|

시장보고서

상품코드

1998750

선박 탑재 통신 및 제어 시스템 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Marine Onboard Communication and Control Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

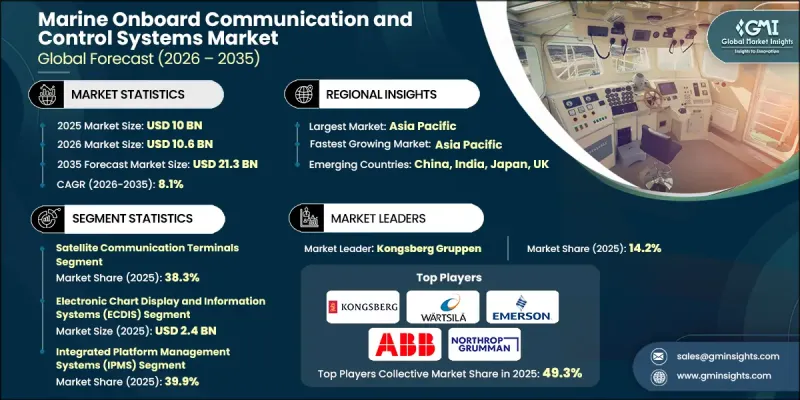

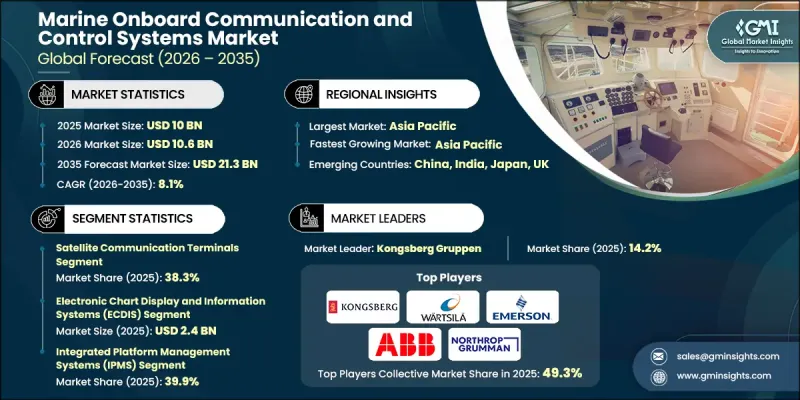

세계의 선박 탑재 통신·제어 시스템 시장은 2025년에 100억 달러로 평가되며, CAGR 8.1%로 성장하며, 2035년까지 213억 달러에 달할 것으로 추정되고 있습니다.

이 시장의 확대는 스마트 선박 자동화 플랫폼의 도입 확대, 신뢰할 수 있는 해상 위성통신에 대한 수요 증가, 세계 상선대의 지속적인 성장에 의해 주도되고 있습니다. 실시간 선박 모니터링 및 선대 관리 시스템의 통합과 더불어 디지털 항법 및 해상 안전 프레임워크의 발전은 시장 성장을 더욱 촉진하고 있습니다. 해운사들은 항해, 추진 및 운항 제어를 통합하는 커넥티드 선내 시스템에 대한 의존도가 높아지고 있으며, 이를 통해 효율성, 운항 안전 및 규정 준수를 향상시키고 있습니다. 또한 디지털 해상 인프라에 대한 정부의 투자와 선단 모니터링, 해상 영역 인식 및 운항 안전성 향상을 위한 노력도 첨단 선내 통신 및 제어 솔루션의 보급에 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 100억 달러 |

| 예측액 | 213억 달러 |

| CAGR | 8.1% |

위성통신 단말기 부문은 선박과 육상 기지 간 끊김 없는 장거리 통신을 제공할 수 있는 능력으로 인해 2025년 38.3%의 점유율을 차지할 것으로 예측됩니다. 이러한 시스템은 광활한 해역을 가로지르는 실시간 항로 업데이트, 운항 관리 및 승무원 간의 원활한 통신을 지원하여 지속적인 수요를 견인하고 있습니다.

