|

시장보고서

상품코드

1998709

담금질 유체 및 염류 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Quenching Fluids and Salts Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

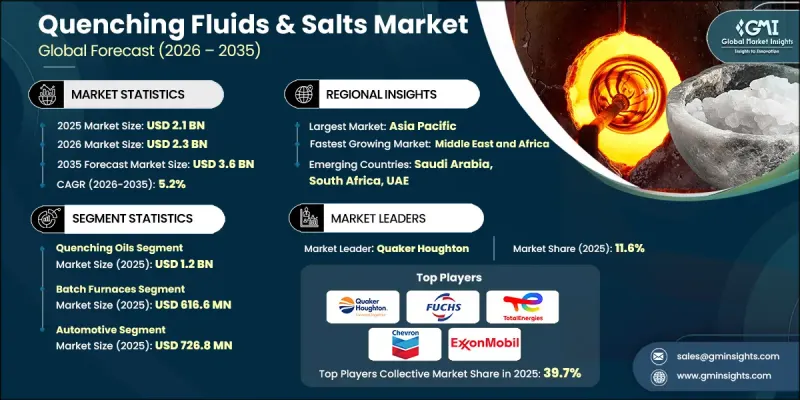

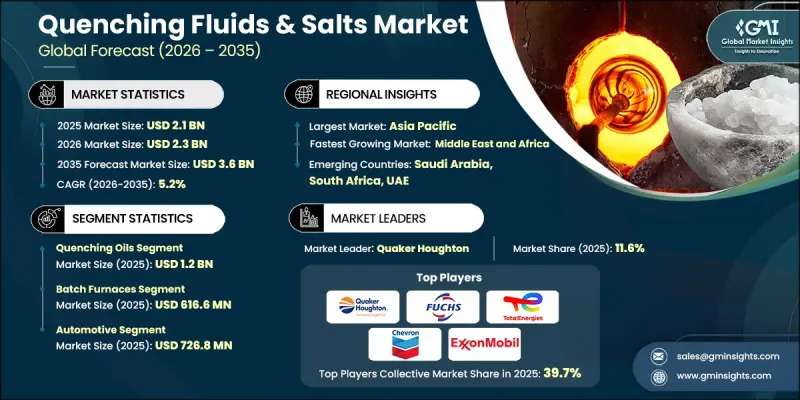

세계의 담금질 유체 및 염류 시장은 2025년에 21억 달러로 평가되었고, CAGR5.2%로 성장하여 2035년까지 36억 달러에 달할 것으로 예측됩니다.

담금질 유체 및 염류는 가열된 금속을 빠르게 냉각시키고 경도와 구조적 강도 향상과 같은 바람직한 기계적 특성을 부여함으로써 열처리 공정에서 핵심적인 역할을 합니다. 이러한 재료는 가공된 금속의 미세조직, 내구성 및 치수 안정성에 직접적인 영향을 미치는 제어된 냉각을 가능하게 합니다. 수년에 걸쳐 열처리 작업은 산업 생산의 효율성과 일관성을 향상시키기 위해 설계된 기술적으로 진보된 담금질 시스템으로 전환되고 있습니다. 최신 담금질 기술에서는 냉각 제어의 향상, 작업의 안전성 및 공정의 신뢰성 향상에 중점을 두고 있습니다. 제조업체들은 보다 정밀한 열 관리를 가능하게 하고, 급속 냉각 공정에 따른 운영상의 문제를 최소화하는 혁신적인 배합을 도입하고 있습니다. 또한, 시장에서는 진화하는 지속가능성 기준을 충족하도록 설계된 환경 친화적인 담금질 솔루션이 개발되고 있습니다. 또한, 열처리 시스템에 자동화 및 디지털 프로세스 모니터링의 통합이 진행됨에 따라 시설은 온도 제어, 반복성 및 생산성 향상을 실현하고 있습니다. 이러한 발전은 종합적으로 다양한 제조 환경에서 사용되는 열처리 부품의 성능과 신뢰성을 뒷받침하는 데 있어 담금질유 및 염의 역할을 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 금액 | 21억 달러 |

| 예측 금액 | 36억 달러 |

| CAGR | 5.2% |

담금질 유체 부문은 2025년 12억 달러 시장 규모를 기록했습니다. 담금질 유체는 신뢰할 수 있는 냉각 특성과 일관된 금속학적 성능을 제공하기 때문에 열처리 공정에서 널리 사용되고 있습니다. 제어된 냉각을 실현할 수 있는 능력으로 광범위한 열처리 시스템 및 금속학적 요구 사항에 적합합니다. 업계 동향을 살펴보면, 대규모 제조 환경에서 더 빠르고 균형 잡힌 냉각 거동을 제공하도록 설계된 최적화된 오일 배합에 대한 관심이 증가하고 있습니다. 제조업체들은 열 안정성 향상, 증발량 감소, 가동 중 배출량 감소를 위한 첨단 배합에 점점 더 많은 노력을 기울이고 있습니다. 이러한 개발은 보다 안전한 산업 환경을 지원하는 동시에 유체의 수명을 연장하고 공정의 일관성을 유지합니다.

