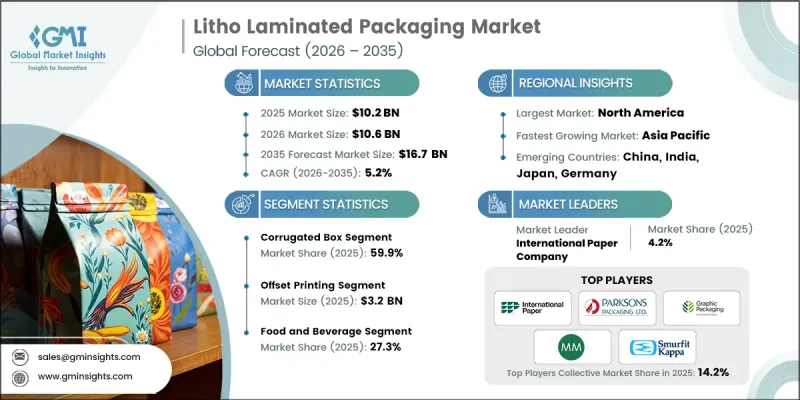

세계의 리소 라미네이트 포장 시장은 2025년에 102억 달러로 평가되었고, CAGR 5.2%로 성장하여 2035년까지 167억 달러에 달할 것으로 예측됩니다.

리소 라미네이트 포장 시장의 성장은 소매 업계의 트렌드 변화, 고급 제품 진열에 대한 수요 증가, 여러 소비재 산업에서 시각적으로 매력적인 포장의 중요성 증가 등에 의해 크게 뒷받침되고 있습니다. 포장은 기업이 자사 제품을 차별화하고 브랜드 아이덴티티를 소비자에게 효과적으로 전달할 수 있는 매우 중요한 브랜딩 요소로 자리 잡았습니다. 조직화된 소매업과 현대적 유통 채널이 전 세계적으로 확대됨에 따라 기업들은 내구성과 강력한 시각적 효과를 겸비한 포장 형태에 대한 의존도가 높아지고 있습니다. 디지털 소매 채널과 직송 모델의 성장도 포장 요구 사항에 영향을 미치고 있습니다. 기업들은 매력적인 브랜딩을 유지하면서 운송 중 제품을 보호할 수 있는 솔루션을 찾고 있기 때문입니다. 동시에 지속가능성에 대한 고려는 포장의 혁신을 형성하고 있으며, 구조적 강도와 환경적 책임의 균형을 맞춘 재활용 가능한 섬유 기반 구조의 채택을 촉진하고 있습니다. 리소 라미네이트 포장은 고품질 그래픽과 내구성이 뛰어난 골판지 소재를 결합하여 제품 보호와 매장 내 가시성을 높이고자 하는 기업에게 효과적인 솔루션이 될 수 있습니다. 이러한 요인들이 복합적으로 작용하여 세계 리소 라미네이트 포장 시장의 지속적인 확장을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 102억 달러 |

| 예측액 | 167억 달러 |

| CAGR | 5.2% |

소매업체와 제품 제조업체가 제품 프레젠테이션과 브랜드 커뮤니케이션을 강화하는 포장에 점점 더 많은 관심을 기울이면서 리소그래피 라미네이션 포장 시장은 계속 성장하고 있습니다. 현대의 소매 환경에서는 유통 및 취급 과정에서 구조적 신뢰성을 유지하면서 소비자의 관심을 끌 수 있는 패키징 솔루션이 요구되고 있습니다. 리소그래피 라미네이팅 기술을 통해 골판지에 고해상도 인쇄 그래픽을 적용할 수 있어 선명한 색상, 정교한 디테일, 고급스러운 시각적 마감을 구현할 수 있습니다. 이러한 시각적 품질과 물리적 내구성의 조합은 소매 환경에서 제품의 가시성을 높이고 브랜드 인지도를 높이는 데 기여합니다. 동시에 온라인 소매 및 직송 채널의 급속한 성장에 따라 배송 중 보호 성능과 시각적 매력을 모두 갖춘 포장 형태에 대한 수요가 증가하고 있습니다. 특히, 제품 프레젠테이션이 여전히 중요한 요소인 디지털 커머스 환경에서 패키지는 고객 경험의 중요한 부분으로 자리 잡았습니다.

2025년에는 골판지 상자 부문이 59.9%의 점유율을 차지했습니다. 골판지 상자는 우수한 구조적 특성, 적재 강도 및 효율적인 운송 능력으로 인해 여전히 선호되는 포장 솔루션입니다. 이 디자인은 더 무거운 하중을 지탱하고 대규모 유통 네트워크에 따른 취급 요구 사항을 견딜 수 있도록 설계되었습니다. 또한, 정교하게 인쇄된 라이너 보드와 골판지 소재를 결합하여 제조업체는 구조적 내구성과 시각적으로 매력적인 그래픽을 동시에 구현할 수 있습니다. 이러한 특성으로 인해 기업은 골판지 상자를 제품 운송과 소매 디스플레이에 모두 활용할 수 있습니다. 대량 유통에 대응하면서도 강력한 브랜딩 능력을 유지할 수 있는 이러한 포장 형태의 특성은 리소 라미네이트 포장 시장에서 그 중요성을 더욱 확고히할 것입니다.