전자해도 표시 및 정보 시스템(ECDIS) 부문은 디지털 항해 및 해상 안전에 중요한 역할을 수행하면서 2025년 24억 달러의 시장 규모를 형성하며 시장을 주도할 것으로 예측됩니다. ECDIS는 실시간 항해 데이터를 제공하고, 상황 인식을 향상시키며, 규제 요건을 준수함으로써 기존의 종이 해도를 대체하고 있습니다. ECDIS와 레이더, AIS, GNSS 시스템과의 통합으로 그 중요성과 상용 선단에서의 도입이 더욱 강화되고 있습니다.

2025년 북미 선박용 통신 및 제어 시스템 시장은 28.3%의 점유율을 차지했습니다. 이 지역의 성장은 해군 현대화, 해상 작업 및 디지털 선박 기술 도입에 대한 막대한 투자로 지원되고 있습니다. 상선사 및 해군 당국은 운항 안전과 효율성을 높이기 위해 선내 자동화, 통합 브리지 시스템 및 위성통신 솔루션을 점점 더 많이 도입하고 있습니다. 해상 상황 인식, 해군용 통신 및 함대 모니터링에 중점을 둔 정부의 구상은 첨단 선상 시스템의 도입을 지속적으로 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 통신 시스템별, 2022-2035

제6장 시장 추산·예측 : 내비게이션·측위 시스템별, 2022-2035

제7장 시장 추산·예측 : 제어·자동화 시스템별, 2022-2035

제8장 시장 추산·예측 : 모니터링·감시 시스템 용도별, 2022-2035

제9장 시장 추산·예측 : 플랫폼별, 2022-2035

제10장 시장 추산·예측 : 최종사용자별, 2022-2035

제11장 시장 추산·예측 : 지역별, 2022-2035

제12장 기업 개요

KSA 26.04.20The Global Marine Onboard Communication and Control Systems Market was valued at USD 10 billion in 2025 and is estimated to grow at a CAGR of 8.1% to reach USD 21.3 billion by 2035.

The market expansion is driven by the increasing adoption of smart vessel automation platforms, rising demand for reliable maritime satellite connectivity, and the continuous growth of global commercial shipping fleets. The integration of real-time vessel monitoring and fleet management systems, alongside the advancement of digital navigation and maritime safety frameworks, is further supporting market growth. Shipping companies are increasingly relying on connected onboard systems that integrate navigation, propulsion, and operational control, enhancing efficiency, operational safety, and regulatory compliance. Government investments in digital maritime infrastructure and initiatives aimed at improving fleet monitoring, maritime domain awareness, and operational safety are also contributing to the widespread adoption of advanced onboard communication and control solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10 Billion |

| Forecast Value | $21.3 Billion |

| CAGR | 8.1% |

The satellite communication terminals segment held 38.3% share in 2025, owing to their capability to provide uninterrupted long-range communication between ships and shore-based operations. These systems support real-time route updates, operational management, and seamless crew communication across vast maritime distances, driving sustained demand.

The electronic chart display and information systems (ECDIS) segment was valued at USD 2.4 billion in 2025 and dominated the market due to its crucial role in digital navigation and maritime safety. ECDIS replaces traditional paper charts by providing real-time navigational data, enhancing situational awareness, and complying with regulatory mandates. The integration of ECDIS with radar, AIS, and GNSS systems further strengthens its relevance and adoption across commercial fleets.

North America Marine Onboard Communication and Control Systems Market accounted for 28.3% share in 2025. The region's growth is supported by substantial investment in naval modernization, offshore maritime operations, and the deployment of digital vessel technologies. Commercial shipping companies and naval authorities are increasingly implementing onboard automation, integrated bridge systems, and satellite communication solutions to enhance operational safety and efficiency. Government initiatives focused on maritime domain awareness, naval communications, and fleet monitoring continue to encourage the adoption of advanced onboard systems.

