|

시장보고서

상품코드

1998764

골다공증 치료제 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Osteoporosis Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

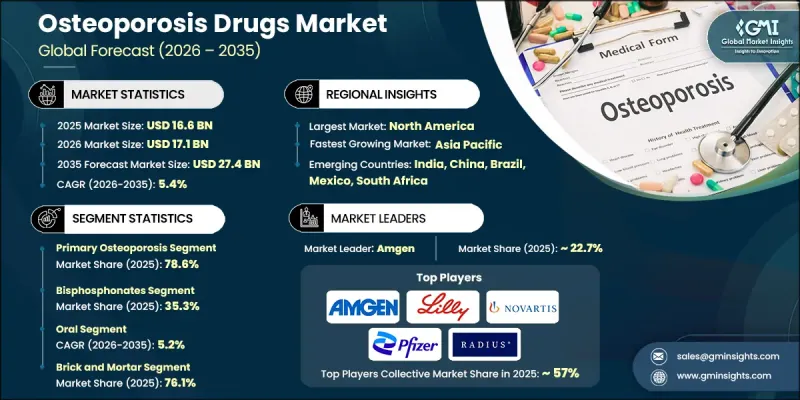

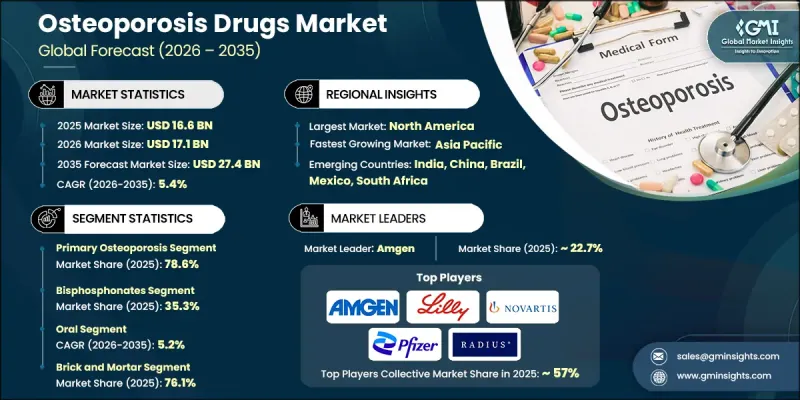

세계의 골다공증 치료제 시장은 2025년에 166억 달러로 평가되며, CAGR 5.4%로 성장하며, 2035년까지 274억 달러에 달할 것으로 추정되고 있습니다.

골다공증 치료제 시장의 성장은 인구 통계학적 변화, 특히 전 세계 노인 인구의 꾸준한 증가와 밀접한 관련이 있습니다. 나이가 들어감에 따라 뼈의 강도는 점차 감소하고, 골절 및 뼈 관련 합병증의 위험이 크게 증가합니다. 골다공증 관리를 위한 약물 치료는 골밀도를 유지하고 골절 위험을 최소화하는 데 필수적인 역할을 합니다. 이러한 약물은 뼈의 분해 과정을 늦추거나 새로운 뼈의 형성을 촉진하여 환자가 장기적으로 골격의 강도를 유지할 수 있도록 돕습니다. 환자와 의료진의 인식이 높아진 것도 진단율 향상에 기여하고 있습니다. 특히 의료제도에서 골감소증의 조기발견이 중요하게 여겨지게된 배경이 있습니다. 진단 스크리닝 기술의 사용 확대는 치료의 조기 시작을 촉진하고, 장기 치료 프로그램에 참여하는 환자 수를 증가시키고 있습니다. 또한 환자 모니터링과 치료 순응도를 돕기 위해 고안된 디지털 건강 툴은 점차 골다공증의 일상적인 관리의 일부가 되어가고 있습니다. 이러한 기술은 치료 결과 개선에 기여하고 의료진이 장기적인 치료 효과를 추적할 수 있도록 돕습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035 |