오프셋 인쇄 부문은 2025년 32억 달러 시장 규모를 기록했습니다. 오프셋 인쇄 기술은 대량 생산에서도 고화질의 인쇄 품질과 일관된 색 재현을 실현할 수 있기 때문에 계속해서 견고한 입지를 유지하고 있습니다. 이 인쇄 방식은 패키지 제품의 시각적 매력을 높이는 복잡한 디자인 요소와 고급스러운 마감 효과에 대응할 수 있습니다. 대규모 오프셋 라미네이팅 공정과의 호환성으로 인해 오프셋 인쇄는 여전히 고품질 이차 포장 및 소매 디스플레이 솔루션 생산에 널리 사용되고 있습니다. 또한, 제조업체들은 대량 생산 시 비용 효율성이 높기 때문에 이 인쇄 기술을 선호하고 있으며, 일관된 품질 기준으로 시각적으로 인상적인 패키지를 원하는 기업에게 신뢰할 수 있는 선택이 되고 있습니다.

2025년 북미 리소 라미네이트 포장 시장은 35.7%의 점유율을 차지했습니다. 이 지역 시장은 조직화된 소매 환경과 통합된 유통 네트워크에서 고품질 소매 포장에 대한 수요가 증가함에 따라 시장이 확대되고 있습니다. 북미에서 사업을 전개하는 기업들은 경쟁이 치열한 소매 환경에서 제품의 가시성을 높이기 위해 내구성과 고도의 그래픽 표현을 겸비한 패키지 형태를 중요시하고 있습니다. 이 지역은 라미네이트 포장재의 대규모 제조 및 유통을 지원하는 잘 구축된 골판지 포장 인프라의 혜택을 누리고 있습니다. 미국과 캐나다의 포장 가공업체들은 생산 효율을 높이고 재료 폐기물을 줄이기 위해 첨단 제조 기술에 대한 투자를 확대되고 있습니다. 이러한 기술 발전은 제조업체의 운영 역량을 강화하는 동시에 지역 전체의 지속 가능한 포장 관행을 지원하는 데 도움이 되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별, 2022-2035

제6장 시장 추산 및 예측 : 플룻 유형별, 2022-2035

제7장 시장 추산 및 예측 : 인쇄 기술별, 2022-2035

제8장 시장 추산 및 예측 : 최종 이용 산업별, 2022-2035

제9장 시장 추산 및 예측 : 지역별, 2022-2035

제10장 기업 개요

LSH 26.04.23The Global Litho Laminated Packaging Market was valued at USD 10.2 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 16.7 billion by 2035.

Growth of the litho laminated packaging market is strongly supported by evolving retail dynamics, increasing demand for premium product presentation, and the rising importance of visually appealing packaging across multiple consumer industries. Packaging has become a crucial branding element that enables companies to differentiate their products and effectively communicate their brand identity to consumers. As organized retail and modern distribution channels expand globally, businesses increasingly rely on packaging formats that combine durability with strong visual impact. The growth of digital retail channels and direct shipping models is also influencing packaging requirements, as companies seek solutions that protect products during transit while maintaining attractive branding. At the same time, sustainability considerations are shaping packaging innovation, encouraging the adoption of recyclable fiber-based structures that balance structural integrity with environmental responsibility. Litho laminated packaging offers the advantage of combining high-quality graphics with durable corrugated materials, making it an effective solution for companies aiming to enhance both product protection and shelf visibility. These factors collectively support the continued expansion of the global litho laminated packaging market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.2 Billion |

| Forecast Value | $16.7 Billion |

| CAGR | 5.2% |

The litho laminated packaging market continues to gain momentum as retailers and product manufacturers place greater emphasis on packaging that enhances product presentation and brand communication. Modern retail environments require packaging solutions capable of attracting consumer attention while maintaining structural reliability throughout distribution and handling processes. Lithographic lamination technology allows high-resolution printed graphics to be applied to corrugated boards, enabling vibrant colors, refined detailing, and premium visual finishes. This combination of visual quality and physical durability strengthens product visibility in retail environments and supports stronger brand recognition. At the same time, the rapid growth of online retail and direct shipping channels has created demand for packaging formats that offer both protective strength and visual appeal during delivery. Packaging has become an important part of the customer experience, especially in digital commerce environments where product presentation remains critical.

