|

시장보고서

상품코드

1998744

바이오디젤 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Biodiesel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

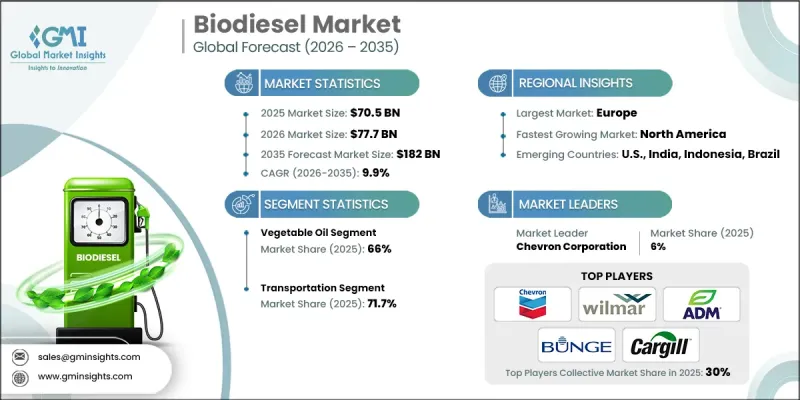

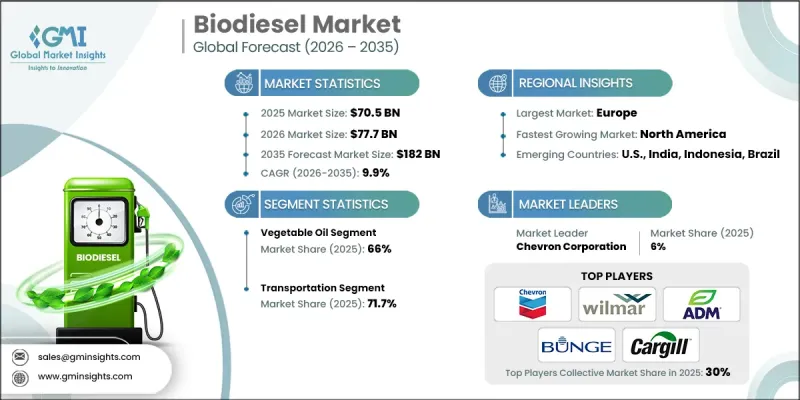

세계의 바이오디젤 시장은 2025년에 705억 달러로 평가되며, CAGR 9.9%로 성장하며, 2035년까지 1,820억 달러에 달할 것으로 추정되고 있습니다.

바이오디젤 시장의 확대는 각국의 운송 부문을 대상으로 한 연료 혼합 의무 강화와 더불어 청정 대체 연료 사용을 장려하는 규제 프레임워크에 의해 지원되고 있습니다. 디젤 의존도가 높은 경제권의 각국 정부는 대형 운송 사업에서 광범위한 탈탄소화 전략의 일환으로 바이오디젤 혼합 비율 요건을 꾸준히 높이고 있습니다. 또한 장비 제조업체들이 고농도 바이오디젤 혼합 연료를 사용하는 엔진에 대한 보증 범위를 확대함에 따라 도입에 대한 재정적 및 운영상의 장벽은 계속 낮아지고 있습니다. 이러한 추세에 따라 차량 보유 사업자는 신규 차량에 대한 대규모 설비 투자 없이도 기존 시스템에 바이오디젤을 도입할 수 있게 되었습니다. 사실상 바이오디젤 시장은 가격적인 이점이 주요 요인으로 작용하는 시장에서 장기적인 수요 전망이 있는 규제적 의무에 의해 형성되는 시장으로 점점 더 전환되고 있습니다. 또한 이러한 의무는 연료 저장, 혼합 인프라, 전체 공급망 시스템의 업그레이드를 촉진하고, 열악한 산업 환경에서 연료 성능 향상을 위한 지속적인 연구를 촉진하고 있습니다. 명확한 규제 프레임워크는 생산 능력, 원료 처리 시설 및 공급 네트워크 확장을 위한 미래 투자에 대한 지침이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 705억 달러 |

