|

시장보고서

상품코드

1998721

자율주행차 개발 플랫폼 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Autonomous Vehicle Development Platform Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

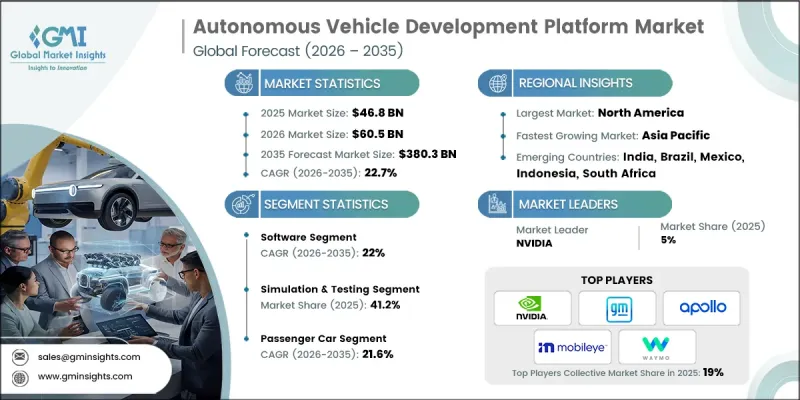

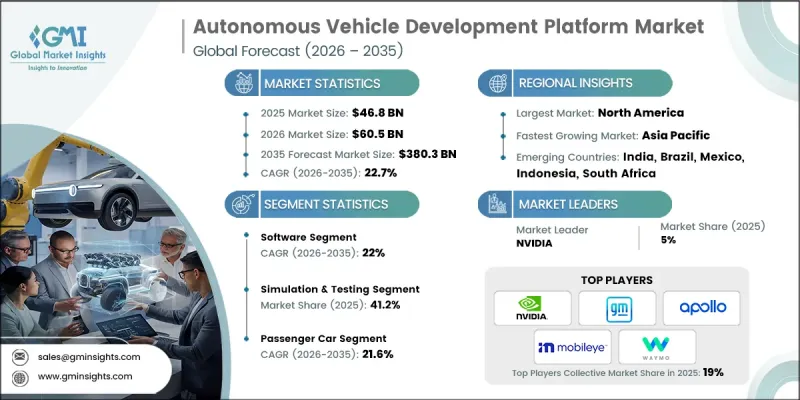

세계의 자율주행차 개발 플랫폼 시장은 2025년에 468억 달러로 평가되며, 2035년까지 CAGR 22.7%로 성장하며, 3,803억 달러에 달할 것으로 추정되고 있습니다.

시장 확대는 머신러닝과 인공지능의 발전에 의해 주도되고 있습니다. 이는 자율주행차의 인지, 의사결정, 경로 계획 기능을 강화하여 복잡한 환경에서의 내비게이션이 가능하도록 합니다. OEM 차량에 첨단운전자보조시스템(ADAS)와 단계적인 자율주행 기능의 통합이 진행되면서 종합적인 개발, 테스트, 검증 플랫폼에 대한 수요가 증가하고 있습니다. 주요 자동차 제조업체와 기술 기업은 혁신을 가속화하고 플랫폼의 기능을 강화하기 위해 많은 투자를 하고 있으며, 이를 통해 상용화를 앞당기는 데 박차를 가하고 있습니다. 클라우드 기반 시뮬레이션 환경은 실차를 이용한 테스트에 비해 대규모 테스트 수행, 분산된 팀 간의 협업 워크플로우, 비용 절감 등의 이점이 있으며, 주목받고 있습니다. AI를 활용한 시뮬레이션은 엣지 케이스의 시나리오 모델링을 더욱 정교하게 만들어 알고리즘의 정확도를 높이는 동시에 비용이 많이 드는 현장 테스트를 최소화할 수 있습니다. 이 시장은 지속적인 소프트웨어 혁신, 확장 가능한 클라우드 플랫폼, AI 기반자율주행 기능에 대한 전략적 투자로 특징지어집니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 468억 달러 |

| 예측액 | 3,803억 달러 |

| CAGR | 22.7% |

소프트웨어 분야는 2025년 72%의 점유율을 차지하며, 2035년까지 연평균 복합 성장률(CAGR) 22%를 나타낼 것으로 예측됩니다. 자율주행차 개발용 소프트웨어에는 센서 시뮬레이션, 인지 모델링, 매핑, 위치 추정, 의사결정 프레임워크 등이 포함되어 다양한 주행 조건에서 가상 검증이 가능합니다. 이 플랫폼은 데이터 수집, 주석, 머신러닝 모델 훈련 및 테스트를 지원하여 물체 감지, 경로 계획, 차량 제어 시스템 개선에 기여합니다.