| 개시 금액 | 166억 달러 |

| 예측액 | 274억 달러 |

| CAGR | 5.4% |

2025년에는 주요 골다공증 부문이 78.6%의 점유율을 차지하며 2035년까지 연평균 5.6%의 성장률로 220억 달러에 달할 것으로 예측됩니다. 노화에 따른 골밀도 감소가 전 세계에서 골다공증 발병의 가장 큰 요인으로 작용하고 있으므로 이 부문은 견고한 수요를 유지하고 있습니다. 많은 국가에서 평균 수명이 길어짐에 따라 뼈가 약화될 위험에 처한 사람들의 수는 계속 증가하고 있습니다. 이러한 인구통계학적 추세는 뼈 건강을 유지하기 위한 장기적인 의약품 개입에 대한 지속적인 수요를 창출하고 있습니다. 또한 진단 스크리닝 기술의 보급으로 의료진은 골감소증을 조기에 발견하여 심각한 합병증이 발생하기 전에 치료를 시작할 수 있게 되었습니다. 질병의 조기 발견은 보다 적극적인 질병 관리를 촉진하고, 골다공증 치료를 받는 전체 환자 증가로 이어지고 있습니다.

경구용 의약품 부문은 2025년 91억 달러의 시장 규모를 기록하며, 2026-2035년 연평균 복합 성장률(CAGR) 5.2%를 나타낼 것으로 예측됩니다. 경구용 제제는 환자 편의성이 높고 여러 의료 채널을 통해 쉽게 유통될 수 있으므로 여전히 널리 사용되고 있습니다. 선진국과 개발도상국의 의료 시스템 모두에서 쉽게 이용할 수 있다는 점은 안정적이고 일관된 시장 수요를 보장합니다. 의료진은 뼈의 건강을 돕고 골절과 관련된 합병증 발생 확률을 낮춘다는 점에서 치료 효과가 입증된 경구용 골다공증 치료제를 지속적으로 처방하고 있습니다. 경구 치료와 관련된 풍부한 임상 실적은 의사들의 이러한 치료법에 대한 신뢰를 강화하여 전 세계에서 보급에 기여하고 있습니다.

미국 골다공증 치료제 시장은 2025년 57억 달러에 달했습니다. 골다공증 관련 질환은 북미의 고령화 인구에서 여전히 흔한 질환으로 장기적인 약물 치료의 필요성이 증가하고 있습니다. 평균 수명이 연장됨에 따라 뼈 건강 상태를 지속적으로 관리해야 하는 환자 수가 증가하고 있습니다. 또한 인식 개선 활동 강화와 의사 주도의 검진 프로그램도 조기 발견율 향상에 기여하고 예방적 치료법 활용을 촉진하고 있습니다. 또한 첨단 의료 인프라와 진단기술이 잘 갖추어진 환경은 이 지역 전체에서 효과적인 질병 관리를 지속적으로 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 유형별, 2022-2035

제6장 시장 추산·예측 : 약제 클래스별, 2022-2035

제7장 시장 추산·예측 : 투여 경로별, 2022-2035

제8장 시장 추산·예측 : 유통 채널별, 2022-2035

제9장 시장 추산·예측 : 지역별, 2022-2035

제10장 기업 개요

KSA 26.04.20The Global Osteoporosis Drugs Market was valued at USD 16.6 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 27.4 billion by 2035.

The growth of the osteoporosis drugs market is closely associated with demographic changes, particularly the steady expansion of the elderly population worldwide. As individuals age, bone strength gradually declines, which significantly increases the risk of fractures and bone-related complications. Pharmaceutical therapies designed to manage osteoporosis play an essential role in preserving bone density and minimizing fracture risk. These medications function by slowing the process of bone degradation or by stimulating new bone formation, helping patients maintain skeletal strength over time. Increased awareness among patients and healthcare providers has also contributed to improved diagnosis rates, particularly as healthcare systems emphasize early detection of bone loss conditions. The growing use of diagnostic screening technologies is encouraging earlier treatment initiation and expanding the number of patients entering long-term therapy programs. In addition, digital health tools designed to support patient monitoring and treatment adherence are gradually becoming part of routine osteoporosis management. These technologies contribute to better therapeutic outcomes and help healthcare providers track long-term treatment effectiveness.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16.6 Billion |

| Forecast Value | $27.4 Billion |

| CAGR | 5.4% |

The primary osteoporosis segment held 78.6% share in 2025 and is expected to reach USD 22 billion by 2035 while growing at a CAGR of 5.6%. This segment maintains strong demand because bone density loss associated with aging represents the largest source of osteoporosis cases globally. As life expectancy increases across many countries, the number of individuals vulnerable to bone deterioration continues to grow. This demographic trend is generating sustained demand for long-term pharmaceutical interventions designed to preserve bone health. Expanding use of diagnostic screening technologies is also enabling healthcare professionals to detect bone loss at earlier stages, allowing treatment to begin before severe complications occur. Earlier identification of the condition is encouraging more proactive disease management and increasing the overall patient population receiving osteoporosis therapies.

