|

시장보고서

상품코드

1998740

피혁용 염료 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Leather Dyes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

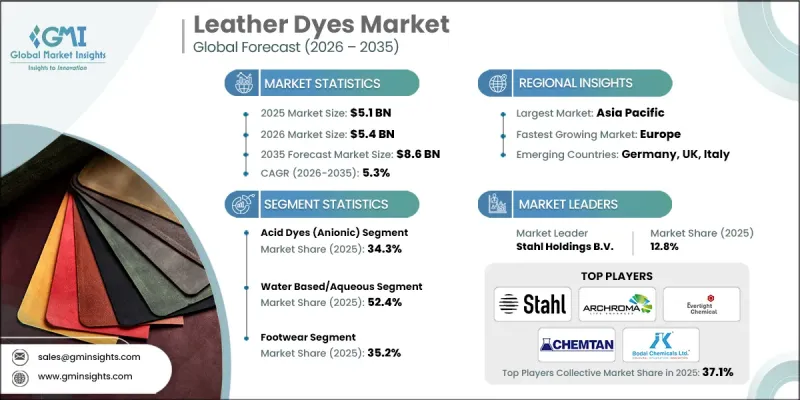

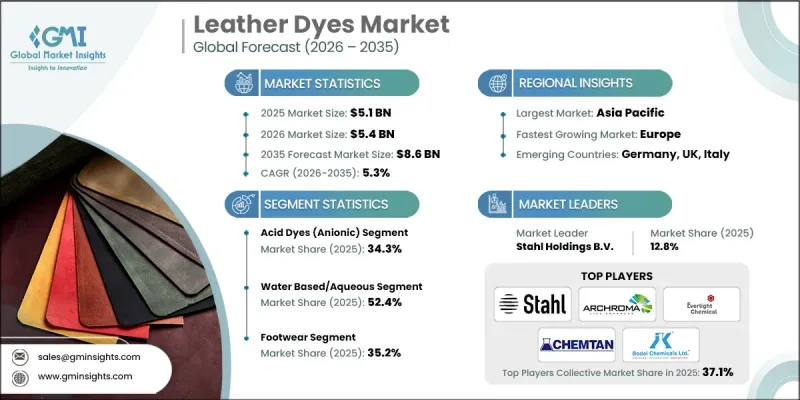

세계의 피혁용 염료 시장은 2025년에 51억 달러로 평가되며, CAGR 5.3%로 성장하며, 2035년까지 86억 달러에 달할 것으로 추정되고 있습니다.

여러 최종 사용 분야에서 고급 가죽 제품에 대한 수요가 지속적으로 증가함에 따라 이 산업은 점점 더 많은 추진력을 얻고 있습니다. 가죽용 염료는 가죽 제품의 미적 매력, 질감 및 장기적인 성능을 향상시키는 데 중요한 역할을 합니다. 제조업체들은 일관된 발색, 향상된 마감 품질, 강화된 내구성을 달성하기 위해 첨단 염료 배합에 의존하고 있습니다. 고품질 가죽 소재에 대한 선호도가 높아짐에 따라 색상의 선명도와 제품의 장기적인 신뢰성을 보장하는 혁신적인 염색 기술에 대한 수요가 증가하고 있습니다. 또한 소비자들이 점점 더 친환경적인 가공 방법을 선호함에 따라 지속가능성도 시장 역학을 형성하고 있습니다. 이러한 변화는 진화하는 환경 기준에 부합하는 수성 및 저독성 염료 솔루션의 채택을 촉진하고 있습니다. 화학물질 사용 및 배출에 대한 규제 압력도 제조업체들이 더 깨끗한 생산 기술에 투자하도록 더욱 촉구하고 있습니다. 염료 화학의 지속적인 발전과 우수한 품질 및 지속가능한 성과에 대한 기대치가 높아지면서 세계 가죽 염료 시장의 장기적인 성장 전망은 더욱 견고해지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 51억 달러 |

| 예측액 | 86억 달러 |

| CAGR | 5.3% |

수성 및 수용성 염료 부문은 2025년에 52.4%의 점유율을 차지하며, 2026-2035년 연평균 5.5%의 성장률을 보일 것으로 예측됩니다. 이 제제들은 환경 부하가 적고 엄격한 VOC 배출 기준을 준수하므로 강력한 지지를 받고 있습니다. 일부 선진국의 규제 감독 강화로 인해 지속가능한 염색 대안으로의 전환이 가속화되고 있습니다. 액체 염료는 효율적인 처리, 균일한 침투, 자동 제조 시스템과의 호환성으로 인해 계속해서 시장을 독점하고 있습니다. 적용의 용이성과 신뢰할 수 있는 성능으로 인해 대규모 생산자들에게 선호되는 선택이 되고 있습니다.

2025년 기준 신발 부문은 35.2%의 점유율을 차지하고 있으며, 2035년까지 연평균 복합 성장률(CAGR) 5.5%를 나타낼 것으로 예측됩니다. 개인화되고 패션성이 높은 가죽 제품에 대한 소비자의 관심이 높아지면서 이 부문의 성장세를 지원하고 있습니다. 제조업체들은 지속가능성 기준을 충족시키면서 색상의 일관성과 내구성을 향상시키기 위해 첨단 염색 기술을 점점 더 많이 활용하고 있습니다. 친환경 소재에 대한 수요가 증가함에 따라 생태계를 고려하지 않고도 성능 기준을 유지하는 혁신적인 염색 솔루션의 개발이 촉진되고 있습니다.