승용차 부문은 2025년 62%의 점유율을 차지하며, 2026-2035년 연평균 복합 성장률(CAGR) 21.6%를 나타낼 것으로 예측됩니다. 승용차에는 레벨 2+ 및 조건부 레벨 3의 자율주행 기능이 빠르게 도입되고 있으며, 개발 플랫폼에 대한 수요를 주도하고 있습니다. OEM은 시뮬레이션, 센서 융합 소프트웨어 및 AI 기반 검증 툴을 통해 기능 배포를 가속화하고, 규제를 준수하고, 안전 테스트를 통과하고, OTA(Over-the-Air) 업데이트를 통해 커넥티드카 시스템을 통합하기 위해 시뮬레이션, 센서 융합 소프트웨어 및 AI 기반 검증 툴에 의존하고 있습니다. 이 플랫폼은 대규모 데이터 훈련과 디지털 트윈 테스트를 통해 AI 개인화, 예측적 의사결정 및 고급 인지 시스템을 통해 도시 주행 성능을 향상시키는 데 중점을 두고 있습니다.

2025년 미국의 자율주행차 개발 플랫폼 시장은 131억 달러 규모에 달했습니다. AI, 클라우드, 시뮬레이션에 대한 전문 지식이 집중되어 있으며, 자율주행차 플랫폼 개발에서 세계 선두를 달리고 있습니다. 대학, 연구기관, OEM 간의 협력을 통해 머신러닝, 인식, 의사결정의 프레임워크가 강화되고 있습니다. 벤처캐피털의 투자가 스타트업과 플랫폼 기술 혁신을 지원하며 미국의 리더십을 더욱 공고히 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 컴포넌트별, 2022-2035

제6장 시장 추산·예측 : 기능별, 2022-2035

제7장 시장 추산·예측 : 최종 용도별, 2022-2035

제8장 시장 추산·예측 : 차량별, 2022-2035

제9장 시장 추산·예측 : 도입 형태별, 2022-2035

제10장 시장 추산·예측 : 지역별, 2022-2035

제11장 기업 개요

KSA 26.04.20The Global Autonomous Vehicle Development Platform Market was valued at USD 46.8 billion in 2025 and is estimated to grow at a CAGR of 22.7% to reach USD 380.3 billion by 2035.

Market expansion is fueled by advances in machine learning and artificial intelligence, which enhance autonomous vehicle perception, decision-making, and route planning, enabling navigation in complex environments. Increasing integration of advanced driver assistance systems (ADAS) and incremental autonomous features in OEM vehicles is driving demand for comprehensive development, testing, and validation platforms. Major automakers and technology firms are investing heavily to accelerate innovation and enhance platform capabilities, facilitating faster commercial deployment. Cloud-based simulation environments are gaining traction as they enable large-scale testing, collaborative workflows across distributed teams, and cost reductions compared with physical test vehicles. AI-powered simulation further refines edge-case scenario modeling, improving algorithm accuracy while minimizing expensive real-world trials. The market is defined by continual software innovation, scalable cloud platforms, and strategic investments in AI-driven autonomous functionality.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $46.8 Billion |

| Forecast Value | $380.3 Billion |

| CAGR | 22.7% |

The software segment accounted for 72% share in 2025 and is expected to grow at a CAGR of 22% through 2035. Autonomous vehicle development software includes sensor simulation, perception modeling, mapping, localization, and decision-making frameworks, allowing virtual validation under diverse driving conditions. These platforms support data collection, annotation, and the training and testing of machine learning models, improving object detection, path planning, and vehicle control systems.

The passenger car segment held 62% share in 2025 and is expected to grow at a CAGR of 21.6% from 2026 to 2035. Passenger vehicles are rapidly incorporating Level 2+ and Conditional Level 3 autonomy, driving demand for development platforms. OEMs rely on simulation, sensor fusion software, and AI-based validation tools to accelerate feature deployment, comply with regulations, pass safety tests, and integrate connected vehicle systems with over-the-air updates. Platforms emphasize AI personalization, predictive decision-making, and advanced perception systems through large-scale data training and digital twin testing, improving urban driving performance.

U.S. Autonomous Vehicle Development Platform Market generated USD 13.1 billion in 2025. The country leads globally in AV platform development due to its concentration of AI, cloud, and simulation expertise. Collaboration between universities, research institutions, and OEMs strengthens machine learning, perception, and decision-making frameworks. Venture capital investment supports innovation in start-ups and platform technologies, further reinforcing U.S. leadership.