Prominent players in the Global Marine Onboard Communication and Control Systems Market include L3Harris Technologies, Inc., Raymarine, Viasat, Inc., Northrop Grumman Corporation, Furuno Electric Co., Ltd., Kongsberg, ABB Group, ST Engineering, Wartsila, Honeywell International Inc., Navico Group, Emerson Electric Co., Saab Ab, and Japan Radio Co., Ltd. Companies in the Global Marine Onboard Communication and Control Systems Market are adopting multiple strategies to solidify their presence and expand market share. They are investing in research and development to deliver advanced, integrated communication, navigation, and control solutions. Strategic collaborations with shipbuilders, naval authorities, and fleet operators enhance technology adoption and service reach. Firms are diversifying product portfolios to include satellite communication terminals, ECDIS, integrated bridge systems, and fleet management solutions, enabling comprehensive offerings. Expanding regional operations, enhancing after-sales support, and ensuring regulatory compliance are also key strategies for strengthening market footholds and building long-term client relationships.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Communication systems trends

- 2.2.2 Navigation & positioning systems trends

- 2.2.3 Control & automation systems trends

- 2.2.4 Monitoring & surveillance systems trends

- 2.2.5 Platform trends

- 2.2.6 End-User trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of smart and connected vessels

- 3.2.1.2 Growing maritime satellite communication demand

- 3.2.1.3 Expansion of global seaborne trade and fleet size

- 3.2.1.4 Rising need for real-time vessel monitoring systems

- 3.2.1.5 IMO regulations driving digital navigation systems adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High installation and retrofitting costs for legacy fleets

- 3.2.2.2 Cybersecurity risks in connected shipboard networks

- 3.2.3 Market opportunities

- 3.2.3.1 Autonomous and remotely operated vessel development

- 3.2.3.2 Expansion of satellite broadband for offshore vessels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Communication Systems, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Satellite communication terminals

- 5.2.1 VSAT terminals

- 5.2.2 L-band terminals

- 5.3 Marine Radio Systems

- 5.3.1 VHF radio systems

- 5.3.2 MF/HF radio systems

- 5.3.3 GMDSS equipment

- 5.4 Onboard network infrastructure

- 5.4.1 Routers & switches

- 5.4.2 Onboard broadband backbone systems

- 5.5 Internal communication systems

- 5.5.1 Public address / general alarm (PA/GA) systems

- 5.5.2 Intercom systems

Chapter 6 Market Estimates and Forecast, By Navigation & Positioning Systems, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Electronic chart display & information systems (ECDIS)

- 6.3 Radar systems

- 6.3.1 X-Band radar

- 6.3.2 S-Band radar

- 6.4 Automatic identification systems (AIS)

- 6.5 Global navigation satellite systems (GNSS/GPS)

- 6.6 Voyage data recorders (VDR)

- 6.7 Dynamic positioning systems

Chapter 7 Market Estimates and Forecast, By Control & Automation Systems, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Propulsion control systems

- 7.3 Engine automation systems

- 7.4 Thruster control systems

- 7.5 Power management systems

- 7.6 Integrated platform management systems (IPMS)

Chapter 8 Market Estimates and Forecast, By Monitoring & Surveillance Systems Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Fire detection systems

- 8.3 Gas detection systems

- 8.4 CCTV & onboard security systems

- 8.5 Hull stress monitoring systems

- 8.6 Condition-based monitoring systems

Chapter 9 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Commercial vessels

- 9.2.1 Passenger vessels

- 9.2.2 Cargo vessels

- 9.2.3 Offshore & specialized vessels

- 9.3 Defense vessels

- 9.3.1 Aircraft carriers

- 9.3.2 Destroyers

- 9.3.3 Frigates

- 9.3.4 Corvettes

- 9.3.5 Submarines

- 9.3.6 Amphibious assault ships

Chapter 10 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 ABB Group

- 12.1.2 Kongsberg

- 12.1.3 Wartsila

- 12.1.4 Northrop Grumman Corporation

- 12.1.5 Honeywell International Inc.

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 Emerson Electric Co.

- 12.2.1.2 L3Harris Technologies, Inc.

- 12.2.1.3 Viasat, Inc.

- 12.2.2 Asia Pacific

- 12.2.2.1 Furuno Electric Co., Ltd.

- 12.2.2.2 Japan Radio Co., Ltd.

- 12.2.2.3 Raymarine

- 12.2.3 Europe

- 12.2.3.1 Saab AB

- 12.2.3.2 ST Engineering

- 12.2.1 North America

- 12.3 Niche Players/Disruptors

- 12.3.1 Navico Group