The corrugated box segment accounted for 59.9% share in 2025. Corrugated boxes remain a preferred packaging solution due to their strong structural properties, stacking strength, and efficient transportation capabilities. Their design allows them to support heavier loads and withstand the handling demands associated with large-scale distribution networks. In addition, the integration of finely printed linerboards with corrugated materials enables manufacturers to combine structural durability with visually appealing graphics. This feature allows companies to use corrugated boxes for both product transportation and retail display purposes. The ability of these packaging formats to support large-volume distribution while maintaining strong branding capabilities ensures their continued importance in the litho laminated packaging market.

The offset printing segment generated USD 3.2 billion in 2025. Offset printing technology continues to maintain a strong position due to its ability to deliver high-definition print quality and consistent color reproduction across large production volumes. The printing method supports intricate design elements and premium finishing effects that enhance the visual appeal of packaging products. Because of its compatibility with large-scale lithographic lamination processes, offset printing remains widely adopted for producing high-quality secondary packaging and retail display solutions. Manufacturers also favor this printing technology for its cost efficiency when operating at high production volumes, making it a reliable option for companies seeking visually striking packaging with consistent quality standards.

North America Litho Laminated Packaging Market accounted for 35.7% share in 2025. The market in this region is expanding due to increasing demand for high-quality retail packaging across organized retail environments and integrated distribution networks. Businesses operating in North America are placing strong emphasis on packaging formats that combine durability with advanced graphic presentation to improve product visibility in competitive retail settings. The region benefits from a well-established corrugated packaging infrastructure that supports large-scale manufacturing and distribution of laminated packaging materials. Packaging converters across the United States and Canada are increasingly investing in advanced manufacturing technologies designed to improve production efficiency and reduce material waste. These technological improvements are helping manufacturers enhance operational capacity while supporting sustainable packaging practices across the region.

Key companies operating in the Global Litho Laminated Packaging Market include Smurfit Kappa Group, International Paper Company, Graphic Packaging International, LLC, Mayr-Melnhof Karton AG, Greif, Inc., Accurate Box Company, Inc., Parksons Packaging Ltd., Brandon Packaging, LLC, Frankston Packaging, LGR Packaging, Infinity Packaging Solutions, Jaymar Packaging Ltd., Platypus Print Packaging, PM Packaging, SK Offset, Shanghai DE Printed Box, Alliance Packaging, and The Cardboard Box Company. Companies participating in the Global Litho Laminated Packaging Market are implementing several strategies to strengthen their competitive position and expand their global footprint. Many manufacturers are investing in advanced lamination technologies and automated production lines to improve operational efficiency and maintain consistent product quality. Expanding sustainable packaging solutions has also become a major strategic priority, with companies developing recyclable fiber-based materials and lightweight structures that reduce environmental impact. Strategic partnerships with consumer goods companies and retail brands allow packaging providers to develop customized packaging formats tailored to specific branding and distribution needs. Businesses are also focusing on enhancing printing capabilities and graphic finishing technologies to meet the growing demand for visually impactful packaging.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Flute type trends

- 2.2.3 Printing technology trends

- 2.2.4 End-use industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Premium shelf-appeal demand in retail packaging

- 3.2.1.2 E-commerce growth requiring durable branded cartons

- 3.2.1.3 Expansion of quick-service restaurant chains globally

- 3.2.1.4 Shift toward recyclable corrugated-based packaging

- 3.2.1.5 Retail-ready packaging adoption by supermarkets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatile kraft liner and fluting prices

- 3.2.2.2 Competition from digitally printed corrugated

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in sustainable fiber-based packaging

- 3.2.3.2 Custom litho-laminated e-commerce shipper boxes

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Corrugated box

- 5.3 Cartons

Chapter 6 Market Estimates and Forecast, By Flute Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 B Flute

- 6.3 C Flute

- 6.4 E Flute

- 6.5 F Flute

- 6.6 BC Flute

- 6.7 BE Flute

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Printing Technology, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Offset printing

- 7.3 Flexographic printing

- 7.4 Gravure printing

- 7.5 Digital printing

Chapter 8 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Food and beverage

- 8.3 Pharmaceutical and healthcare

- 8.4 Consumer goods

- 8.5 Industrial packaging

- 8.6 Electronics and electrical

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 International Paper Company

- 10.1.2 Smurfit Kappa Group

- 10.1.3 Graphic Packaging International, LLC

- 10.1.4 Mayr-Melnhof Karton AG

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Accurate Box Company, Inc.

- 10.2.1.2 Brandon Packaging, LLC

- 10.2.1.3 Frankston Packaging

- 10.2.1.4 Infinity Packaging Solutions

- 10.2.1.5 Grief, Inc.

- 10.2.1.6 The Cardboard Box Company

- 10.2.2 Asia Pacific

- 10.2.2.1 Parksons Packaging Ltd.

- 10.2.2.2 Shanghai DE Printed Box

- 10.2.2.3 SK Offset

- 10.2.2.4 PM Packaging

- 10.2.3 Europe

- 10.2.3.1 Jaymar Packaging Ltd

- 10.2.3.2 LGR Packaging

- 10.2.3.3 ALLIANCE PACKAGING

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Platypus Print Packaging