Key players in the Global Autonomous Vehicle Development Platform Market include NVIDIA, Waymo (Alphabet), Tesla, GM / Cruise, Mobileye (Intel), Mercedes-Benz, Toyota, Baidu (Apollo), Microsoft, and Qualcomm. Companies in the Autonomous Vehicle Development Platform Market are focusing on several strategies to strengthen their market position. Key approaches include heavy investment in AI and machine learning to enhance perception and decision-making capabilities. Firms are developing scalable cloud-based simulation environments for faster and cost-effective validation of autonomous systems. Strategic partnerships with OEMs, technology providers, and research institutions enable collaboration on advanced sensor fusion, mapping, and digital twin technologies. Companies are also expanding globally to tap into emerging markets and adopting modular, adaptable platforms to meet varying vehicle types and autonomy levels.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Functionality

- 2.2.4 End use

- 2.2.5 Vehicle

- 2.2.6 Deployment mode

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Advanced AI and machine learning integration

- 3.2.1.2 Increasing adoption of ADAS and autonomous technologies

- 3.2.1.3 Growing investment from OEMs and tech companies

- 3.2.1.4 Expansion of cloud computing and simulation infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and R&D costs

- 3.2.2.2 Regulatory uncertainty and compliance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for Level 4-5 autonomous vehicles

- 3.2.3.2 Integration of digital twin and simulation technologies

- 3.2.3.3 Partnerships between tech companies and automakers

- 3.2.3.4 Emerging markets adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Transport Canada Motor Vehicle Safety Standards (CMVSS)

- 3.4.2 Europe

- 3.4.2.1 European Whole Vehicle Type Approval (WVTA)

- 3.4.2.2 ECE Regulation 124 (R124)

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan Automotive Standards Organization (JASO)

- 3.4.3.2 AIS (Automotive Industry Standards) - India

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Traffic Council (CONTRAN) - Resolution 242

- 3.4.4.2 Mexican NOM Standards (Normas Oficiales Mexicanas)

- 3.4.5 Middle East & Africa

- 3.4.5.1 Emirates Authority for Standardization and Metrology (ESMA)

- 3.4.5.2 South African Bureau of Standards (SABS)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis (Driven by Primary Research)

- 3.8.1 Historical price trend analysis

- 3.8.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 Gen AI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Infrastructure & deployment landscape (Driven by primary research)

- 3.13.1 Deployment penetration by region & buyer segment

- 3.13.2 Scalability constraints & infrastructure investment trends

- 3.14 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Simulation & testing software

- 5.2.2 Sensor fusion & perception software

- 5.2.3 Machine learning & AI frameworks

- 5.2.4 Data management & annotation software

- 5.2.5 Mapping & localization software

- 5.2.6 Control & decision-making software

- 5.3 Services

- 5.3.1 Professional services

- 5.3.2 Managed services

Chapter 6 Market Estimates & Forecast, By Functionality, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Sensor simulation

- 6.3 Data collection & analysis

- 6.4 Simulation & testing

Chapter 7 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Automotive manufacturers

- 7.3 Technology companies

- 7.4 Research institutions & universities

- 7.5 Government & defense

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Hatchback

- 8.2.2 SUV

- 8.2.3 Sedan

- 8.3 Commercial vehicle

- 8.3.1 LCV

- 8.3.2 MCV

- 8.3.3 HCV

Chapter 9 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 On-premises platforms

- 9.3 Cloud-based platforms

- 9.4 Hybrid deployment

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.4.8 Philippines

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 Baidu (Apollo)

- 11.1.2 GM

- 11.1.3 Mercedes-Benz

- 11.1.4 Microsoft

- 11.1.5 Mobileye (Intel)

- 11.1.6 NVIDIA

- 11.1.7 Qualcomm

- 11.1.8 Tesla

- 11.1.9 Toyota

- 11.1.10 Waymo (Alphabet)

- 11.2 Regional players

- 11.2.1 Ansys

- 11.2.2 Aurora Innovation

- 11.2.3 dSPACE

- 11.2.4 Momenta

- 11.2.5 Pony.ai

- 11.3 Emerging players

- 11.3.1 Applied Intuition

- 11.3.2 CARLA Simulator (Open-Source Community)

- 11.3.3 Cognata

- 11.3.4 Foretellix

- 11.3.5 Parallel Domain

- 11.3.6 Scale AI