북미 가죽 염료 시장은 2025년 17.9%의 점유율을 차지했습니다. 자동차, 가구, 신발 제조 분야의 견고한 수요가 이 지역 시장 확대를 지원하고 있습니다. 화학물질의 사용과 배출을 규제하는 엄격한 환경 규제로 인해 생산자들은 환경 부하가 적은 염색 기술을 채택하도록 장려하고 있습니다. 고급 가죽 제품에 대한 소비자의 선호도가 높아지면서 우수한 색상 유지력과 장기적인 내구성을 제공하는 고성능 염료에 대한 수요가 더욱 증가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 유형별, 2022-2035

제6장 시장 추산·예측 : 제제별, 2022-2035

제7장 시장 추산·예측 : 용도별, 2022-2035

제8장 시장 추산·예측 : 지역별, 2022-2035

제9장 기업 개요

KSA 26.04.20The Global Leather Dyes Market was valued at USD 5.1 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 8.6 billion by 2035.

The industry is gaining momentum as demand for premium leather goods continues to increase across multiple end-use sectors. Leather dyes play a critical role in enhancing the aesthetic appeal, texture, and long-term performance of leather products. Manufacturers rely on advanced dye formulations to deliver consistent coloration, improved finish quality, and enhanced durability. Growing preference for high-grade leather materials is accelerating the need for innovative dyeing technologies that ensure lasting vibrancy and product reliability. Sustainability is also shaping market dynamics, as consumers increasingly favor environmentally responsible processing methods. This shift is encouraging the adoption of water-based and low-toxicity dye solutions that align with evolving environmental standards. Regulatory pressure regarding chemical usage and emissions is further influencing manufacturers to invest in cleaner production techniques. Continuous advancements in dye chemistry, combined with rising expectations for superior quality and sustainable outcomes, are reinforcing long-term growth prospects across the global leather dyes market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.1 Billion |

| Forecast Value | $8.6 Billion |

| CAGR | 5.3% |

The water-based and aqueous dyes segment accounted for 52.4% share in 2025 and is forecast to grow at a CAGR of 5.5% between 2026 and 2035. These formulations are gaining strong traction due to their lower environmental impact and compliance with strict VOC emission standards. Heightened regulatory oversight in several developed regions is accelerating the transition toward sustainable dyeing alternatives. Liquid dye formats continue to dominate the market, as they allow for efficient processing, uniform penetration, and compatibility with automated manufacturing systems. Their ease of application and reliable performance make them a preferred choice among large-scale producers.

The footwear segment held 35.2% share in 2025 and is anticipated to grow at a CAGR of 5.5% through 2035. Rising consumer interest in personalized and fashion-forward leather products is supporting segment expansion. Manufacturers are increasingly utilizing advanced dye technologies to achieve enhanced color consistency and durability while meeting sustainability benchmarks. The push for environmentally responsible materials is driving the development of innovative dye solutions that maintain performance standards without compromising ecological considerations.

North America Leather Dyes Market held a 17.9% share in 2025. Strong demand across automotive, furniture, and footwear manufacturing supports regional market expansion. Strict environmental regulations governing chemical usage and emissions are encouraging producers to adopt low-impact dyeing technologies. Growing consumer preference for premium leather goods is further stimulating demand for high-performance dyes that deliver superior color retention and long-term resilience.

Key companies operating in the Global Leather Dyes Market include Alliance Organics LLP, Stahl Holdings B.V., Archroma Management GmbH, American Enterprises Pvt Ltd, Atul Limited, Bodal Chemicals Ltd., Burboya, Chemtan Company Inc., Colourtex Industries, Ebro Chemicals, Everlight Chemical, Kiri Industries Ltd., Kolorjet Chemicals Pvt Ltd, and Krishna Industries. Companies in the Global Leather Dyes Market are strengthening their foothold through product innovation, sustainability initiatives, and strategic partnerships. Leading manufacturers are investing heavily in research and development to introduce advanced water-based and low-emission dye formulations that comply with evolving environmental regulations. Capacity expansions and modernization of production facilities are helping firms improve efficiency and meet rising global demand. Strategic collaborations with raw material suppliers and end-use manufacturers are enhancing supply chain stability and market reach. Many players are also focusing on geographic expansion to tap into emerging markets with growing leather consumption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Formulation

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Acid dyes (anionic)

- 5.3 Metal-complex dyes

- 5.4 Direct dyes

- 5.5 Pre-metalized dyes

- 5.6 Basic dyes (cationic)

- 5.7 Reactive dyes

- 5.8 Mordant dyes

- 5.9 Others (sulfur, etc.)

Chapter 6 Market Estimates and Forecast, By Formulation, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Water-based/aqueous

- 6.3 Liquid form

- 6.4 Powder/dust form

- 6.5 Solvent-based

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Footwear

- 7.3 Automotive

- 7.4 Furniture upholstery

- 7.5 Garments & apparel

- 7.6 Bags & luggage

- 7.7 Industrial leather

- 7.8 Gloves & accessories

- 7.9 Equestrian products

- 7.10 Others (book binding, etc.)

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Alliance Organics LLP

- 9.2 American Enterprises Pvt Ltd

- 9.3 Archroma Management GmbH

- 9.4 Atul Limited

- 9.5 Bodal Chemicals Ltd.

- 9.6 Burboya

- 9.7 Chemtan Company Inc.

- 9.8 Colourtex Industries

- 9.9 Ebro Chemicals

- 9.10 Everlight Chemical

- 9.11 Kiri Industries Ltd.

- 9.12 Kolorjet Chemicals Pvt Ltd

- 9.13 Krishna Industries

- 9.14 Stahl Holdings B.V.