|

시장보고서

상품코드

1998698

자동차 제어 케이블 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Control Cables Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

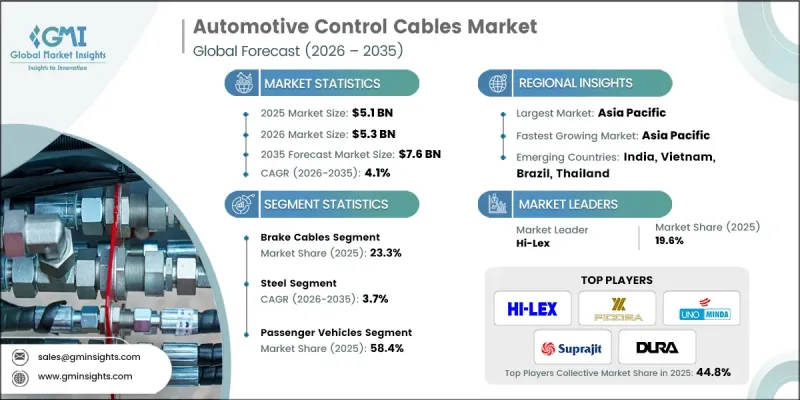

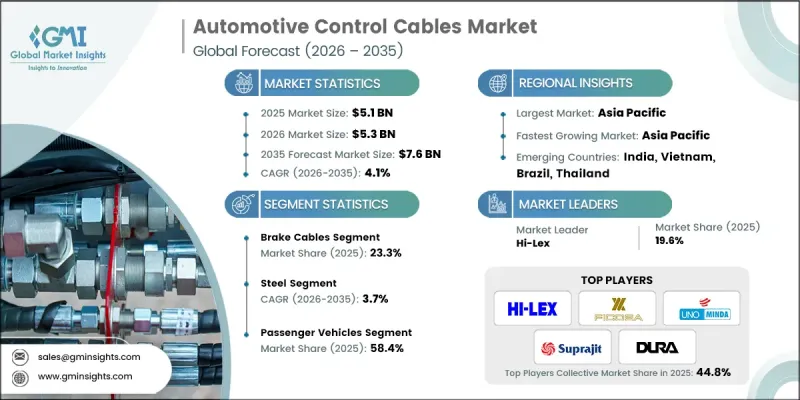

세계의 자동차 제어 케이블 시장은 2025년에 51억 달러로 평가되었고, CAGR 4.1%로 성장하여 2035년까지 76억 달러에 달할 것으로 예측됩니다.

차량의 전동화 전환이 진행되고 있음에도 불구하고 자동차 제어 케이블에 대한 수요는 안정적으로 유지되고 있습니다. 이는 다양한 기계 시스템에서 작동 기능을 실현하기 위해 여전히 케이블 기반 메커니즘이 필요하기 때문입니다. 전기 구동 시스템을 갖춘 차량이라도 일관된 움직임과 기능을 달성하기 위해 일부 내부 기계 작동은 여전히 제어 케이블 시스템에 의존하고 있습니다. 신차 생산과 더불어 전 세계적으로 노후화된 차량군도 교체 부품 수요를 유지하는 데 중요한 역할을 하고 있습니다. 2023년, 전 세계에서 운행되는 차량의 평균 차령은 12년 이상이며, 이는 제어 케이블과 같은 기계 부품의 마모율 상승의 한 원인이 되고 있습니다. 차량 운행 기간이 길어짐에 따라 선진국과 개발도상국 자동차 시장을 막론하고 유지보수 및 교체 작업의 중요성이 커지고 있습니다. 그 결과, 성숙 시장에서 자동차 제어 케이블 총 매출의 약 40%를 교체용 부품이 차지하고 있으며, 세계 자동차 제어 케이블 시장에서 OEM(순정 부품) 수요와 함께 애프터마켓 부문의 중요성이 더욱 커지고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 금액 | 51억 달러 |

| 예측 금액 | 76억 달러 |

| CAGR | 4.1% |

자동차 산업에서 첨단 전자식 변속기 기술 및 디지털 제어 시스템의 도입이 점차 진행되고 있지만, 수동 변속기 탑재 차량은 여전히 세계 자동차 생산에서 중요한 점유율을 유지하고 있습니다. 2024년에는 수동 변속기를 장착한 차량이 전 세계 총 생산량의 30%에 육박할 것으로 예측됩니다. 이러한 지속적인 존재감은 승용차 및 소형 상용차 카테고리 전반에 걸쳐 클러치 및 기어 제어 케이블에 대한 안정적인 수요를 뒷받침하고 있습니다. 차량의 전자화 및 자동화 시스템의 발전이 부품 설계에 영향을 미치고 있지만, 이러한 발전으로 인해 자동차 부문에서 필요한 제어 케이블의 총량이 크게 감소할 것으로 예상되지는 않습니다.