| 예측액 | 1,820억 달러 |

| CAGR | 9.9% |

사용 후 식용유 부문은 2035년까지 연평균 복합 성장률(CAGR) 11.4%를 나타낼 것으로 예측됩니다. 폐식용유는 기존 석유 원료에 비해 수명주기 동안 탄소 강도가 낮다는 특성으로 인해 바이오디젤 생산에 있으며, 매우 전략적인 원료로 급부상하고 있습니다. 온실가스 감축에 대한 규제가 강화되면서 연료 공급망에서 지속가능성 지표를 개선할 수 있는 폐기물 유래 원료의 사용이 촉진되고 있습니다. 투명성 기준이 강화됨에 따라 원자재 조달에 있으며, 추적성 및 모니터링 시스템의 중요성이 점점 더 커지고 있습니다. 규제 감독 및 검증 메커니즘의 개선으로 재생유 원료의 국제 공급망에 대한 신뢰가 높아지면서 향후 바이오디젤 생산에서 폐식용유의 역할이 더욱 강화되고 있습니다.

운송 용도 부문은 2025년 71.7%의 점유율을 차지하며, 2035년까지 연평균 9%의 성장률을 보일 것으로 전망됩니다. 디젤 연료에 재생 연료를 혼합하도록 의무화하는 규제 정책이 증가함에 따라 운송 분야는 여전히 바이오디젤 소비의 가장 큰 분야로 남아 있습니다. 정책 입안자들은 여전히 전통적 디젤 엔진에 대한 의존도가 높은 운송 부문의 배출량을 줄이기 위한 실용적인 해결책으로 바이오디젤을 점점 더 중요하게 여기고 있습니다. 바이오디젤은 기존 디젤 인프라에 직접 통합할 수 있으므로 차량이나 연료 공급 시스템을 대대적으로 개조하지 않고도 에너지 전환 목표를 달성할 수 있습니다. 이러한 호환성을 통해 운영 효율성을 유지하면서 상용 차량 및 대규모 운송 네트워크 전반에 걸쳐 도입이 가속화되고 있습니다.

2025년 미국 바이오디젤 시장은 93%의 점유율을 차지하며 219억 달러의 시장 규모를 기록했습니다. 미국 시장의 발전은 탄소 강도 감소에 초점을 맞춘 체계적인 정책 메커니즘과 컴플라이언스 시장을 통해 재생 연료의 사용을 촉진하는 강력한 규제 환경으로 지원되고 있습니다. 또한 이 지역의 업계에서는 지속가능성에 대한 기대가 높아짐에 따라 기존 작물 유래 원료에서 폐기물 및 잔류물 유래 원료로 점차 전환이 진행되고 있습니다. 또한 국제 바이오디젤 시장을 향한 미국의 활발한 수출 활동은 국내 생산의 안정성을 지속적으로 향상시켜 이 부문의 장기적인 회복력을 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 규모·예측 : 원료별, 2022-2035

제6장 시장 규모·예측 : 용도별, 2022-2035

제7장 시장 규모·예측 : 지역별, 2022-2035

제8장 기업 개요

KSA 26.04.20The Global Biodiesel Market was valued at USD 70.5 billion in 2025 and is estimated to grow at a CAGR of 9.9% to reach USD 182 billion by 2035.

Expansion across the biodiesel market is supported by strengthening national fuel blending mandates targeting the transportation sector, along with regulatory frameworks encouraging the use of cleaner fuel alternatives. Governments across several diesel-dependent economies are steadily raising required biodiesel blend ratios as part of broader decarbonization strategies for heavy transport operations. As equipment manufacturers broaden warranty coverage for engines operating on higher biodiesel blends, the financial and operational barriers to adoption continue to decline. This dynamic allows fleet operators to integrate biodiesel into existing systems without requiring significant capital investment in new vehicles. In effect, biodiesel is increasingly shifting from a market driven by optional price advantages to one shaped by regulatory obligations with long-term demand visibility. These mandates are also stimulating upgrades across fuel storage, blending infrastructure, and supply chain systems while encouraging continued research aimed at improving fuel performance in demanding industrial environments. Clear regulatory frameworks are providing signals for future investments in production capacity, feedstock processing facilities, and supply network expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $70.5 Billion |