2025년 기준, 배치로 부문 시장 규모는 6억 1,660만 달러에 달했습니다. 이러한 용광로 시스템은 운영상의 유연성과 다양한 부품 크기 및 생산량을 처리할 수 있는 능력으로 인해 열처리 시설에서 널리 사용되고 있습니다. 제조업체들은 담금질 공정을 정밀하게 제어하면서 효율적인 열처리를 수행하기 위해 이러한 시스템에 의존하고 있습니다. 산업 분야에서 생산 효율성 향상, 에너지 사용 최적화, 다양한 담금질 매체와의 호환성이 우선순위가 되면서 장비 부문도 진화하고 있습니다. 용광로 설계의 기술적 진보로 열 분포의 균일성 향상, 자동화 기능 강화 및 공정 신뢰성 향상이 가능해졌습니다. 장비 공급업체 역시 생산 워크플로우의 효율성과 일관된 처리 결과를 지원하는 솔루션에 초점을 맞추었습니다. 산업시설이 열처리 인프라를 현대화함에 따라, 운영 유연성과 안정적인 담금질 성능을 제공하는 용광로 기술에 대한 수요는 계속 견고할 것으로 예측됩니다.

미국의 담금질 유체 및 염류 시장은 2025년 4억 5,960만 달러에 달했습니다. 이 나라 시장 성장은 까다로운 성능 요건을 요구하는 용도를 위한 고품질 열처리 부품이 필요한 제조 생태계가 잘 구축되어 있기 때문에 가능했습니다. 이 지역의 산업 부문은 제품의 신뢰성과 내구성을 향상시키기 위해 첨단 소재 가공 기술에 지속적으로 투자하고 있습니다. 한편, 캐나다에서는 광범위한 산업 현대화 이니셔티브의 일환으로 최신 담금질 기술이 꾸준히 도입되고 있습니다. 이 지역의 제조업체들은 금속 가공 공정의 생산 효율성 향상과 품질 관리 강화에 중점을 두고 있습니다. 디지털 제조 방식과 자동화된 열처리 시스템의 도입으로 기업들은 담금질 공정을 최적화하고, 운영상의 실수를 줄이며, 생산 비용을 보다 효과적으로 관리할 수 있게 되었습니다. 이러한 요인들이 복합적으로 작용하여 북미 전역의 담금질 유체 및 염류 시장의 지속적인 성장에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별, 2022년-2035년

제6장 시장 추산 및 예측 : 노/설비 유형별, 2022년-2035년

제7장 시장 추산 및 예측 : 최종사용자 산업별, 2022년-2035년

제8장 시장 추산 및 예측 : 지역별, 2022년-2035년

제9장 기업 개요

LSH 26.04.23The Global Quenching Fluids & Salts Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 3.6 billion by 2035.

Quenching fluids and salts play a central role in heat treatment processes by rapidly cooling heated metals so that they achieve desired mechanical characteristics such as improved hardness and structural strength. These materials enable controlled cooling that directly influences the microstructure, durability, and dimensional stability of treated metals. Over time, heat treatment operations have increasingly transitioned toward technologically advanced quenching systems designed to improve efficiency and consistency in industrial production. Modern quenching technologies emphasize improved cooling control, operational safety, and enhanced process reliability. Manufacturers are introducing innovative formulations that support more precise thermal management and minimize operational challenges associated with rapid cooling processes. The market is also witnessing the development of environmentally considerate quenching solutions designed to meet evolving sustainability standards. In addition, growing integration of automation and digital process monitoring within heat treatment systems is helping facilities achieve better temperature regulation, repeatability, and productivity. These developments collectively strengthen the role of quenching fluids and salts in supporting the performance and reliability of heat-treated components used across multiple manufacturing environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 5.2% |

The quenching oils segment generated USD 1.2 billion in 2025. Quenching oils remain widely used in heat treatment operations because they provide reliable cooling characteristics and consistent metallurgical performance. Their ability to deliver controlled cooling makes them suitable for a wide range of heat treatment systems and metallurgical requirements. Industry trends indicate rising interest in optimized oil formulations designed to provide faster or more balanced cooling behavior for large-scale manufacturing environments. Manufacturers are increasingly focusing on advanced formulations that offer improved thermal stability, reduced evaporation, and lower emissions during operation. These developments are supporting safer industrial environments while also extending fluid life and maintaining process consistency.