브레이크 케이블 부문은 2025년 23.3%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 5%를 나타낼 것으로 예측됩니다. 브레이크 케이블 시스템은 차량 안전 메커니즘의 기본 구성 요소로, 전 세계 승용차 및 상용차 카테고리에서 그 중요성이 계속되고 있음을 입증하고 있습니다. 차량 안전 표준에 초점을 맞춘 규제 프레임워크는 내구성이 뛰어난 제어 케이블을 필요로 하는 신뢰할 수 있는 브레이크 시스템에 대한 안정적인 수요에 기여하고 있습니다. 순정 부품으로서 수요 외에도, 브레이크 케이블은 일상적인 차량 운행으로 인해 자주 마모되기 때문에 차량 수명주기 동안 교체 부품의 필요성이 증가합니다. 그 결과, 브레이크 케이블 시스템은 자동차 제어 케이블 시장에서 OEM 및 애프터마켓 부문에서 판매되는 제어 케이블의 총량에 크게 기여하고 있습니다.

재료 유형별로는 철강 부문이 2025년 44.6%의 점유율을 차지했으며며, 2026년부터 2035년까지 연평균 3.7%의 성장률을 보일 것으로 예측됩니다. 스틸 케이블은 신뢰할 수 있는 기계적 동작을 유지하기 위해 높은 인장 성능과 높은 하중 지지력을 필요로 하는 자동차 용도에서 여전히 널리 선호되고 있습니다. 이러한 특성은 장기간에 걸친 작동 주기 동안 내구성과 일관된 성능이 요구되는 차량 시스템에서 특히 중요합니다. 또한, 스틸 케이블은 기계적 스트레스와 환경 조건에 대한 높은 내성을 보여 다양한 차량 플랫폼에서 장기간 사용하기에 적합합니다. 자동차 제조업체들은 신뢰성과 성능 특성으로 인해 여러 자동차 부문에 걸친 대규모 차량 생산에서 스틸 제어 케이블에 지속적으로 의존하고 있습니다.

중국의 자동차 제어 케이블 시장은 53%의 점유율을 차지하고 있으며, 2025년에는 14억 달러 규모에 도달했습니다. 중국은 방대한 자동차 생산 능력과 대규모 차량 보유량을 바탕으로 자동차 제조의 중요한 거점 역할을 하고 있습니다. 승용차, 상용차, 이륜차 부문에서의 높은 생산량은 순정(OEM) 제어 케이블 시스템에 대한 지속적인 수요를 뒷받침하고 있습니다. 또한, 차량 대수의 지속적인 증가는 애프터마켓용 교체 부품에 대한 큰 수요를 창출하고 있습니다. 인구 밀도가 높은 도시나 교외에서 주행하는 차량은 자주 출발과 정지를 반복하는 경우가 많으며, 이는 기계식 케이블 시스템의 마모를 가속화하는 요인으로 작용합니다. 그 결과, 교체 수요는 계속 견고하게 유지되고 있으며, 아시아태평양의 자동차 제어 케이블 생산 및 소비에서 중국이 가장 중요한 시장 중 하나로 자리 매김하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 케이블별, 2022년-2035년

제6장 시장 추산 및 예측 : 재료별, 2022년-2035년

제7장 시장 추산 및 예측 : 차량별, 2022년-2035년

제8장 시장 추산 및 예측 : 용도별, 2022년-2035년

제9장 시장 추산 및 예측 : 판매채널별, 2022년-2035년

제10장 시장 추산 및 예측 : 지역별, 2022년-2035년

제11장 기업 개요

LSH 26.04.23The Global Automotive Control Cables Market was valued at USD 5.1 billion in 2025 and is estimated to grow at a CAGR of 4.1% to reach USD 7.6 billion by 2035.