The oral segment generated USD 9.1 billion in 2025 and is projected to grow at a CAGR of 5.2% throughout 2026-2035. Oral drug formulations remain widely used because they are convenient for patients and easily distributed through multiple healthcare channels. Their accessibility across both developed and developing healthcare systems ensures stable and consistent market demand. Healthcare professionals continue to prescribe oral osteoporosis medications due to their well-established therapeutic effectiveness in supporting bone health and lowering the likelihood of fracture-related complications. The extensive clinical history associated with oral treatments has strengthened physician confidence in these therapies and contributed to their continued adoption worldwide.

U.S. Osteoporosis Drugs Market reached USD 5.7 billion in 2025. Osteoporosis-related conditions remain common among the aging population in North America, contributing to the growing need for long-term pharmaceutical treatment. Rising life expectancy is expanding the number of patients who require continued management of bone health conditions. Increased awareness initiatives and physician-led screening programs have also improved early detection and encouraged the use of preventive treatment options. In addition, advanced healthcare infrastructure and strong availability of diagnostic technologies continue to support effective disease management across the region.

Prominent companies operating in the Global Osteoporosis Drugs Market include Amgen, Apotex, DAIICHI SANKYO COMPANY, Dr. Reddy's Laboratories, Eisai, Eli Lilly and Company, Merck & Co., Mylan, Novartis, Pfizer, Radius Health, Roche, Sanofi, Sun Pharmaceutical Industries, and Teva Pharmaceutical Industries. Companies competing in the Global Osteoporosis Drugs Market are strengthening their competitive position through a combination of product innovation, research investments, and strategic collaborations. Many pharmaceutical manufacturers are increasing funding for clinical research to develop next-generation therapies that improve treatment outcomes and support long-term bone health management. Organizations are also expanding their global distribution networks to increase product availability across emerging healthcare markets. Partnerships with healthcare providers and research institutions are helping companies accelerate drug development and improve patient access to therapies. Additionally, firms are focusing on digital health integration to support medication adherence and patient monitoring.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Drug class trends

- 2.2.4 Route of administration trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of osteoporosis

- 3.2.1.2 Technological advancements in drug development

- 3.2.1.3 Rising incidence of fractures

- 3.2.1.4 Growth in biologic and novel therapeutic adoption

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Side effects and safety concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Development of next-generation anabolic agents

- 3.2.3.2 Biosimilar and biobetter entry

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Future market trends

- 3.8 Pipeline analysis

- 3.9 Value chain analysis

- 3.10 Impact of AI and generative AI on the market

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Start-up scenarios

- 3.14 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Primary osteoporosis

- 5.2.1 Postmenopausal osteoporosis

- 5.2.2 Senile osteoporosis

- 5.2.3 Idiopathic osteoporosis

- 5.3 Secondary osteoporosis

Chapter 6 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Bisphosphonates

- 6.3 RANK ligand inhibitors

- 6.4 Parathyroid hormone analogs

- 6.5 Hormone replacement therapy (HRT)

- 6.6 Selective estrogen receptor modulators (SERMs)

- 6.7 Other drug classes

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

- 7.4 Other route of administrations

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Brick and mortar

- 8.3 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amgen

- 10.2 Apotex

- 10.3 DAIICHI SANKYO COMPANY

- 10.4 Dr. Reddy’s Laboratories

- 10.5 Eisai

- 10.6 Eli Lilly and Company

- 10.7 Merck & Co.

- 10.8 Mylan

- 10.9 Novartis

- 10.10 Pfizer

- 10.11 Radius Health

- 10.12 Roche

- 10.13 Sanofi

- 10.14 Sun Pharmaceutical Industries

- 10.15 Teva Pharmaceutical Industries