The batch furnaces segment accounted for USD 616.6 million in 2025. These furnace systems are widely utilized in heat treatment facilities due to their operational flexibility and ability to process varied component sizes and production volumes. Manufacturers rely on these systems for efficient thermal processing while maintaining precise control over quenching operations. The equipment segment is evolving as industries prioritize improved production efficiency, optimized energy utilization, and compatibility with multiple quenching media. Technological advancements in furnace design are enabling better thermal uniformity, improved automation capabilities, and enhanced process reliability. Equipment suppliers are also focusing on solutions that support streamlined production workflows and consistent processing outcomes. As industrial facilities continue to modernize their heat treatment infrastructure, furnace technologies that deliver operational flexibility and stable quenching performance are expected to maintain strong demand.

United States Quenching Fluids & Salts Market reached USD 459.6 million in 2025. Market growth in the country is supported by the presence of a well-established manufacturing ecosystem that requires high-quality heat-treated components for demanding performance applications. Industrial sectors across the region continue to invest in advanced materials processing technologies to improve product reliability and durability. Meanwhile, Canada is steadily adopting modern quenching technologies as part of broader industrial modernization initiatives. Manufacturers across the region are emphasizing improved production efficiency and enhanced quality control in metal processing operations. Increasing adoption of digital manufacturing practices and automated heat treatment systems is helping companies optimize quenching processes, reduce operational errors, and control production costs more effectively. These factors collectively contribute to the continued expansion of the quenching fluids & salts market across North America.

Major companies operating in the Global Quenching Fluids & Salts Market include BP Castrol, Croda International Plc, CONDAT, Idemitsu Kosan Co., Ltd., Exxon Mobil Corporation, Petrofer Chemie, Chemtool Incorporated, FUCHS Petrolub SE, Quaker Houghton, TotalEnergies SE, Chevron Corporation, Hubbard-Hall, Park Thermal International, Metal Heat Treatment Solutions, and Savannah River Nuclear Solutions. Companies in the quenching fluids & salts market are focusing on multiple strategic initiatives to strengthen their competitive position and expand their global presence. Product innovation remains a key priority, with manufacturers investing in research and development to create advanced quenching solutions that deliver improved thermal performance, longer service life, and enhanced environmental compatibility. Strategic collaborations with equipment manufacturers and heat treatment service providers are also helping companies integrate their fluids into advanced thermal processing systems. In addition, firms are expanding production capabilities and distribution networks to serve growing industrial demand across emerging manufacturing regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Furnace/Equipment Type

- 2.2.3 End User Industry

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth of automotive and manufacturing industries

- 3.2.1.2 Rising demand for high-performance materials

- 3.2.1.3 Technological advancements in heat treatment processes

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental and regulatory challenges

- 3.2.2.2 Risk of metallurgical defects

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of polymer-based quenchants

- 3.2.3.2 Rising demand from infrastructure and energy projects

- 3.2.3.3 Demand for customized and application-specific solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Quenching oils

- 5.2.1 Fast/accelerated quenching oils

- 5.2.2 Medium-speed quenching oils

- 5.2.3 Slow-speed quenching oils

- 5.2.4 Marquench/martempering

- 5.2.5 Vacuum quenching oils

- 5.2.6 Synthetic quenching oils

- 5.2.7 Others

- 5.3 Quenching salts

- 5.3.1 Nitrate-based salts

- 5.3.2 Nitrite-based salts

- 5.3.3 Chloride-based salts

- 5.3.4 Cyanide-based salts

- 5.3.5 Fluoride-based salts

- 5.3.6 Others

- 5.4 Polymer quenchants

- 5.4.1 PAG-based (polyalkylene glycol)

- 5.4.2 PVP-based (polyvinylpyrrolidone)

- 5.4.3 Others

Chapter 6 Market Estimates and Forecast, By Furnace/Equipment Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Batch furnaces

- 6.3 Continuous furnaces

- 6.4 Vacuum furnaces

- 6.5 Induction heating systems

- 6.6 Salt bath furnaces

- 6.7 Sealed quench furnaces

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By End User Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Aerospace and defense

- 7.4 Construction equipment and heavy machinery

- 7.5 Tool and die manufacturing

- 7.6 Bearing manufacturing

- 7.7 Energy and power generation

- 7.8 Medical devices

- 7.9 Oil and gas

- 7.10 Rail and transportation

- 7.11 Mining

- 7.12 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BP Castrol

- 9.2 Chemtool Incorporated

- 9.3 Chevron Corporation

- 9.4 CONDAT

- 9.5 Croda International Plc

- 9.6 Exxon Mobil Corporation

- 9.7 FUCHS Petrolub SE

- 9.8 Hubbard-Hall

- 9.9 Idemitsu Kosan Co., Ltd.

- 9.10 Metal Heat Treatment Solutions

- 9.11 Park Thermal International

- 9.12 Petrofer Chemie

- 9.13 Quaker Houghton

- 9.14 Savannah River Nuclear Solutions

- 9.15 TotalEnergies SE