Despite the increasing shift toward vehicle electrification, the demand for automotive control cables remains stable because various mechanical systems still require cable-based mechanisms for operational functionality. Even in vehicles powered by electric drivetrains, several internal mechanical operations continue to rely on control cable systems to enable consistent movement and functionality. In addition to new vehicle production, the global aging vehicle fleet is playing a significant role in sustaining demand for replacement components. The average age of vehicles in circulation worldwide surpassed twelve years in 2023, which has contributed to higher wear rates for mechanical components such as control cables. As vehicles remain in service for longer periods, maintenance and replacement activities have become increasingly important across both developed and developing automotive markets. Consequently, replacement parts account for roughly forty percent of total automotive control cable sales in mature markets, reinforcing the importance of the aftermarket segment alongside original equipment manufacturing demand within the global automotive control cables market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.1 Billion |

| Forecast Value | $7.6 Billion |

| CAGR | 4.1% |

Although the automotive industry is gradually adopting advanced electronic transmission technologies and digital control systems, manual transmission vehicles continue to maintain a meaningful share of global vehicle production. In 2024, vehicles equipped with manual transmissions accounted for nearly thirty percent of total global production. This continued presence supports consistent demand for clutch and gear control cables across passenger vehicles and light-duty vehicle categories. While advancements in vehicle electronics and automated systems are influencing component design, these developments are not expected to significantly reduce the overall volume of control cables required within the automotive sector.

The brake cables segment held 23.3% share in 2025 and is expected to grow at a CAGR of 5% from 2026 to 2035. Brake cable systems remain a fundamental component in vehicle safety mechanisms, which supports their continued importance across passenger and commercial vehicle categories worldwide. Regulatory frameworks focused on vehicle safety standards contribute to consistent demand for reliable braking systems that require durable control cables. In addition to original equipment demand, brake cables experience frequent wear due to regular vehicle operation, which increases the need for replacement parts throughout the lifespan of vehicles. As a result, brake cable systems contribute significantly to the overall volume of control cables sold across both OEM and aftermarket segments within the automotive control cables market.

Based on material type, the steel segment held a 44.6% share in 2025 and is projected to grow at a CAGR of 3.7% between 2026 and 2035. Steel cables remain widely preferred for automotive applications that require strong tensile performance and high load-bearing capacity to maintain reliable mechanical operation. These characteristics are particularly important in vehicle systems where durability and consistent performance are required over extended operating cycles. Steel-based cables also demonstrate strong resistance to mechanical stress and environmental conditions, making them suitable for long-term use in various vehicle platforms. Due to their established reliability and performance characteristics, automotive manufacturers continue to rely on steel control cables for large-scale vehicle production across multiple automotive segments.

China Automotive Control Cables Market held 53% share, generating USD 1.4 billion in 2025. The country represents a critical hub for automotive manufacturing due to its extensive vehicle production capacity and large installed vehicle base. High production volumes across passenger vehicles, commercial vehicles, and two-wheeler segments contribute to sustained demand for original equipment control cable systems. The continuous expansion of the vehicle population also creates substantial demand for aftermarket replacement components. Vehicles operating in densely populated urban and semi-urban environments often experience frequent start-and-stop driving conditions, which can accelerate wear in mechanical cable systems. As a result, replacement demand remains strong, reinforcing China's position as one of the most significant markets for automotive control cable production and consumption within the Asia Pacific region.

Major companies operating in the Global Automotive Control Cables Market include Atsumitec, Chuo Spring, Dura Automotive Systems, Ficosa International, Grand Rapids Controls, Hi-Lex, Kuster, Minda, Suprajit Engineering, and TSC. Companies competing in the Automotive Control Cables Market are adopting a range of strategic initiatives to strengthen their competitive positions and expand global market presence. Manufacturers are focusing on product innovation by developing advanced cable systems that offer improved durability, flexibility, and performance across diverse vehicle applications. Many companies are also investing in expanding production facilities and strengthening supply chain capabilities to support growing demand from automotive manufacturers worldwide. Strategic collaborations with vehicle manufacturers are helping suppliers integrate control cable systems into next-generation vehicle platforms. In addition, companies are expanding their aftermarket distribution networks to capture the growing demand for replacement components as the global vehicle fleet ages.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Cable

- 2.2.3 Material

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle parc

- 3.2.1.2 Sustained demand for mechanical systems

- 3.2.1.3 Increasing average vehicle age

- 3.2.1.4 Growth in emerging automotive markets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Shift toward electronic actuation systems