| Forecast Value | $182 Billion |

| CAGR | 9.9% |

The used cooking oil segment is projected to grow at a CAGR of 11.4% through 2035. Used cooking oil has rapidly emerged as a highly strategic feedstock within biodiesel production due to its ability to deliver lower lifecycle carbon intensity compared with many traditional oil sources. The increasing regulatory focus on reducing greenhouse gas emissions is encouraging the use of waste-derived feedstocks that can improve sustainability metrics within fuel supply chains. As transparency standards continue to strengthen, traceability and monitoring systems for feedstock sourcing have become increasingly important. Improved regulatory oversight and verification mechanisms are helping create stronger confidence in international supply networks for recycled oil feedstocks, further supporting the role of used cooking oil in future biodiesel production.

The transportation application segment accounted for 71.7% share in 2025 and is projected to grow at a CAGR of 9% through 2035. Transportation remains the largest area of biodiesel consumption due to the growing number of regulatory policies that mandate renewable fuel blending in diesel supplies. Policymakers increasingly view biodiesel as a practical solution for reducing emissions from transportation sectors that remain heavily dependent on conventional diesel engines. Since biodiesel can be integrated directly into existing diesel infrastructure, it enables energy transition goals without requiring large-scale modifications to vehicles or fuel distribution systems. This compatibility supports faster adoption across commercial fleets and large transportation networks while maintaining operational efficiency.

U.S. Biodiesel Market held 93% share in 2025 and generated USD 21.9 billion. Market development in the United States is supported by a robust regulatory environment that promotes renewable fuel usage through structured policy mechanisms and compliance markets focused on reducing carbon intensity. The regional industry is also undergoing a gradual shift away from traditional crop-based feedstocks toward waste-based and residue-derived raw materials to meet evolving sustainability expectations. In addition, strong export activity from the United States toward international biodiesel markets continues to strengthen domestic production stability and supports the long-term resilience of the sector.

Major companies operating across the Global Biodiesel Market include Wilmar International, Archer Daniels Midland, Cargill, Bunge, Chevron, Total Energies, Clariant, FutureFuel, Greenergy, Grupo Potencial, Manuelita, Universal Biofuels, Renewable Biofuels, Washwell Biodiesel, TerraVia, Ag Processing, Abellon Clean Energy, Altret Greenfuels, Anellotech, and G-Energetic Biofuels. Companies participating in the Global Biodiesel Market are strengthening their competitive position through a combination of capacity expansion, feedstock diversification, and strategic partnerships across the fuel value chain. Many producers are investing in advanced processing technologies to improve production efficiency while enabling the use of alternative feedstocks derived from waste oils and agricultural residues. Strategic collaborations with feedstock suppliers, logistics providers, and energy distributors are helping companies secure reliable supply networks and expand market access. Several firms are also focusing on developing integrated biofuel platforms that combine refining, storage, and distribution capabilities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Feedstock trends

- 2.1.3 Application trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Feedstock, 2022 - 2035 (USD Million, Mtoe)

- 5.1 Key trends

- 5.2 Vegetable oils

- 5.3 Used cooking oil (UCO)

- 5.4 Animal fats

- 5.5 Others

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million, Mtoe)

- 6.1 Key trends

- 6.2 Transportation

- 6.3 Power generation

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million, Mtoe)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 UK

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Indonesia

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Abellon Clean Energy

- 8.2 Ag Processing

- 8.3 Altret Greenfuels

- 8.4 Anellotech

- 8.5 Archer Daniels Midland

- 8.6 Bunge

- 8.7 Cargill

- 8.8 Chevron Corporation

- 8.9 Clariant

- 8.10 FutureFuel

- 8.11 G-Energetic Biofuels

- 8.12 Greenergy

- 8.13 Grupo Potencial

- 8.14 Manuelita

- 8.15 Renewable Biofuels

- 8.16 TerraVia

- 8.17 Total Energies

- 8.18 Universal Biofuels

- 8.19 Washwell Biodiesel

- 8.20 Wilmar International