- 3.2.2.2 Price sensitivity in aftermarket

- 3.2.3 Market opportunities

- 3.2.3.1 Rising electric vehicle production

- 3.2.3.2 Expansion of organized aftermarket

- 3.2.3.3 Localization of component manufacturing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States automotive safety and mechanical control component regulations

- 3.4.1.2 Federal motor vehicle safety standards related to braking and control systems

- 3.4.1.3 Vehicle durability and performance compliance requirements

- 3.4.1.4 Canada automotive component safety and quality regulations

- 3.4.2 Europe

- 3.4.2.1 European Union automotive safety and component compliance framework

- 3.4.2.2 ECE regulations for braking and mechanical control systems

- 3.4.2.3 Country level automotive component certification requirements

- 3.4.2.4 Environmental and material compliance rules for automotive cables

- 3.4.3 Asia Pacific

- 3.4.3.1 China automotive component standards and quality regulations

- 3.4.3.2 India automotive safety and component homologation standards

- 3.4.3.3 Japan vehicle safety and mechanical control system guidelines

- 3.4.3.4 South Korea automotive component quality and durability standards

- 3.4.3.5 ASEAN regional automotive component regulatory frameworks

- 3.4.4 Latin America

- 3.4.4.1 Brazil automotive safety and component compliance regulations

- 3.4.4.2 Argentina vehicle component quality requirements

- 3.4.4.3 Mexico automotive manufacturing and safety standards

- 3.4.4.4 Regional automotive component regulatory frameworks

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE automotive safety and vehicle component regulations

- 3.4.5.2 Saudi Arabia vehicle safety and mechanical system compliance

- 3.4.5.3 South Africa automotive component standards and road safety requirements

- 3.4.5.4 Regional automotive regulatory frameworks

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Drive by Wire Technology Substitution Threat

- 3.13.1 Electronic Throttle Control Penetration

- 3.13.2 Electronic Parking Brake Adoption Rates

- 3.13.3 Shift by Wire Transmission Systems

- 3.13.4 Cost Benefit Analysis Mechanical versus Electronic Systems

- 3.14 Geographic Manufacturing Cluster Analysis

- 3.14.1 Major Manufacturing Hubs by Region

- 3.14.2 Proximity to OEM Facility Requirements

- 3.14.3 Regional Production Capacity Distribution

- 3.14.4 Manufacturing Consolidation versus Distributed Models

- 3.15 Patent Monetization and IP Value Creation

- 3.15.1 Licensing Revenue Opportunities

- 3.15.2 Patent Portfolio Valuation

- 3.15.3 Cross Licensing Agreements

- 3.15.4 Defensive Patent Strategies

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Cable, 2022 - 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Clutch cables

- 5.3 Accelerator cables

- 5.4 Brake cables

- 5.5 Gear shift cables

- 5.6 Handbrake cables

- 5.7 Throttle cables

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Steel

- 6.3 PVC (Polyvinyl Chloride)

- 6.4 Nylon

- 6.5 Rubber coated

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Medium Commercial Vehicles (MCV)

- 7.3.3 Heavy Commercial Vehicles (HCV)

- 7.4 Two-wheelers

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Engine control

- 8.3 Transmission control

- 8.4 Braking system

- 8.5 HVAC system

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Norway

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Atsumitec

- 11.1.2 Cofle

- 11.1.3 Dura Automotive Systems

- 11.1.4 Ficosa International

- 11.1.5 Hi-Lex

- 11.1.6 Kuster

- 11.1.7 Kyung Chang Industrial

- 11.1.8 Nippon Cable System

- 11.1.9 Sila

- 11.1.10 Suprajit Engineering

- 11.2 Regional Players

- 11.2.1 Cable Manufacturing & Assembly

- 11.2.2 Cablecraft Motion Controls

- 11.2.3 Chuo Spring

- 11.2.4 GEMO

- 11.2.5 Grand Rapids Controls

- 11.2.6 Minda

- 11.2.7 Tata AutoComp Systems

- 11.2.8 Thai Steel Cable

- 11.2.9 WR Controls

- 11.3 Emerging Players / Disruptors

- 11.3.1 Acey Engineering

- 11.3.2 Kalpa Industries

- 11.3.3 KALTROL

- 11.3.4 Premier Auto Cables

- 11.3.5 Remsons Industries

- 11.3.6 Silco Automotive Solutions